Buying a house in Montreal can feel overwhelming at first. But the process itself can be described in 9 steps:

- Work out your budget

- Get mortgage pre-approval

- Make a list of properties you want to visit

- Find a buyer’s broker

- Visit the homes

- Make an offer (in Quebec we call this a Promise to Purchase)

- Secure Financing and Complete Inspections

- Hire a notary to complete the legal paperwork and transfer legal ownership to you

- Organize your move and pick up the keys

The graphic below gives a visual illustration of these 9 steps.

As you can see, the challenge is not understanding the steps. The challenge is making good decisions at each step — especially in a market as local and nuanced as Montreal.

In the rest of this article, we break down each stage of the buying process so that you can understand what is happening, ask better questions, and avoid some of the mistakes that catch buyers off guard.

But before we begin, there is one important question worth addressing: should you hire a realtor to help with your home-buying journey, and if so, how do you know whether a realtor is actually a good fit for your situation?

Find a local expert

We’ve developed an AI-powered system that analyzes more than 27 million past real estate transactions to help match you with the best realtor for your needs in Montreal.

1. Work out your budget

It’s important to figure out how much you can afford to spend before you start looking for a home. Your mortgage payment will probably be the biggest expense, but there are other costs you should be aware of. You don’t want any unpleasant surprises!

The more you know about your current financial situation, the more prepared you’ll be when you meet with your lender or mortgage broker. These calculations will clarify your current financial picture and help you figure out how much you can afford.

- Calculation 1: How much are you spending now

- Calculation 2: How much can you afford monthly

- Calculation 3: Figure out upfront costs

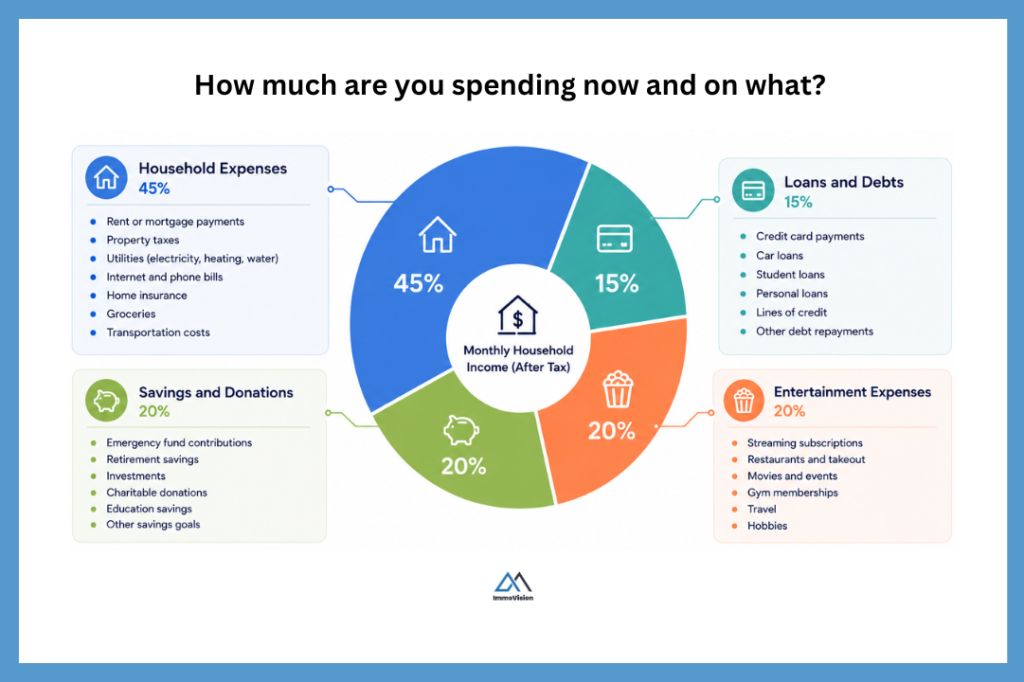

Calculation 1: How much are you spending now

First, list out what you currently spend each month. Group these expenses into four categories:

- Household expenses e.g. rent, groceries, electricity, internet, insurance, cell phone bills

- Loans and debts e.g. car payments, student loans, credit card payments, personal loans

- Entertainment expenses e.g. restaurants, streaming services, gym memberships, travel, hobbies

- Savings and donations e.g. TFSA contributions, RRSP contributions, emergency savings, charitable donations

Second, write down your monthly household income after taxes (this is the amount your household actually takes home each month).

Finally, allocate your income across the four categories above so you can clearly see what proportion of your budget is going toward each area of spending. This might look something like the following:

ℹ️ Note

A common guideline in personal finance is to aim for roughly 45% of your income on household expenses, 30% on lifestyle spending, and 20% on savings and debt repayment.

Calculation 2: How much can you afford monthly

Next, you need to work out how much you can afford to spend on housing each month without putting yourself into a financially risky position. There are two simple rules that you can use to do this:

Affordability rule one

As a general rule, your monthly housing costs should be no more than 32% of your average gross (before-tax) monthly income. For example, let’s say that your monthly household income is $12,000 before tax, you should spend no more than $3,840 on housing costs. This is known as your Gross Debt Service Ratio (or GDS ratio).

Your housing costs include mortgage payments, property taxes, heating expenses, condo fees (if applicable), home owner association fees (if applicable), and site rent for leasehold tenure (if applicable).

ℹ️ Note

Lenders may qualify you for a mortgage with a higher GDS ratio. However, this is often not a financially prudent decision because it can leave you “house poor”, meaning that too much of your monthly income goes toward housing expenses, leaving less room in your budget for savings, emergencies, retirement contributions, and everyday living costs.

Affordability rule two

As a general rule, your average monthly debt load i.e. the amount of money that you spend on credit card payments, car loans, and other lines of credit, should not be more than 40% of your average gross (before tax) household monthly income. For example, if you have a have a monthly household income of $12,000, then you should not spend more than $4,800 per month on debt repayments. This percentage is known as your total debt-to-income or total debt service (TDS) ratio.

Your total monthly debt load includes housing costs (everything included in affordability rule one), plus car loans or leases, credit card payments, lines of credit, and other mortgage payments.

ℹ️ Note

In Canada, the Canada Mortgage and Housing Corporation (CMHC) restricts homebuyers to a 39% GDS ratio and to a 44% TDS ratio to qualify for an insured mortgage.

This essentially restricts homebuyers from qualifying for a mortgage with a A Lender when the down payment is less than 20% of the home value. For more information on this, read How much is a down payment for a house.

Calculation 3: Figure out upfront costs

Your upfront costs are the total amount you need to purchase the property. This includes the purchase price (market value minus any major repairs or renovations required) plus the closing costs.

Closing costs are the additional expenses associated with completing the purchase of a home. While the exact amount is difficult to know at the beginning of your home-buying journey, most buyers should budget approximately 2–4% of the purchase price.

- Land Transfer Tax (also known as the welcome tax)

- Notary fees

- Title insurance

- Home inspection

- Home appraisal

- Mortgage insurance premium (if <20% down)

- Property tax adjustments

- Utility adjustments

- Moving costs

The maximum home price you can afford is determined by adding your down payment to the maximum mortgage amount you qualify for based on affordability rules.

ℹ️ Note

For more information on closing costs and to calculate how much mortgage you can afford, check out:

2. Get mortgage pre-approval

You are now ready to set up a call with your lender or mortgage broker to discuss how you can finance your home purchase. On this call, they will explain what information they need from you to get mortgage pre-approval. They will also discuss with you the interest rates that they are prepared to offer you, and the terms and conditions of their mortgage products.

It is very important to get pre-approval before you start house hunting. This is because it helps to define your house search in terms of what you can realistically afford, so that you don’t waste a lot of time visiting homes that are outside of your price range. And whilst getting pre-approved does not guarantee that you will get a final approval, it does make it more likely and there are things you can do to protect yourself from being denied your mortgage at closing.

In this section, we will explain some of the key mortgage terms that you need to be aware of, how to get pre-approved, and how to get the best rate for your mortgage so that you can pay the lowest amount of monthly payments and reduce the cost of financing by literally tens of thousands of dollars.

To start with, let’s get an understanding of the key mortgage terms so that we can understand precisely how mortgages work and the different types that you can get.

