Most buyers in Quebec, especially first-timers, drastically underestimate the actual cash that they need to buy a home. This is because closing costs, which are typically tens of thousands of dollars, only show up right at the end of the transaction.

But don’t worry—you may not have to pay all of these costs out of pocket. Experienced buyers don’t pay every expense at face value. They negotiate certain costs, avoid others altogether, and use government grants, tax credits, and rebate programs get money back whenever possible.

I learned this firsthand. My closing costs were roughly $12,000, but the seller agreed to pay $2,000 of my costs, and I received a $5,000 municipal grant. In total, I reduced my out-of-pocket costs by $7,000—and I felt great about it!

In this article I’ll cover everything that you need to know about closing costs, including:

- What are closing costs?

- What is total cash to close?

- What is typically included in closing costs?

- How to manage closing costs

- Which closing costs are fixed vs negotiable

- How experienced buyers reduce their closing costs

- Final remarks

Want To Reduce Your Closing Costs?

Research shows that the right real estate agent can reduce your closing costs by up to 60%. Use Immovision AI to find top-rated, local agents so that you can avoid overpaying for your home.

What are closing costs?

Closing costs are the one time fees and taxes that buyers and sellers must pay in order to complete a real-estate transaction.

In Quebec, the buyers closing costs are typically between 2 – 4% of the purchase price. Whereas sellers closing costs are typically between 3 – 5% of the buyers total purchase price.

For example, let’s say that you want to buy a home worth $750,000. In this case, the closing costs would be between $15,000 and $30,000 for the buyer, and between $22,500 and $37,500 for the seller. If the buyer was making a downpayment of 20%, this means they would need to pay $150,000 plus an additional $15,000 – $30,000 in closing costs.

⚠️ Budget Carefully

Closing costs are a lot of money, and something that you will need to budget for.

Many buyers save enough for their down payment but underestimate the cash they will need to cover taxes, legal fees, inspections, insurance, and other closing costs. If you arrive at closing without sufficient funds, you could delay the transaction, breach your purchase agreement, lose your deposit, and end up in a financial and even legal nightmare.

To help you develop an accurate estimate of your closing costs, we built the Immovision Closing Cost Calculator. You can use this for free.

What is total cash to close?

The total cash to close is the total amount of cash that has to be paid by the buyer in order to close. This is normally calculated as:

Total Buyer Cash To Close = Downpayment + Closing Costs + Adjustments

In a standard real-estate transaction in Quebec, the general advice is that your closing costs will be between 2% – 4% of the purchase price to close.

The table below shows an example of this. If we assume a $750,000 purchase price, a 20% down payment, closing costs of 4% of the purchase price for the buyer and $2500 of adjustments.

| Downpayment | $150,000 |

| Closing costs | $30,000 |

| Adjustments | $2,500 |

| Total cash required to close | $182,500 |

ℹ️ Note

At closing, you may need to reimburse the seller for things they have already paid for. This might include pre-paid school and municipal property taxes, utilities, condo fees, and so on.

Your notary calculates any adjustments at closing.

Because some closing costs are variable, it’s better to slightly over-budget for them. This way, you have a buffer for surprises instead of scrambling for cash at the last step.

What is typically included in closing costs?

The buyers closing costs in Quebec typically include the following:

- Property inspection

- Notary

- Adjustments & reimbursements

- Land transfer tax

- Moving fees

- Appraisal fee

- Title insurance

- Latent defect insurance

Now that we know what closing costs are, let’s take a look at what exactly each of them is for.

ℹ️ Buyers Note

Not all of the closing costs listed here are mandatory. You should ask your realtor which costs are essential for you. This will help you to avoid overpaying for your home.

If you need to find a good buyer’s broker in your area, you can use our free Find And Compare Realtor platform that ranks local brokers according to their performance history.

Property inspection (Average cost: $800 – $1300)

A property inspection (often called a home inspection or pre-purchase inspection) is an independent evaluation of a home’s physical condition, carried out before you finalize the purchase.

You indicate that you want a property inspection in your promise to purchase, under Clause 8: “Inspection by a person chosen by the buyer.”