Key mortgage terms to be aware of

There are several different types of mortgage that you can get. To evaluate them, you need to understand certain key terms.

Amortization Period

Total time needed to fully repay your mortgage

What it means

The amortization period is the total amount of time it will take to fully repay your mortgage. In Canada, lenders will normally give you an option for a 20, 25, and 30 year amortization period.

Why it matters

Longer amortization periods reduce your monthly payments, but increase the total amount of interest paid over time.

Mortgage Term

Length of time your mortgage contract remains in effect

What it means

The mortgage term is the length of time your mortgage contract remains in effect before it must be renewed or renegotiated.

Things to know

In Canada, the most common mortgage term is between 3–5 years.

Payment Schedule

How often you make mortgage payments

What it means

The payment schedule is how often you make your mortgage payments. In Canada you normally have a choice between monthly, bi-weekly, and weekly payments.

Things to know

Some lenders also offer accelerated payment options, which can help you pay off your mortgage faster and reduce interest costs over time.

Interest Rate

Cost of borrowing money for your mortgage

What it means

The interest rate tells you how much interest your lender charges you to borrow money for your mortgage. Your monthly mortgage payment is then divided between paying interest and repaying a portion of the principal.

Example

For example, you might have a monthly mortgage payment of $1,500, where $900 goes toward interest charged by the lender, while $600 goes toward paying down the principal balance of your mortgage.

Types of Interest Rate

Fixed, variable, or capped variable

Fixed rate

The rate does not change for the term of the mortgage.

Variable rate

The interest rate fluctuates with market rates.

Protected (or capped) variable rate

The interest rate fluctuates but will not rise over a pre-set cap written into your mortgage contract.

Open and Closed Mortgages

Different rules around early repayment

Open mortgage

An open mortgage allows you to repay the mortgage in full, refinance it, or make large lump-sum payments at any time without paying a prepayment penalty.

Closed mortgage

A closed mortgage limits how much you can prepay each year and usually charges a penalty if you break the mortgage term early.

Conventional and High-Ratio Mortgages

Based on the size of your down payment

Conventional mortgage

A conventional mortgage is one where the loan amount is equal to or less than 80% of the property’s value, meaning the borrower provides a down payment of at least 20%.

High-ratio mortgage

A high-ratio mortgage is one where the loan amount is greater than 80% of the property’s value, meaning the borrower provides a down payment of less than 20%.

Down Payment

Money you pay upfront toward the purchase

What it means

The down payment is the portion of the home’s purchase price that you pay upfront using your own money. The remaining amount is borrowed through a mortgage.

Things to know

In Canada, the minimum down payment required depends on the purchase price of the property.

Pre-payment Options

Ability to pay down your mortgage faster

What it means

Pre-payment options give you the chance to make extra payments towards your principal, or to pay off your mortgage early without incurring a penalty.

Portability

Transfer your mortgage to another property

What it means

A portable mortgage allows you to transfer or switch your mortgage to another home with little or no penalty when you sell your existing home.

Mortgage Stress Test

Ensures you can afford higher future payments

What it means

You will generally need to pass a stress test in order to qualify for a mortgage with a federally regulated lender in Canada.

Things to know

Lenders qualify you using an interest rate that is higher than the actual rate in your mortgage contract. This helps ensure you can still afford your payments if interest rates rise in the future.

Credit Score

A rating lenders use to evaluate borrowing history

What it means

Your credit score is a three digit number between 300–900. Lenders use this score to evaluate how reliably you have managed credit and debt in the past.

Things to know

A higher credit score indicates to lenders that you are more likely to repay your debts compared to borrowers with lower credit scores.

Different types of lenders

You can get a mortgage from several different types of lenders, which can generally be grouped into three broad categories. Each type of lender is willing to finance borrowers with different risk profiles, based largely on factors such as credit score, income stability, debt levels, and down payment size.

| Type of Lender | This includes | Examples | Work with borrowers with credit scores of |

| A Lenders | Banks, credit unions, prime monoline lenders | RBC, Scotia Bank, Desjardins, MCAP. | 660+ |

| B Lenders | Subprime monoline lenders | Home Trust, Equitable Bank, CMLS Financial. | 500+ |

| Private Lenders | Mortgage Investment Corporations (MICs) | Castleton Hypothèques-Mortgages, Guardian Financing. | 300+ |

Each lender will evaluate you based on your likelihood of repaying the mortgage. Traditionally, A-lenders offer the best rates and terms because they typically lend to borrowers with “Good” or “Excellent” credit scores, stable income, and stronger overall financial profiles.

B Lenders and Private Lenders, meanwhile, are often willing to work with borrowers who may not qualify with traditional banks due to lower credit scores, higher debt ratios, inconsistent income, recent credit issues, or other financial challenges.

Because these lenders take on more risk, they tend to charge higher interest rates and may offer more restrictive terms. They also generally require larger down payments, since borrowers who do not qualify for insured financing usually need at least 20% down for alternative lending solutions.

Get Your Credit Score – Know Who You Can Work With

Use LoansCanada.ca to find out your credit score for free.

How to get the best mortgage for you

The best mortgage is one that you can comfortably afford, keeps your housing costs within a sustainable portion of your income, minimizes unnecessary borrowing costs, and still provides enough financing to meet your homeownership goals.

For example, if you are a first-time home buyer with a fixed monthly income. It might make sense to take a standard 25-year fixed rate mortgage with a 5 year term. This gives you some stability and, it makes it easy to budget for.

However, you may want the flexibility to make extra payments toward your mortgage since, this can dramatically decrease the interest paid and shorten the time it takes to become mortgage-free. Most A Lenders offer the option to make extra payments however, this privilege is often capped to a 10% to 20% of the original mortgage amount.

To get the best mortgage for you, you need options. The best way to do this is to get pre-approved by several banks and credit unions like RBC, Scotia Bank and Desjardin. At the same time, you can also reach out to a mortgage broker and see if they are able to get you a better deal. To find a reputable mortgage broker, you can use Immovision Broker Finder tool to get a list of the top mortgage brokers in Quebec.

⚠️ Important

When comparing different mortgage offers, make sure to factor in any administration or lender fees, as these can increase the overall cost of borrowing.

Traditional banks and credit unions typically do not charge administration fees on standard mortgages, while many alternative lenders, B Lenders, and private lenders often do.

What documents do you need for pre-approval

When you apply for a mortgage pre-approval, the lender is deciding whether they are comfortable lending you a large amount of money. To do this, they need to verify your identity, confirm your income, review your financial situation, and assess your ability to repay the mortgage.

While requirements vary by lender and employment type, you will commonly be asked to provide the following documents:

Proof of Income

Proof of Down Payment & Assets

Existing Debts & Financial Obligations

Identification & Personal Information

Mortgage insurance

Mortgage insurance exists to protect the lender from financial loss if you default on your mortgage. For example, imagine you borrow $300,000 from a bank, make your mortgage payments for two years, and then stop making payments. If the mortgage is insured, the lender can recover some or all of its losses through the insurance provider.

In Canada, mortgage default insurance is typically provided by Canada Mortgage and Housing Corporation, Sagen, and Canada Guaranty. Your lender typically chooses the insurance provider and arranges the coverage on your behalf during the mortgage approval process.

Even though mortgage insurance exists to protect the lender, the borrower typically pays for it. In Canada, it is generally mandatory whenever the down payment is less than 20% of the purchase price.

The cost of mortgage insurance is calculated as a percentage of the mortgage amount. The percentage depends on how much money you put down. For example:

- Purchase price: $500,000

- Down payment: $50,000 (10%)

- Mortgage amount: $450,000

- Mortgage insurance premium rate: 3.1%

- Insurance premium: $13,950

So the total cost mortgage insurance in this case is $13,950 plus any taxes.

Unlike many other purchases, federal GST does not apply to mortgage insurance premiums. However, in Quebec, borrowers must pay a 9% provincial tax on the mortgage insurance premium at closing. This means that the total cost of the mortgage premium in our example is:

- QST payable at closing: $1,255.50

- Insurance premium added to mortgage: $13,950

- New mortgage balance: $463,950

As you can see from this example, even though the buyer made a 10% down payment of $50,000, the final mortgage balance becomes approximately 92.8% of the home’s purchase price on day one. This means that the buyer loses roughly 3% of their down payment on day one.

ℹ️ Note

As you can see from this example, a buyer may put down 10% of the purchase price but still owe almost 93% of the home’s value immediately after closing because the insurance premium is financed into the mortgage.

This is one reason why some buyers choose to save a 20% down payment and avoid mortgage insurance altogether. Others intentionally target a 15% down payment, because this is where insurance premiums drop significantly. For example:

- 10–14.99% down: 3.1% premium

- 15–19.99% down: 2.8% premium

- 20%+ down: No mandatory mortgage insurance

First time buyer incentives

Over the past two decades, home prices have risen much faster than wages, making it harder for first time buyers to enter the market.

To help bridge this gap, the federal, provincial, and municipal governments offer a range of programs and incentives that can reduce the upfront cost of buying a home for first time buyers. If you use these strategically, you can save tens of dollars when buying a house in Montreal. Below is a breakdown of the main incentives available to buyers in Montreal.

| Program | Level | What it does |

|---|---|---|

| Federal incentives | ||

| First-Time Home Buyers’ Tax Credit (HBTC) | Federal | Provides a non-refundable tax credit to help offset some of the closing costs associated with buying your first home. |

| RRSP Home Buyers’ Plan (HBP) | Federal | Allows first-time buyers to withdraw funds from their RRSP tax-free to use toward a down payment. |

| First Home Savings Account (FHSA) | Federal | A registered savings account that allows eligible buyers to save for a home with tax-deductible contributions and tax-free withdrawals. |

| Registered investment accounts | Federal | Buyers may also use savings held in accounts such as TFSAs, RRSPs, or non-registered investment accounts toward their down payment. |

| GST Rebate for First-Time Buyers of New Homes | Federal | Proposed federal program intended to eliminate GST on newly constructed homes under $1 million purchased by eligible first-time buyers. |

| Provincial incentives | ||

| Quebec First-Time Home Buyers’ Tax Credit | Provincial | Quebec offers a provincial tax credit to help first-time buyers offset some of the costs associated with purchasing a property. |

| QST/GST New Housing Rebate | Provincial / Federal | Buyers of newly built homes may qualify for rebates on a portion of the GST and QST paid on the purchase price. |

| Municipal incentives | ||

| Montreal Home Purchase Assistance Program | Municipal | Financial assistance program that may provide grants or support to eligible homebuyers purchasing property in Montreal. |

There are also eco-friendly housing programs available for energy-efficient homes and renovations. These include the CMHC Eco Improvements and Eco Plus Program, the Canada Greener Homes Loan, and the Green Home Loan Insurance Incentive, and several other green incentives.

🎓 Learn more about other types of financial incentives

3. Make a list of properties you want to visit

Now that you have a mortgage pre-approval, you know your budget and can start thinking seriously about the type of home you want to buy. Since buying a home comes with significant upfront costs, it is important to choose a property that will suit your needs not just today, but for the next 5–10 years.

What to look for in a home?

It can be helpful to write down the key things that matter most to you in an ideal home — such as location, size, features, and lifestyle. This can keep your search organized and help ensure you don’t overlook something that may later prove important.

Location

Do you want to live in the heart of downtown, or by the beach in Verdun? Is a outdoorsy setting like L’Île-Perrot what you are after? Or do you want to be close to transport links so that you won’t need to buy a car?

Size

How many bedrooms do you need? Do you need a space for a home office, or for extra storage? Do you want an indoor garage, or are you okay with street parking?

Features

Do you want a south facing property, that gets lots of sunlight? Can you make do with a terrace, or do you want a garden? Do you need a bath tub in the bathroom? Do you want modern renovations, or are you okay to make home improvements yourself?

Lifestyle

Do you have children, or are you planning to have children soon? Are local schools important to you? Do you have teenagers who will be moving out soon? Are you looking to downsize for retirement? Do you need to be close to parks, outdoor walking spots, or day cares?

⏰ Take your time when looking for a home

As a general rule, buyers should expect to stay in a home for at least 5 years before selling. This is because the upfront costs of purchasing a property — such as the welcome tax, notary fees, inspection costs, mortgage insurance, and moving expenses — are largely unrecoverable. In Montreal, these costs typically add up to between 2%–4% of the purchase price.

If you buy and sell too quickly, there is a risk that property values may not have increased enough to offset these costs. In some cases, this can leave you losing money on the sale or even underwater on your mortgage.

Types of home ownership

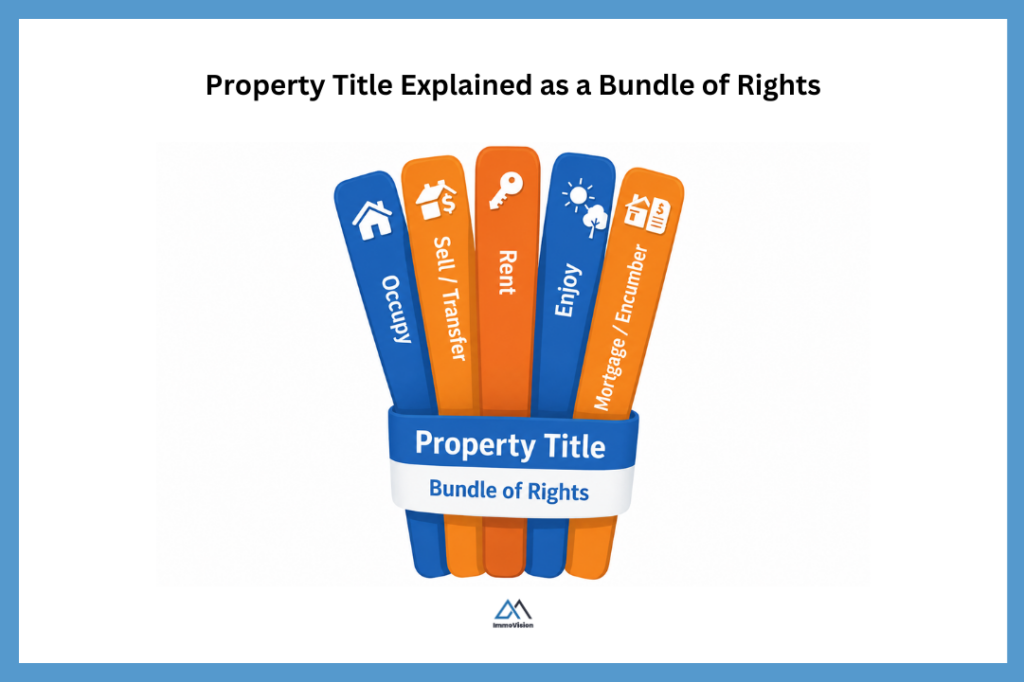

Owning a property really means owning a collection of legal rights to the property. For example, you may have the right to live in the property, rent it out, renovate it, sell it, or pass it on to someone else. This collection of rights is bundled together into something we call a “property title“.

A simple way to think about the property title is as a bundle of sticks. Each stick represents one right. If you hold the entire bundle, you own all the rights to the property. But sometimes you only buy or receive some of those rights rather than all of them.

Different combinations of rights create different types of legal ownership. In Quebec, there are four types of home ownership. These are listed out below.

Freehold

A freehold is when you buy the rights to the property and the land it sits on.

The most common example is a single-family home. Freehold properties tend to be more expensive and often appreciate faster due to limited land supply.

Leasehold

A leasehold means you own the property but not the land. You pay to lease the land for a fixed period (often 99 years), and must renegotiate once the lease expires.

Leaseholds can be prepaid or non-prepaid.

Condominium (Strata)

A condominium (or strata) is shared ownership where you own your unit and a share of common areas like hallways, elevators, and lobbies.

In Quebec, condos can be divided or undivided, affecting ownership structure and governance.

Co-operative (Co-op)

In a co-op, you buy shares in a corporation that owns the building. Those shares give you the right to occupy a specific unit.

This structure exists in Quebec but is less common than other ownership types.

🎓 Learn more about ownership types in Quebec

For more information on the different types of property ownership, read:

Different types of property

In Canadian census data, housing is classified along two independent dimensions: structure type and tenure (ownership type). We have already discussed the different ownership types, below is are the structure types that you can buy, along with the pros and cons of each.

Single-Detached House

A standalone residential building that does not share walls with any other dwelling and sits on its own lot.