Most people consider this an essential step in the home buying process because, the promise to purchase is a legally binding contract. Without this clause, the seller can force you to buy the property even if you discover a major issue with the property during closing.

Whilst many sellers get a pre-listing inspection, you should not rely solely on this. This is because you don’t know who performed the inspection, what standards they followed, or whether the report was biased. More importantly, you have no legal relationship with the seller’s inspector. This means that you will have no legal recourse if the inspector missed something critical.

ℹ️ Note

Before you sign your promise to purchase, speak with your real estate broker about the type of inspection that best suits the property you are considering. Older homes, income properties, and properties with known issues may require additional inspections beyond a standard home inspection. These will look for issues like pyrite, asbestos, radon, mould, or Iron Ochre.

Keep in mind that the OACIQ (Quebec’s real estate brokerage regulator) requires:

- Brokers to recommend that buyers obtain a pre-purchase inspection whenever possible.

- Brokers who recommend inspectors to provide at least two options so that buyers can make an informed choice.

While many buyers choose an inspector recommended by their broker, your broker may earn a commission on that referral, which means the recommendation may not be entirely independent.

If you prefer an independent referral, you can use Immovision’s Find a Specialist feature to locate inspectors and other real estate professionals in your area.

Notary (Average cost: $1,700 – $2,800)

In Quebec, it is typical for the buyer to hire the notary. This is because the notary does work to the direct benefit of the buyer. For instance, the notary will make sure the person selling the property has the property title and the legal right to sell the home. They will also check for unpaid taxes or hypothec such as a hypothec of construction, and ensure that the property is free of any other legal claims, zoning law violations, or any other encumbrances.

Once these checks are complete, the notary prepares the key legal documents. This will include the Deed of Sale and, if needed, the Deed of Hypothec (your mortgage contract). The notary will then coordinate with your lender to receive the mortgage funds and hold them safely in trust until the transaction closes.

The notary will also calculate adjustments between buyer and seller. This will include things like prepaid property taxes or condo fees.

Finally, the notary will arrange the final appointment where both parties sign the Deed of Sale. Once this has happened, the notary registers the sale in the Quebec Land Register, transfers the funds to the seller, pays the brokers their commission, and provides you with certified copies of the deeds. At that point, the process is complete and ownership officially passes to you.

Adjustments & reimbursements (Average cost: It depends on the property and time of year)

Adjustments are reimbursements between the buyer and seller for any prepaid costs (like school taxes, municipal taxes, condo fees or special assessments). The notary calculates these at closing to make sure each party pays their fair share based on the possession date.

For example, let’s say you’re buying a condo and the seller has already paid the municipal taxes for the next six months, but your move-in date is one month away. In that case, the seller may ask you to reimburse the remaining five months of prepaid taxes, since you’ll benefit from that period of ownership.

These adjustments typically range from a few hundred to a few thousand dollars, depending on the property and the time of year.

Land transfer tax (Average cost: It depends on the size of your property)

In Quebec, you must pay a municipal land transfer tax (also known as the Welcome Tax) whenever you buy a property. For example, let’s say that you buy a condo for $500,000 on the Island of Montreal. In this case, you will need to pay roughly $5,000 in land transfer tax.

The municipalities use the revenue that this tax generates to fund local infrastructure and services such as road repairs, public transit, parks, libraries, and emergency services.

It is a progressive tax which means that the municipality will tax different portions of the property’s value at different rates. For example, they will tax the first $50,000 of property value at 0.5%, whereas they might tax the next $50,000 of value at 1%, and the upper portion of the home is at a higher rate. The municipality calculate the properties value itself as the higher of either the purchase price or the assessed value.

Officially, municipalities say that you have 30 days to pay your welcome tax from the billing date, and you should receive the bill within 30 to 60 days of your purchase. However, many realtors will tell you that in practice it can take several months—and sometimes over a year—before you receive your bill. You can pay the welcome tax either by going into your local bank or online.

Calculate Your Exact Welcome Tax

Your Welcome Tax is variable based on the value of your home and where you buy. Use our Welcome Tax calculator to calculate the exact amount that you will have to pay.