Advantages

- Maximum privacy

- Full control of building and land

- No shared walls or condo fees

- Typically stronger long-term land value appreciation

Disadvantages

- Highest purchase price

- Full maintenance responsibility

- Higher property taxes

- More exposure to market fluctuations

Semi-Detached House

A dwelling that shares one common wall with another unit, forming a pair of houses.

Advantages

- More affordable than detached homes

- Private entrance and yard

- Lower maintenance costs

Disadvantages

- Less privacy than detached homes

- Potential shared wall noise

- Limited renovation flexibility in some cases

Row House (Townhouse)

A series of attached homes sharing walls on both sides, each with separate entrances.

Advantages

- More affordable entry into ownership

- Efficient use of land

- Often located in urban areas

- Lower maintenance than detached homes

Disadvantages

- Shared walls reduce privacy

- HOA or condo fees may apply

- Less land ownership and control

Apartment / Condominium

A unit within a multi-unit building where owners share common areas and amenities.

Advantages

- Lower entry cost

- Access to amenities

- Lower exterior maintenance responsibility

- Often centrally located

Disadvantages

- Monthly condo fees

- Less control over building decisions

- Restrictions on renovations

- Shared governance through condo boards

Other Single-Attached / Mixed Structures

Includes converted houses, duplexes, and smaller multi-unit dwellings not fitting standard categories.

Advantages

- Often more affordable

- Potential rental income opportunities

- Flexible layouts in some cases

Disadvantages

- Can be harder to finance

- Inconsistent classification

- Potentially higher maintenance complexity

Movable Dwelling

A movable residential structure such as a mobile home or trailer home.

Advantages

- Lowest cost of entry

- Flexibility of location in some cases

- Lower property taxes

Disadvantages

- Higher depreciation risk

- Financing limitations

- Possible land lease issues

- Lower long-term appreciation potential

🎓 Learn more about the different property types in Quebec

- What are the different types of house in Quebec (2026)

- What is a detached house? All You Need To Know (2026)

- What is a semi-detached house? All you need to know (2026)

- What is a Townhouse? All you need to know (2026)

- What is a plex? Everything you need to know (2026)

- What is a duplex? All you need to know (2026)

Home buying vs home building

Another choice that you have is between:

Newly built home

A newly built home is a residential property that has been recently constructed and is purchased directly from a builder or developer. Unlike resale properties, new builds may be subject to additional taxes and regulatory requirements at the time of purchase.

Many buyers assume that a newly built home will require minimal maintenance and few renovations during the first 5 to 10 years, particularly for major systems such as roofing, plumbing, and electrical work. While this can often be the case, it is not guaranteed.

Because the property has not been previously lived in, there is no occupancy history to reveal potential issues such as settling defects, workmanship inconsistencies, or early-stage system failures. As a result, construction quality can be difficult to assess in advance, and some buyers may encounter unexpected defects or finishing issues after moving in.

That said, when construction quality is high and the builder is reputable, a newly built home can offer the advantage of modern materials and systems with relatively low maintenance requirements in the early years of ownership.

A previously owned home

A previously owned home (or “resale” home) is one that has been lived in by at least one prior owner before being resold.

Unlike newly built properties, resale homes come with an established usage history. This means buyers can evaluate the property based on real-world performance, including how the building has aged, how systems such as plumbing, heating, and electrical have held up, and whether any renovations or repairs have already been completed.

However, resale properties may require additional renovation or maintenance depending on their age and condition. Buyers may also encounter outdated building systems or design features that do not meet modern construction standards for energy efficiency and indoor air quality.

Build your own home

If you want to control the size, layout, and design of your home, you may decide to build it yourself. This option offers the highest level of customization, but it also requires a significant investment of time, money, and effort.

It typically involves a more complex financing structure than a standard purchase, such as construction financing or a specialized mortgage arrangement. In addition, you will need to secure land (either through purchase or, in some cases, long-term lease agreements), obtain the necessary building permits, and comply with local planning and zoning regulations.

For these reasons, building a home is generally considered a more advanced option and is not suitable for inexperienced buyers or those looking for a straightforward purchase process.

Where best to search?

In Montreal, more than 90% of buyers start their property search in Google, using terms like “houses for sale in Montreal,” “Verdun property listings,” or similar location-based queries.

From there, buyers find listings that are published via listing agents through the MLS® (Multiple Listing Service) and displayed across major real estate platforms such as Realtor.ca, DuProprio, and other third-party websites.

Each of these platforms offers its own set of search filters, allowing buyers to narrow down properties based on criteria such as location, price range, property type, number of bedrooms, and lifestyle features. Most platforms also allow users to create automatic alerts, notifying them whenever a new property matching their criteria is listed on the market.

⚠️ Warning

The real estate agent shown on a property listing is either the listing agent, who represents the seller, or, on some platforms, a promoted agent who has paid for increased visibility in search results.

If you’re looking to buy a home in Montreal, we recommend working with a buyer’s agent. However, it’s important to do your own research to find one who is genuinely skilled and a good fit for your needs. We cover how to do this in the next section.

4. Find a buyer’s broker

A buyer’s broker (or buyer’s agent) is a realtor who helps the buyer purchase a property.

In Quebec, there are normally two agents on every transaction: a buyer’s agent whose job it is to represent the interests of the buyer and a seller’s agent, whose job it is to represent the interests of the seller. The reason that you have two brokers on the transaction are that, these transactions tend to be highly advesarial, meaning that the seller’s agent will do whatever they can to get the best deal for their client. And so, as a buyer, if you are not represented by your own agent, then you can easily end up overpaying by tens of thousands of dollars for a property.

A buyer’s agent meanwhile is there to make sure that you:

✔ Avoid paying significantly more than a property’s fair market value

✔ Identify potential red flags before making an offer

✔ Navigate the buying process and reduce costly mistakes

How to avoid overpaying

A property’s market value is generally determined by comparing it to similar properties that have recently sold in the same area, then adjusting for differences such as renovations, condition, size, location, and any repairs or upgrades required.

A good buyer’s agent will help you determine the fair market value of a property before you make an offer. To do this, they will typically conduct a CMA (Comparative Market Analysis).

The process usually begins with a review of important documents, such as the seller’s declaration, which outlines any known defects or other issues that could materially affect the property’s value.

This may include things such as references to unpaid property taxes, zoning violations, hypothec of construction, and so on. However, a good buyer’s agent will also look in the Quebec Land Register to learn more about the property, its owners, and possible reasons for selling.

After reviewing the documentation, the broker will conduct an on-site walkthrough of the property with you to assess its overall condition and quality. This also allows them to verify whether the property matches the seller’s description and to look for any potential risk factors, defects, or issues that may not have been disclosed in the seller’s declaration.

Finally, the broker will analyze recent and historic sales of comparable properties in the area and use this to make an adjustment based on differences in features, condition, renovations, lot size, location, and other relevant factors to estimate the property’s fair market value.

Once the valuation is complete, your buyer’s agent will review the results with you and help structure an offer that is competitive enough to be accepted, while also helping you avoid overpaying.

A good buyer’s agent can also help negotiate better terms, such as a lower purchase price, seller-paid repairs, included appliances or fixtures, favourable occupancy dates, and set pre-purchase inspection protections and conditions related to financing. Most buyer’s agents also carry latent defect insurance for their clients. This is to help safeguard you against hidden defects discovered after taking possession of the property.

ℹ️ Note

Real estate valuations require highly localized and property specific knowledge.

For instance, a condo in downtown Montreal vs a duplex in the Plateau vs a detached home in the West Island. These all come with very different considerations that effect their valuation.

For instance, construction methods and materials vary by region, as do zoning bylaws, and common property issues can vary significantly depending on the property type.

That is why finding someone with experience in the neighbourhood and property types is an absolute must.