Moving costs (Average cost: $750 – $1,500)

Buying a new home comes with all the moving expenses that follow. This includes boxes, packing supplies, transportation, and sometimes storage. Even after you’ve signed at the notary, you will still need to budget for the physical move itself.

If you have large furniture, small children, or a busy family schedule, hiring professional movers can be a worthwhile investment. They can handle heavy lifting, reduce stress, and often include basic insurance for your belongings during transport.

ℹ️ Where To Find Movers In Quebec

You can compare and book movers easily on platforms like MovingWaldo or Kijiji. On these websites you can read reviews and request quotes from multiple companies in just a few minutes.

Appraisal fee (Average cost: Depends on the size of the property)

A home appraisal is an unbiased, professional evaluation of a property’s current market value conducted by a licensed or certified appraiser. Lenders mostly require this before they will sign off on your mortgage. This is because the lender wants to make sure that they are not lending more than the home is worth. There are two ways to order an appraisal:

- Lender orders an appraisal (most common)

- Buyer orders an appraisal

In most transactions, the buyer never personally orders or even sees the appraisal. This is because your lender hires a certified appraiser to confirm that the property’s market value that supports the loan amount. If you are working with an A Lender, they will most likely not even charge you for the appraisal. By contrast, if you are working with a B Lender or another Alternative Lender, they charge for the home appraisal as part of their mortgage administration fees.

If you want to double-check the price independently for example, in a private sale, a cash purchase, or to challenge an asking price, you can hire your own appraiser. This is less common but gives you visibility into the report. More commonly you would ask your realtor to complete a Comparative Market Analysis (CMA) of the property. Your realtor can use this to challenge a home appraisal if necessary.

Find Out The Value Of Your Property In Seconds

Get a free valuation of any property in seconds so that you do not overpay for the home.

Title insurance (Average cost: $500 – $1,200)

When you buy a home, your notary conducts a title search through the Quebec Land Register to confirm that the seller legally owns the property, that it’s free of unpaid debts, and that there are no hidden legal claims. All of this information is summarized in the property title, also known as the Index of Immovables.

Title insurance is an optional one-time protection that covers you and your lender against unexpected problems with the property title. These are things the notary might not have been able to detect during their search. These could include clerical or registration errors in the land registry, unpaid liens from a previous owner, boundary disputes, or even fraud or forgery where someone illegally claims ownership.

In Quebec’s civil law system, the notary is legally responsible for verifying ownership, disclosing servitudes, and ensuring there are no outstanding debts on the property. Because of this, most lenders don’t require title insurance and instead rely on the notary’s verification to protect their interests.

Many notaries consider title insurance optional and only recommend it in specific situations for example, when the property has an unclear ownership history, when renovations or additions weren’t properly registered, or violate local zoning bylaws, or when it’s located on a private road or rural lot with servitudes.

If your notary reviewed the Quebec Land Register and found everything in order, they likely didn’t suggest title insurance and that’s perfectly normal in Quebec.

Latent defect insurance (Average cost: $350–$600)

A latent defect (or vice caché) is a hidden problem with a property that isn’t visible during a normal inspection and that significantly reduces the property value or use. Examples might include water infiltration behind walls, foundation cracks, electrical faults, or mould hidden behind dry wall.

In Quebec, the Civil Code gives buyers the right to take legal action against the seller if such a defect existed before the sale and the seller failed to disclose it in their Sellers Declaration. However, these cases can be complex, stressful, and expensive often taking months or years to resolve.

Latent defect insurance is an optional policy that helps protect you from the financial fallout of discovering a hidden issue after you move in. It can cover the cost of repairs or reimburse part of your loss if a serious defect is found and confirmed by an expert.

💡 Buyer’s Tip

Some brokerages in Quebec, such as Royal LePage and RE/Max, include a latent defect insurance policy. Check with your realtor if you are covered by their latent defect insurance.

You can find realtors that carry latent defect insurance for their clients on our Find and Compare Realtors platform.

How to manage closing costs?

To manage your closing costs, we recommend that you use a closing cost calculator. These will give you a better understanding of how closing costs work and how much to budget .You can access our free closing cost calculator @ Immovision Closing Cost Calculator.