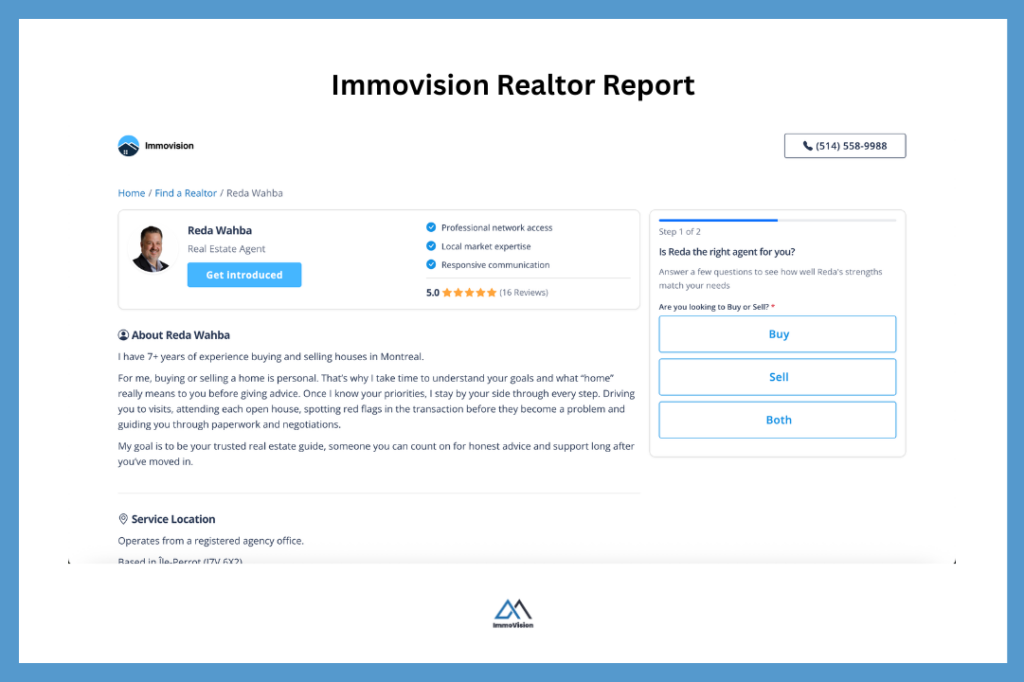

How to find a local real-estate expert

To find a broker that is an expert in your local market, you can use several methods.

Friend and family referrals:

Many people start by asking friends or family members for recommendations. While referrals can be helpful, every buyer’s situation is different. In addition, highly sought-after realtors are often very busy, which can sometimes mean less availability and attention throughout the process.

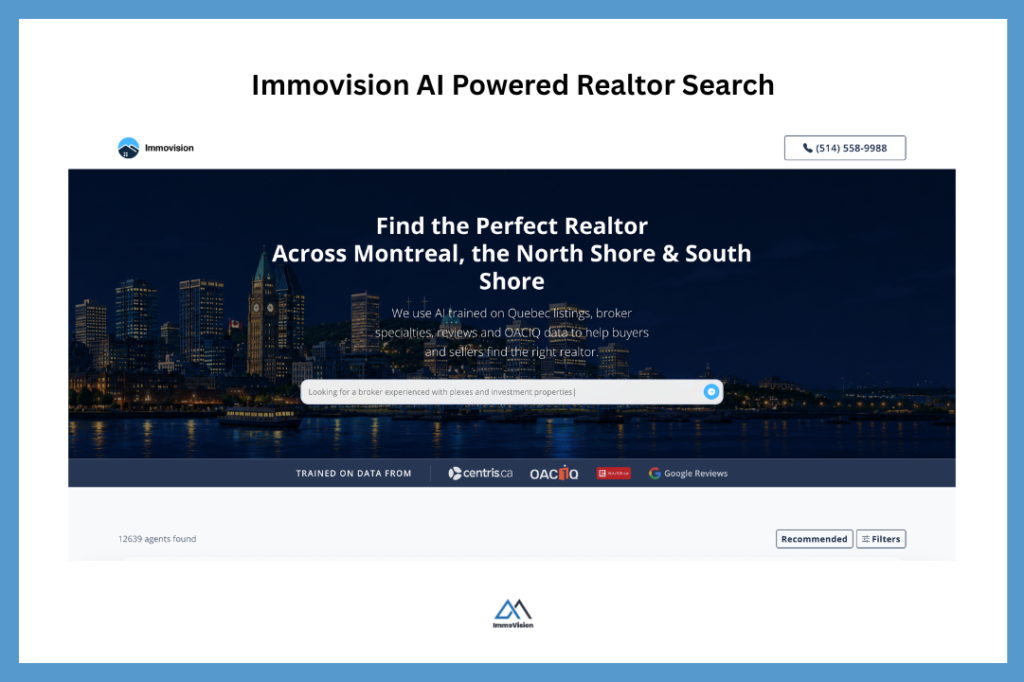

AI-powered search tools:

New AI-driven search platforms can also help match buyers with suitable brokers. Immovision’s AI matching tool analyzes your goals, budget, preferred neighborhoods, and property type to help identify agents who may be a strong fit for your needs.

Broker matchmaking services:

Some buyers prefer a more hands-on approach through a matchmaking service. With Immovision’s AI-assisted matchmaking process, we can personally contact agents, review their current projects and activity level, provide insight into their market expertise, and even give you a tailored list of questions to ask before choosing who to work with.

Get Broker Performance Report (Free)

Get a list of the top 3 agents for your area, for free.

Interview your realtor

Whichever method you choose, it’s important to interview your realtor before deciding to work with them. For a buyer’s agent, you should consider the following points:

- Experience in your type of property

- Knowledge of your local area

- Strong performance stats

- Good, verified reviews

- Professional network

- Effective communication

- Personal comfort

- Red flags

Using the Immovision AI Agent Finder, you can search an agent’s name to review their professional background, including any regulatory violations or disciplinary records, as well as the training and certifications they have completed.

You can also see the neighborhoods and property types they are currently active in, along with details such as the date of their most recent transaction in the area. An example of this is shown below.

🎓 Learn how to interview a realtor

For more information on how to interview a realtor to buy a house in Montreal, read:

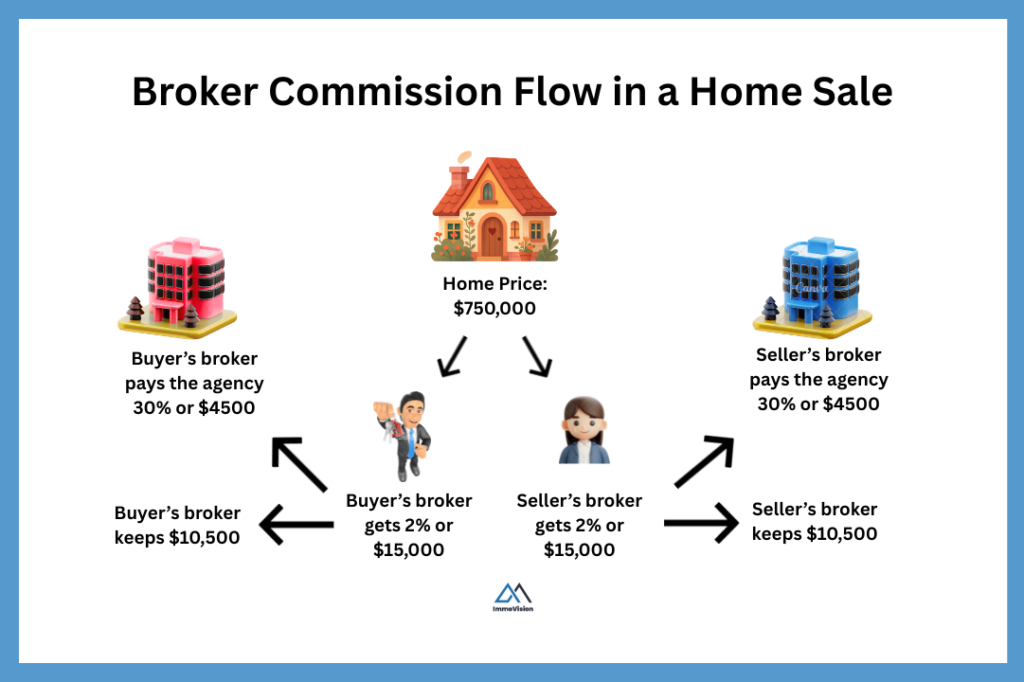

How much does a buyer’s agent cost

Buyer’s agents typically charge around 2% of the final transaction amount. For instance, if you purchase a property for $500,000, a buyer’s agent may expect to earn approximately $10,000 in commission. This amount is typically split between the buyer’s brokerage and the individual agent. However, an agent may also charge additional amounts if the seller’s agent does not agree to share the full commission, or through additional administrative or service fees.

At first glance, this can seem like a large amount of money for reviewing a few documents and accompanying you on a property walkthrough. However in reality, most buyers will visit somewhere between 10 and 20 properties before they decide to make an offer. In each case, the realtor needs to coordinate visits, review property documents, analyze comparable sales, communicate with the listing agent, and accompany you during showings. By the end of the process, a good realtor often does far more work behind the scenes than most buyers initially realize.

That said, not all agents provide the same level of service. Some may simply help you complete the promise to purchase without thoroughly analyzing the property’s market value, condition, resale potential, or possible risks beforehand. In situations like this, you may be able to negotiate a reduction in the buyer broker’s commission or fees. If you feel that the agent is not providing sufficient value or representation, you can often end the relationship before signing a formal buyer brokerage agreement or exclusivity contract.

💡 Buyer's Tip

If you are not sure where you are going to buy yet, don’t sign a contract with a buyer’s agent until you are ready to make an offer. This way, you can use different brokers depending on where specifically you are searching.

To find these brokers in Montreal, use Immovision AI Agent Finder for free.

5. Visit the homes

If you decide to work with a broker, you should visit the homes with them, so that they can help you perform a visual inspection of the property. In this section, we look at:

How to prepare for a property visit

Before visiting a property, you should:

- Review the seller’s declaration

- Ask your agent to do a title search

- Ask your agent about the area

- Put the list price of the property in context

- Know the number of days on market

Review the seller’s declaration

The seller’s declaration is a document that outlines everything the seller believes could affect the property value. This includes known issues, past repairs, deferred maintance, renovations, and other important details, like rising condo fees. It’s best to review the declaration alongside the property photos before scheduling a visit. Doing this can help you identify potential red flags that you might want to take a closer look at, and to estimate future costs.

Ask your agent to do a title search

A title search is an important step in the home-buying process, and your notary will do a very thorough title search before the transaction is complete. However, you can also ask your agent to do a title search before you visit the home. To do this, they will need to review records in the Quebec Land Register, which is a public database containing legal information about properties in Quebec.

By searching the property, you can often see past sale prices and ownership history, as well as identify potential issues such as unpaid property taxes, legal claims, construction hypothecs, servitudes, permits, or municipal bylaw infractions. This information can help you better understand the property’s history and may also provide useful leverage during negotiations if you decide to submit an offer to purchase.

Ask your agent about the area

You should also ask your buyer’s agent about the surrounding area, including local schools, daycares, upcoming developments, public transit projects, and recreational facilities. An experienced local broker can also tell you whether the area has benefited from major municipal investment or redevelopment programs. For example, in 2008, Griffintown got approval approximately for roughly $1.3 billion in investment. This money was used to transform the area from a neglected industrial district into one of Montreal’s fastest-growing (and now most expensive) neighbourhoods.

Put the list price of the property in context

An experienced local broker can often estimate a home’s value simply by analyzing its list price compared to similar properties in the area. In Montreal, many homes are listed using predictable pricing strategies, allowing experienced agents to gauge the seller’s expectations before negotiations begin. Local brokers also become familiar with each other’s negotiation styles and attention to detail, which can sometimes create opportunities to renegotiate the price or request compensation for overlooked repairs.

Know the number of days on market

The average detached, single-family home in Montreal typically stays on the market for around 30 days. However, this changes constantly depending on market conditions and can vary significantly from one neighbourhood to another.

Buyer’s agents have access to up-to-date Quebec MLS data for different property types, broken down by neighbourhood and sector. This allows them to tell you the average days on market for the exact area you are considering. You can then compare this with how long the property you are viewing has on the market for.

Homes that remain on the market longer than average may be overpriced. In some cases, you may also notice from the listing photos that the property has not been marketed effectively, which can reduce buyer interest and create negotiating opportunities.

How to do a property visit

As you walk through the property, your goal is not just to decide whether you like the home — it is also to evaluate the overall condition of the building, identify potential problems, and estimate how expensive repairs could be.

Try to approach the visit like a checklist. As you move through each area of the property, make notes about visible issues, signs of neglect, and anything that may require repair or replacement in the near future. Even rough estimates can help you better understand the true cost of owning the property.

A good buyer’s agent will usually do this far better than the average buyer, but having your own understanding can help you ask better questions, negotiate more effectively, and avoid overlooking major issues.

During your visit, pay attention to:

Exterior of the House

Structure, grading, drainage, and visible movement

Exterior of the House

Structure, grading, drainage, and visible movement

Start by walking completely around the property. Look carefully at the condition of the structure, grading, drainage, and visible signs of movement or water infiltration.

Watch for

- Cracks in the foundation

- Sloping landscaping toward the house

- Water pooling near the foundation

- Damaged brickwork or siding

- Uneven walkways or driveway sinking

- Signs of foundation settlement

Possible repair costs

- Minor crack sealing: $500–$2,000

- Foundation stabilization: $20,000+

- French drain replacement: $15,000–$40,000+

- Exterior waterproofing: $10,000–$30,000+

Roof and Drainage

Roofing materials and water management

Roof and Drainage

Roofing materials and water management

The roof protects the entire structure. Water intrusion from roofing failures can eventually damage insulation, ceilings, walls, and structural framing.

Watch for

- Curling or missing shingles

- Sagging rooflines

- Moss growth

- Damaged flashing

- Overflowing gutters

- Water stains on ceilings

Possible repair costs

- Minor roof repair: $1,000–$5,000

- Full roof replacement: $8,000–$30,000+

- Attic water damage repairs: $5,000+

Living Areas

Interior movement, moisture, and workmanship

Living Areas

Interior movement, moisture, and workmanship

Focus on signs of movement, moisture, or poor workmanship throughout the main living spaces.

Watch for

- Sloping floors

- Cracks around doors and windows

- Uneven flooring

- Musty smells

- Fresh paint covering isolated areas

- Doors that no longer close properly

Possible repair costs

- Cosmetic drywall repairs: $500–$3,000

- Structural floor corrections: $10,000+

- Mould remediation: $5,000–$30,000+

Kitchen

Plumbing, cabinetry, and moisture issues

Kitchen

Plumbing, cabinetry, and moisture issues

Kitchens are expensive to renovate and can also reveal plumbing or moisture problems.

Watch for

- Water damage under sinks

- Soft cabinet bottoms

- Poor water pressure

- Signs of leaks around appliances

- Outdated plumbing

- Improper ventilation

Possible repair costs

- Plumbing repairs: $1,000–$10,000+

- Full plumbing replacement: $10,000–$40,000+

- Kitchen renovation: $15,000–$75,000+

Bedrooms and Bathrooms

Humidity, leaks, and hidden water damage

Bedrooms and Bathrooms

Humidity, leaks, and hidden water damage

Bathrooms are one of the most common sources of hidden water damage.

Watch for

- Loose tiles

- Soft flooring

- Excess humidity

- Black staining around tubs or showers

- Poor ventilation

- Water stains on ceilings

Possible repair costs

- Bathroom leak repair: $1,000–$5,000

- Mould remediation: $5,000–$30,000+

- Full bathroom renovation: $10,000–$35,000+

Windows and Doors

Insulation and structural movement

Windows and Doors

Insulation and structural movement

Problems with windows and doors can indicate structural movement or poor insulation.

Watch for

- Condensation between panes

- Drafts

- Rotting frames

- Doors sticking

- Windows that do not open properly

Possible repair costs

- Window replacement: $500–$2,000 per window

- Exterior door replacement: $2,000–$5,000

- Structural corrections if movement exists: $10,000+

Electrical Panel and Wiring

Safety and insurance concerns

Electrical Panel and Wiring

Safety and insurance concerns

Watch for

- Fuse panels

- Knob-and-tube wiring

- Aluminum wiring

- Flickering lights

- Burn marks around outlets

- Overloaded breaker panels

Possible repair costs

- Electrical panel replacement: $3,000–$6,000

- Knob-and-tube replacement: $10,000–$40,000+

- Aluminum wiring remediation: $5,000–$20,000+

Heating and Cooling Systems

Major mechanical systems

Heating and Cooling Systems

Major mechanical systems

Watch for

- Older furnace or boiler systems

- Uneven heating

- Strange noises

- Rust or corrosion

- Poor maintenance records

Possible repair costs

- Furnace replacement: $5,000–$12,000+

- Heat pump installation: $7,000–$20,000+

- Boiler replacement: $10,000–$25,000+

Basement and Foundation

Water infiltration and structural issues

Basement and Foundation

Water infiltration and structural issues

Watch for

- Water infiltration

- Efflorescence

- Cracks in foundation walls

- Musty smells

- Sump pump issues

- Uneven basement floors

- Orange sludge in sump pits

Possible repair costs

- Crack injections: $500–$2,500

- Waterproofing: $10,000–$30,000+

- French drain replacement: $15,000–$40,000+

- Pyrite remediation: $20,000–$50,000+

- Foundation reconstruction: $50,000+

Backyard and Exterior Structures

Decks, garages, fences, and retaining walls

Backyard and Exterior Structures

Decks, garages, fences, and retaining walls

Watch for

- Rotting wood

- Leaning fences

- Cracked retaining walls

- Unsafe balconies or decks

- Poor drainage near structures

Possible repair costs

- Deck replacement: $5,000–$20,000+

- Retaining wall replacement: $10,000+

- Garage structural repairs: $10,000–$50,000+

💡 Buyer Tip

Consider taking a clipboard, notepad or tablet around with you, so that you can note down the repairs that you might need to make as you go. You can then make an estimate of the costs later.

What to do after your visit

Depending on the size of the property, a visit will typically last around 15 to 25 minutes. If you are visiting multiple homes, it is important to keep organized notes about each property, including your first impressions, potential concerns, estimated renovation costs, and how each property compares against your requirements.

Take the opportunity to discuss the property with your broker and compare their observations against your own notes. An experienced buyer’s broker may identify issues, risks, or future costs that you may have overlooked or underestimated. Your broker should also review documents such as the certificate of location to identify potential legal or zoning concerns, encroachments, easements, or discrepancies between the property and official records.

If there is a home that particularly interests you, ask your broker whether additional inspections or specialized tests may be advisable. Depending on the age, location, and condition of the property, there may be environmental or structural risks that are not immediately visible during a standard visit. These can include flood zone risk, high water tables, pyrite in the foundation, mould, radon gas, iron ochre deposits, or other issues that may require expensive remediation work.

Once you feel comfortable with the property and understand the potential risks and costs involved, the next step is to make an offer to purchase. We will cover this process in the next section.

ℹ️ Note

All of the online photos are taken to make you want to visit, and to present the property in its best possible guide. And so it is often very unlikely that the first home you visit will be the one that you eventually end up moving into. So don’t get dishearted if it takes you some time to find the place that you like.

6. Make a Promise to Purchase

When you have found a house that you like, the next step is to submit an offer to the seller. In Quebec, this is typically done using a document called a Promise to Purchase.

A Promise to Purchase is a standardized legal document that sets out the price and conditions under which you are willing to buy the property. It allows you to specify important terms such as the purchase price, deposit amount, financing conditions, inspection clauses, and proposed closing date.

Once submitted, the seller can accept the offer, reject it, or respond with a counter-offer requesting changes to the terms.

⚠️ Warning

A promise to purchase is a legally binding contract. Once it has been submitted and accepted by the seller, it can be difficult, expensive, and legally complicated to back out of an offer to purchase without valid legal grounds or properly drafted protective conditions.

As such, it is important to fully understand the offer you are making, including the financial obligations, timelines, conditions, and legal consequences associated with the purchase.

Promise to Purchase Templates

The promise to purchase is a standardized legal document developed by the OACIQ (Organisme d’autoréglementation du courtage immobilier du Québec). Several versions of the form exist, each designed for a specific type of transaction or property category. It is important to use the correct template. Below is a list of the different templates and the type of properties that they apply to.

- Residential property with fewer than five units (not a condo) Download PDF

- Condo (divided co-ownership) Download PDF

- Undivided co-ownership (shared ownership) Download PDF

- Immovable / general property Download PDF

- Property sold by the Public Curator Download PDF

Top 6 things to watch out for in your promise to purchase

The promise to purchase is a long and highly technical legal contract with many possible clauses, conditions, and permutations. It also interacts with several other important documents exchanged throughout the buying process, such as the seller’s declaration, certificate of location, condominium documents, inspection reports, and financing conditions.

It is important to remember that the promise to purchase marks the formal beginning of the negotiation process. The way the offer is structured — including the price, conditions, timelines, inclusions, exclusions, and negotiation strategy — can significantly impact both the final purchase price and the terms you ultimately agree to. The financial and legal stakes are therefore very high.

There are many ways for inexperienced buyers to unintentionally expose themselves to legal, financial, or negotiation disadvantages within a promise to purchase. In Quebec, real estate brokers are specifically trained not only to understand the contents of these contracts, but also how different clauses interact with related legal documents and how they may affect both the buyer and seller.

In addition to their formal training, experienced brokers have practical experience handling real-world transaction issues, disputes, failed conditions, inspection problems, financing complications, and negotiation breakdowns. Over time, they also develop familiarity with common legal interpretations, industry practices, and jurisprudence that may influence how certain clauses are understood or enforced in practice.

For these reasons, it is important to work with someone who understands both the legal structure and practical implications of the promise to purchase.

🎓 Learn more about what to watch out for in the promise to purchase

Negotiating your promise to purchase

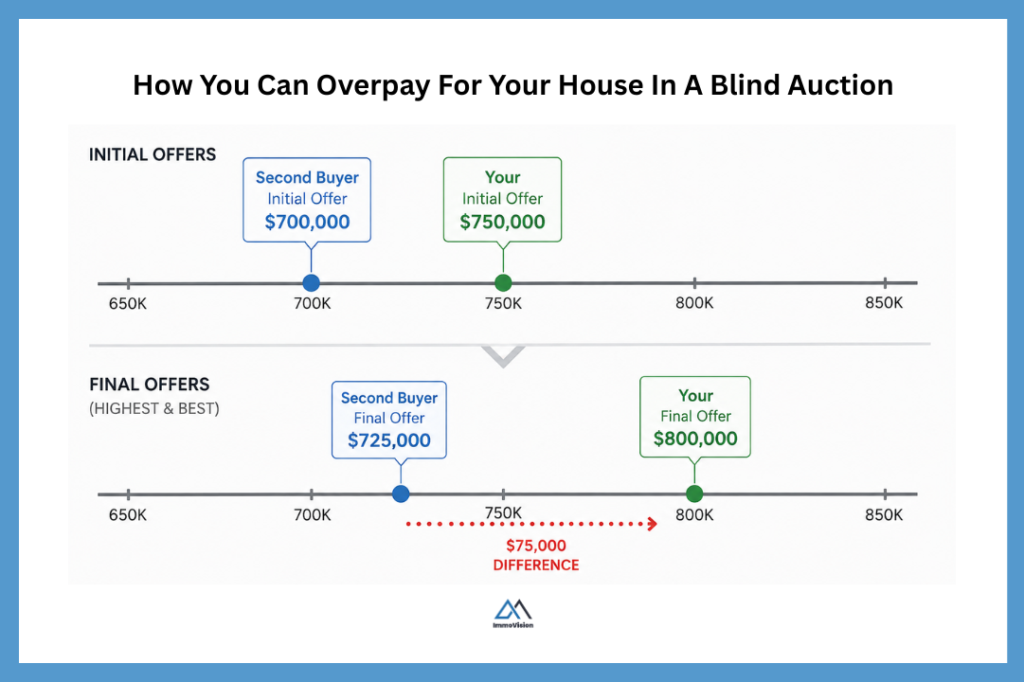

Real estate in Quebec operates using a blind bidding system. This means that when multiple buyers submit offers on the same property, no one can see the competing offers — including the price, conditions, or terms offered by the other buyers.

In competitive situations, negotiations often come down to price. Typically, the seller’s broker will notify all interested buyers that there are multiple offers and ask everyone to return with their “highest and best” offer.

At this stage, many buyers feel pressure to significantly increase their bid. However, it’s important to avoid overpaying unnecessarily. For example, imagine you initially offered $750,000 on a property. You later learn there is another buyer competing for the home, so you decide to increase your offer to $800,000. But what if the competing buyer originally offered $700,000 and only planned to increase to $725,000? In that scenario, you may have paid tens of thousands of dollars more than necessary.

There is no perfect way to know what another buyer is offering in a blind bidding system, so some level of uncertainty is unavoidable. However, there are strategies that can help you remain competitive without overextending yourself.

- Don’t use round numbers

- Use other terms in your offer

- Make sure you don’t overbid market value

One tactic is to avoid round numbers. Many buyers naturally bid in clean increments such as $750,000 or $800,000. Using less conventional numbers — for example bids ending in 1’s or 6’s — can mean that you outbid someone by just $1,000. For example, if a second buyer raises their bid by $25,000, a $26,000 will still beat them.

Another strategy is to strengthen your offer without relying entirely on price. For example, you may choose to improve your terms by offering flexibility on occupancy dates, limiting certain conditions, or including favourable clauses that appeal to the seller.

Most importantly, you should understand the property’s true market value before increasing your offer. A strong buyer’s broker can help you analyze comparable sales and determine what the property is realistically worth in a competitive market. That way, even if you do end up paying more to secure the home, you can feel confident that the price still reflects fair market value and supports your long-term equity in the property.

7. Secure Financing and Complete Inspections

Once your offer has been accepted, you will need to fulfil the conditions that you set in your promise to purchase. The most common things are:

Finanlizing your financing

Once your offer has been accepted, you will meet with your lender to finalize your mortgage financing and review the details of the property. Your lender will then pull your full credit report to confirm that nothing has changed materially since your mortgage pre-approval was issued.

They may also request updated financial and employment information, including:

- An updated letter of employment or job contract

- Recent pay stubs

- Proof of down payment funds

- Bank statements

- Information regarding any new debts or liabilities

ℹ️ Can you be denined financing at closing?

It is important to understand that a mortgage can still be denied after an offer is accepted. Common reasons include:

- Taking on new debt before closing (car loans, credit cards, financing, etc.)

- Changes in employment or income

- Missed payments or a drop in credit score

- Problems uncovered during the lender’s appraisal of the property

- Inability to verify down payment funds

For this reason, buyers should avoid making major financial changes between mortgage approval and closing.

Order a pre-purchase inspection

The OACIQ requires that real estate brokers recommend that buyers obtain a pre-purchase home inspection. The purpose of the inspection is to identify visible issues with the property so that you understand the condition of the home and can estimate the cost of future repairs.

Provided that your Promise to Purchase was made conditional on a satisfactory pre-purchase inspection, this may be your last opportunity to renegotiate the price, request repairs, or withdraw from the transaction before becoming legally obligated to purchase the property.

Examples of issues that may justify renegotiation or cancellation include:

- Major foundation problems

- Structural movement or water infiltration

- Significant roof damage

- Electrical or plumbing systems requiring major replacement

- Evidence of mould or unsafe conditions

Examples of issues that generally would not justify cancelling a purchase include:

- Cosmetic repainting

- Older but functional windows

- Minor maintenance items

- Issues that were already disclosed in the Promise to Purchase or seller declarations

Under Quebec jurisprudence, cancelling a transaction following an inspection generally requires that the defect be serious enough to materially affect the value of the property or the buyer’s willingness to proceed.

A Home Inspection Legally Protects You

A home inspection is designed to help protect you legally and financially by identifying visible issues with the property before you finalize the purchase. Because unexpected repairs and hidden problems can become extremely costly, it is important to hire a qualified and reputable inspector who will thoroughly evaluate the home and clearly explain any concerns.

Order any special tests

Certain areas of Montreal contain older housing stock or environmental conditions associated with known issues such as pyrite, asbestos, radon gas, iron ochre, lead plumbing, or oil tanks. These problems can lead to structural damage, health concerns, insurance complications, environmental cleanup costs, and expensive repairs that may amount to tens of thousands of dollars.

Many homeowners are unaware that these issues exist in their properties because testing has never been performed. For example, the Government of Canada estimates that a significant number of Canadians live in homes with elevated radon levels. Radon exposure is the second leading cause of lung cancer after smoking.

Depending on the location, age, and construction type of the property, your broker may recommend additional testing or expert inspections.

Examples include:

Common in older insulation, floor tiles, ceiling materials, and vermiculite insulation. Removal can be expensive and may require specialized remediation.

A naturally occurring radioactive gas that can accumulate in basements and lower levels of homes. Long-term exposure can create serious health risks.

Found in some concrete slabs and backfill materials in certain regions of Quebec. Pyrite can cause basement floors to crack or lift over time.

A bacterial sludge that can clog foundation drains and sump systems, potentially causing water infiltration.

Common in older homes and associated with health risks, particularly for children.

Older underground or indoor oil tanks can create environmental contamination risks and costly cleanup obligations.

8. Hire a notary, sign the deed of sale, and pay

In Quebec, all residential real estate transactions must be finalized by a notary. A notary is a legal professional and public officer responsible for preparing and authenticating the legal documents required to transfer ownership of the property.

The notary acts as a neutral party between the buyer, seller, and lender, helping ensure that the transaction is legally valid and that all funds and documents are properly handled.

A notary typically performs the following tasks during a real estate transaction:

| Task | What the Notary Does |

|---|---|

| Examine the Property Titles | Reviews the property’s title history in the Quebec Land Register to confirm ownership and identify any liens, unpaid taxes, servitudes, or legal claims attached to the property. |

| Prepare the Deed of Sale | Drafts the official legal document that transfers ownership of the property from the seller to the buyer. |

| Prepare the Deed of Hypothec | Prepares the mortgage security documents required by the lender and registers the lender’s legal interest against the property. |

| Calculate Adjustments | Calculates prorated amounts for municipal taxes, school taxes, condo fees, utilities, and other prepaid expenses so each party pays their fair share. |

| Manage Payments Between Parties | Receives and distributes funds through a trust account, including the down payment, mortgage funds, adjustments, and payment to the seller. |

| Update the Quebec Land Register | Registers the deed of sale and related legal documents with the Quebec Land Register to officially transfer ownership to the buyer. |

Learn more about what a notary does in Quebec

9. Organize your move and pick up the keys

Now that the deed of sale has been signed, it is finally time to move into your new home. This is usually the exciting part: handshakes, hugs, keys in hand, and the beginning of a new chapter.

To help make moving day as smooth and stress-free as possible, here are a few practical tips.

The Property Should Be in the Same Condition

When you arrive at the property, it should generally be in the same condition as when you viewed it and agreed to purchase it. This obligation is normally included in the Promise to Purchase and related legal documents signed during the transaction.

The seller should have removed their belongings unless otherwise agreed, and any included fixtures, appliances, or equipment listed in the agreement should still be present.

If something appears seriously damaged, missing, or different from what was agreed upon, document it immediately and contact your broker or notary as soon as possible.

Move in Stages if Possible

If you have access to the property before the main moving day, consider moving in gradually.

For example:

- Pick up the keys and bring over smaller items first

- Measure rooms and plan furniture placement

- Clean the property before everything arrives

- Test lights, appliances, internet, and utilities

- Move valuables or fragile items separately

This can significantly reduce stress and make the main moving day much more manageable.

Plan Your Lease Exit Carefully

If you are currently renting, try to negotiate your lease termination as early as possible with your landlord.

In Quebec, tenants have certain legal options that may help if they need to leave before the lease expires, including lease assignment or subletting. In many cases, if a landlord refuses a reasonable lease transfer candidate without valid grounds, it may affect their ability to continue enforcing the lease.

However, rental law can be complex, and rules may change depending on the situation. Before making decisions, it is always wise to verify your rights directly with the Tribunal administratif du logement (TAL) or a local housing support organization.

Most landlords prefer to avoid disputes or formal proceedings and are often willing to negotiate a practical solution if approached early and professionally.

Prepare for the Unexpected

Even well-planned moves usually involve a few surprises. Elevators break, trucks arrive late, boxes go missing, and internet installations somehow never happen on time.

A few things that can help:

- Keep important documents with you

- Pack an “essentials” box for the first night

- Confirm utility transfers in advance

- Reserve elevators if moving into a condo building

- Book movers early, especially around July 1st in Montreal

- Take photos of the property when you move in

Most importantly: expect some chaos, stay flexible, and remember that within a few days, it will start to feel like home.