As we have already said, closing costs generally fall between 2% – 4% of the purchase price of the property. However, there can be surprises, and so it’s better to slightly over budget so that you are not left scrambling for cash at the last moment.

From our own research, we found that 40 – 60% of closing costs are negotiable, which can save you A LOT of money. Therefore, you should ask your realtor:

Below is our analysis.

Which closing costs are fixed vs negotiable

💡 Buyers Tip

Every transaction is different. Ask your realtor which costs you can negotiate in your specific situation and save money on your closing costs.

How experienced buyers reduce their closing costs

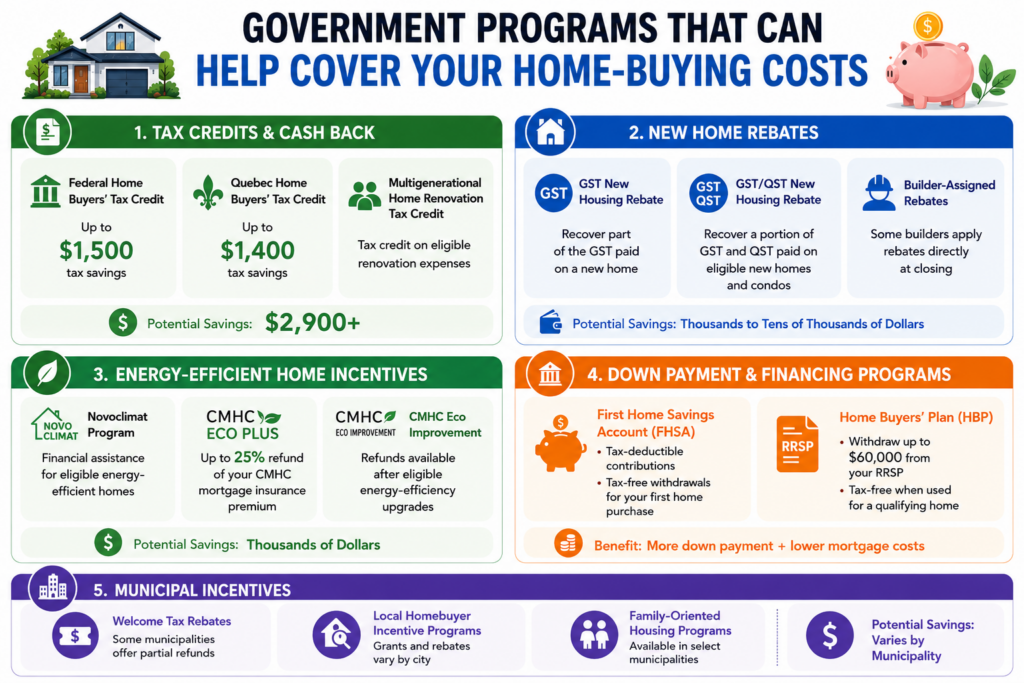

Experienced buyers don’t just negotiate lower closing costs, they also look for federal, provincial, and municipal programs that cover part, or all of their closing costs.

The infographic below gives a list of some of the programs that you may be able to apply for in Quebec. Check with your realtor to see which apply in your specific case.

Want To Reduce Your Closing Costs?

Research shows that the right real estate agent can reduce your closing costs by up to 60%. Use Immovision AI to find top-rated, local agents so that you can avoid overpaying for your home.

Final remarks

Most people feel financially stretched when buying a new home. This is made worse by the closing costs that will add tens of thousands of dollars to the purchase price.

So as to avoid putting yourself into a dangerous financial situation, you should make sure that you understand exactly what you need to pay and when exactly will need to pay it. To do this, make sure that you fully understand the steps involved in your home purchase.

A good realtor will not only help you estimate your closing costs, but they will also help to identify which costs you can skip on, and what rebate programs you can use to get your money back so that you can avoid overpaying for your home.

You can find and compare local realtors for free on the Immovision Agent Finder platform (no login required).

Related articles

There is a lot of financial assistance that is available and can help you get some of the money back when buying a new home. To learn more about what schemes are available in for buyers in Quebec, read the following: