Getting a mortgage with bad credit is definitely possible in Canada. However, if you go about it the wrong way, it can quickly turn into a financial disaster — costing you your savings, trapping you in expensive debt for years, or even making it impossible to buy a house in the foreseeable future.

The good news is that there are ways to buy a home with bad credit while still protecting your long-term financial future.

In this guide, we’ll explain the right way — and the wrong way — to get a mortgage with bad credit in Canada. We’ll cover:

- How do credit scores actually work?

- What credit score is needed for a mortgage?

- How to get a mortgage with bad credit?

- The right way to get a mortgage with bad credit

- Frequently asked questions

Need help with getting mortgage approval?

You don’t have to figure everything out on your own. If you’d rather skip the stress and get clear answers about your options, you can speak directly with a mortgage broker now. A good broker can quickly tell you what solutions may be available based on your situation.

How do credit scores work?

A credit score is a three-digit number between 300 and 900 that lenders use to estimate how likely a borrower is to repay their debt. Generally, the higher your credit score, the lower the risk you present to a lender.

In Canada, your credit score is calculated by one of two major credit bureaus: Equifax Canada and TransUnion Canada. Each bureau uses its own scoring models and algorithms to calculate your score, which means your score can vary slightly depending on where you check it.

Although the exact formulas are not publicly shared, both credit bureaus use information from your credit report, such as payment history, debt usage, credit history length, and recent credit activity.

The table below shows how Canadian lenders commonly view different credit score ranges.

| Classification | Credit Rating | TransUnion Range | Equifax Range |

|---|---|---|---|

| Subprime | Poor | 300 – 692 | 300 – 559 |

| Near-Prime | Fair | 693 – 742 | 560 – 659 |

| Prime | Good | 743 – 789 | 660 – 724 |

| Prime | Very Good | 790 – 832 | 725 – 759 |

| Super-Prime | Excellent | 833+ | 760+ |

What credit score is needed for a mortgage?

In Canada, it is possible to get a mortgage with almost any credit score. However, your credit score can significantly affect the interest rate, borrowing costs, and mortgage options available to you.

Generally, borrowers with stronger credit profiles have access to more lenders, lower interest rates, and more flexible mortgage products. Borrowers with lower scores may still qualify, but often face higher borrowing costs and stricter terms.

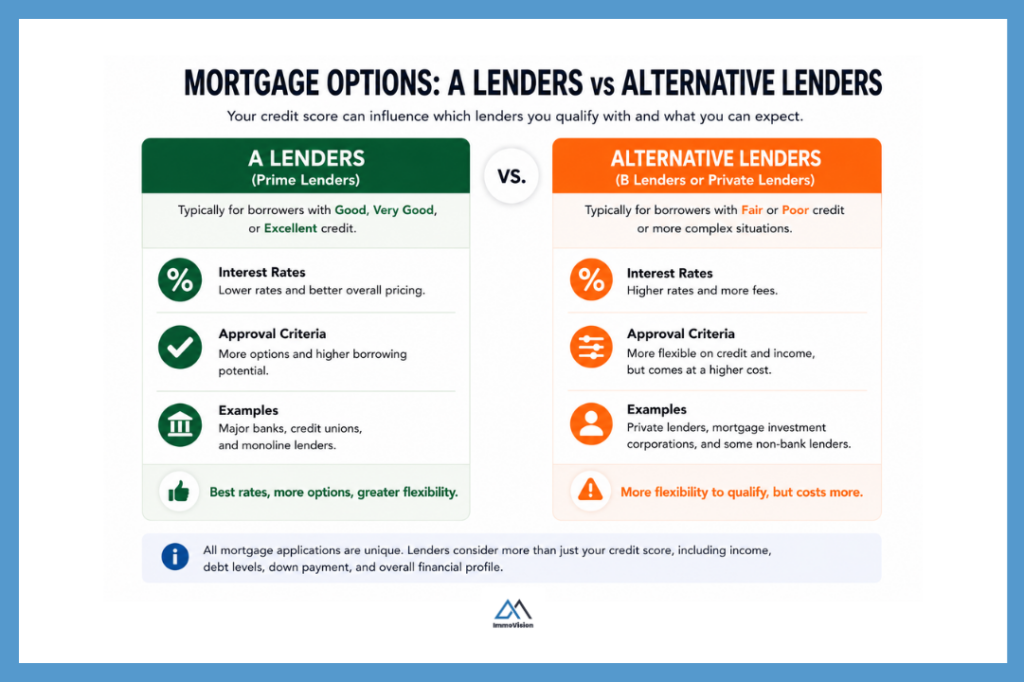

As a general guideline, borrowers with a “Good” credit rating or higher are more likely to qualify with an A Lender. However, the exact credit score required can vary between lenders because each lender may use different credit models and approval criteria.

Borrowers with lower scores often fall into the “Fair” or “Poor” credit categories and may need to work with an Alternative Lender such as a B Lender or Private Lender instead. These lenders are typically more flexible and may approve borrowers with higher debt levels, credit issues, or non-traditional income sources. However, because the lender is taking on more risk, interest rates and fees are often higher.

ℹ️ Note

The important thing to remember is that lenders do not look at your credit score alone. They also consider factors such as your income, debt levels, employment history, down payment size, and overall financial profile. A lower credit score does not automatically prevent you from getting approved.

How to get a mortgage with bad credit?

Broadly speaking there are 4 common ways that home buyers get a mortgage with bad credit.

- Work with an alternative lender

- Repair your credit score

- Increase the size of your downpayment

- Add a co-signer or guarantor

In this section we consider each of these options.

1. Work with an alternative lender

In Canada, you will often hear people refer to A Lenders and Alternative Lenders. A Lenders include banks, credit unions, and other prime lenders. They will typically only lend money to home buyers with good credit. On the other hand, Alternative Lenders which includes, B Lenders, such as subprime Monoline Lenders, and Private Lenders, like MICs, are generally willing to lend money to home buyers with bad credit.

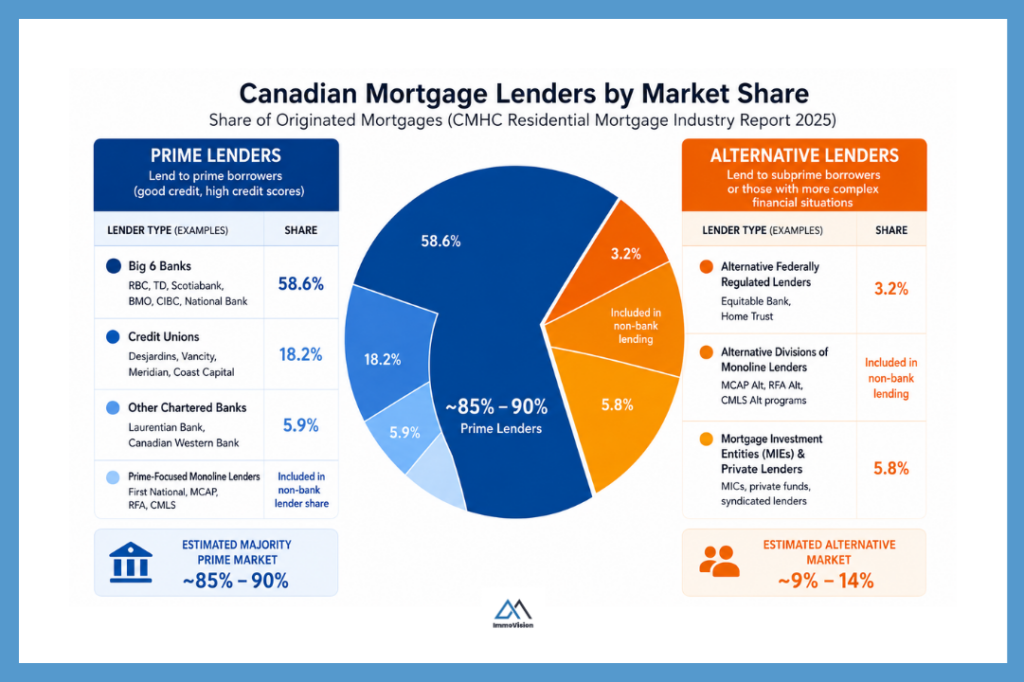

Each year, the CMHC publishes a report showing where Canadians get their mortgages and the market share of different types of lenders. The graphic below shows this data, highlighting the main lender types available in Canada and how popular each option is among borrowers.

ℹ️ Note

In the above graphic, the Monoline Lenders provide mortgages to both prime and subprime borrowers, which is why the percentages may not add up perfectly across categories.

There are some pros and cons to working with Alternative Lenders, the main pro being their willingness to lend money to people who find it difficult to borrow money from traditional lenders e.g. those with non-traditional forms of income, self-employed, new immigrants, and so on.

Counter to this, the main downside is that mortgages from Alternative Lenders tend to be more expensive than loans from the A Lenders. This is because the Alternative Lender charges both a higher rate of interest and fees for mortgage setup. The higher rate of interest is to compensate them for taking on more risk by agreeing to work with people who have been rejected by a bank. While the amount of money they charge extra is not much in the short run, over a 25 – 30 year time horizon, the cost difference can be significant.

2. Repair your credit score

Another way to get a mortgage with bad credit is to improve your credit score. While moving from a poor score to an excellent one can take time, some changes can have a noticeable impact relatively quickly. It often makes sense to tackle these immediate improvements while also working on longer-term issues.

Before making changes, start with a plan. The first step is understanding exactly what is affecting your score so you can focus on fixing the right problems. To do this, review your credit report, which is generally broken into a few key areas that show how you manage debt and credit:

- Payment history: This looks at whether you consistently pay debts on time. Missed payments, overdue accounts, collections, and charge-offs can all negatively affect your score.

- Credit utilization: This measures how much of your available credit you use. For example, if you have a $10,000 credit limit and regularly carry a $9,000 balance, your utilization is 90%. Lenders generally prefer to see this closer to 30% or lower because it suggests you are not heavily dependent on borrowing.

- Credit history length: Lenders prefer to see a longer history of responsible borrowing. If you are new to credit, opening and properly managing a credit account can help build history over time. Likewise, avoid closing older accounts unnecessarily, as this can sometimes reduce your credit age.

- Credit inquiries and account activity: Applying for new credit often triggers a “hard inquiry.” Too many hard inquiries in a short period can lower your score because it may signal financial stress. Soft checks, such as checking your own credit score, do not affect it.

You can review your credit score through free soft-check tools like LoansCanada.ca, which allow you to see your score and the factors affecting it without impacting your credit.

3. Increase the size of your downpayment

Another option is to reduce the amount of risk for the lender. One of the most effective ways to do this is by increasing the size of your down payment.

A larger down payment means you need to borrow less money, reducing the lender’s exposure if market conditions change. It also lowers your loan-to-value ratio, giving the lender more equity in the property as security. For example, if a home costs $500,000 and you put down $25,000, the lender needs to lend you $475,000. If instead you put down $100,000, they only need to lend $400,000. Since you’re borrowing less and already own more of the home, the lender takes on less risk.

Beyond helping you qualify, a larger down payment can also reduce your monthly mortgage payments and, in some cases, improve the mortgage products or interest rates available to you.

ℹ️ Note

There are many different ways to save for your down payment faster for instance, you can use registered accounts such as a First Home Savings Account (FHSA), Home Buyers’ Plan (HBP) through your RRSP, or store money in a Tax-Free Savings Account (TFSA). You can also consider accepting a gifted down payment, however there are certain rules around how you can use this.

4. Add a co-signer or guarantor

One option for getting approved for a mortgage with bad credit is to apply with a co-signer or guarantor.

- A co-signer agrees to share responsibility for the mortgage with you. Because they are equally responsible for the debt, the lender can pursue them for payments if you are unable to make them. In many cases, a co-signer will also have an ownership interest in the property and their name may appear on the title.

- A guarantor serves a similar purpose but does not usually have ownership rights to the property. They agree to step in and cover the mortgage payments only if the borrower cannot meet their obligations.

Each option has advantages and disadvantages, but the most important thing to understand is that this is a significant financial commitment. Since both arrangements involve shared risk, they generally work best when there is a strong existing relationship and a clear understanding of expectations. This is because missed payments or a mortgage default can create financial stress and place strain on personal relationships.

The right way to get a mortgage with bad credit

If an A Lender rejects your mortgage application, there may be a valid reason for it. In many cases, the concern is simply that the mortgage would place too much strain on your monthly budget. You should also consider if this assessment is accurate or, if you can afford a mortgage from an alternative lender.

The key with bad credit mortgages is not just getting approved, but making sure the mortgage remains sustainable over time. If too much of your income goes toward housing, it can become difficult to save for emergencies, home repairs, retirement, investments, or even day-to-day living expenses.

Because mortgage payments are fixed for the term (typically 1–5 years), choosing a payment that is too high can also limit your financial flexibility during that period.

While every situation is different, many financial advisors suggest keeping total housing costs below roughly 30% of your gross monthly income. This is less about what a lender will approve, and more about what is financially comfortable long-term.

Practical guidelines to help decide if a mortgage works for your finances or not

Here are a few practical guidelines that advisors often use when helping people decide whether buying a home makes financial sense:

- The 5 Year Rule: A common benchmark is the “5-year rule”, which suggests that buying tends to make more financial sense if you plan to stay in the home for at least five years. This allows enough time to recover upfront costs of buying a home such as, closing costs, property taxes, and land transfer taxes (the dreaded Quebec “welcome tax”).

- Total Cost of Owning vs Renting: Advisors also often compare the total cost of owning vs. renting, including mortgage payments, interest, taxes, insurance, maintenance, and fees, against the cost of renting and investing the difference. This helps determine whether buying builds long-term value in your specific situation.

- Find The Break-Even Point: Finally, you should find a break-even point. This essentially estimates how long it takes for the financial benefits of ownership (such as equity growth and potential property appreciation) to outweigh the upfront and ongoing costs of buying.

Taken together, these guidelines help ensure that buying a home is not just possible, but financially sensible over the long term.

Frequently asked questions

Most major banks in Canada prefer to see a credit score of at least 680 for the best chance of approval and competitive mortgage rates.

Your credit score is only one part of the mortgage approval process. Lenders will also look at your income, debt levels, employment history, and down payment amount.

– Homes up to $500,000 → Minimum down payment of 5%

– Homes between $500,000 and $1.5 million

→ 5% on the first $500,000

→ 10% on the portion above $500,000

– Homes priced at $1.5 million or more → Minimum down payment of 20%

If your down payment is less than 20%, you’ll usually need mortgage default insurance through providers like Canada Mortgage and Housing Corporation (CMHC). This insurance protects the lender and increases your mortgage costs. For more information on this read, How much is a down payment for a house in Canada.

In addition to the down payment, buyers should also budget for closing costs, which are typically around 1.5% to 4% of the purchase price. To do get an accurate view on your closing costs, you can use the Immovision Closing Cost Calculator.

– Major banks typically have the strictest approval requirements, but offer the lowest rates.

– Credit unions can sometimes be more flexible than banks, especially for self-employed borrowers or people with non-traditional income.

– Mortgage brokers can help you compare multiple lenders and may find lenders that are more willing to approve difficult applications.

– B Lenders are often easier to qualify with if you have bad credit, high debt, or past missed payments, although rates and fees are usually higher.

– Private Lenders are normally the easiest to qualify with, but they are also the most expensive option and are often used as a short-term solution.

If you have strong credit and stable income, a major bank may still be the easiest and cheapest option. However, if you have credit challenges, inconsistent income, or a recent consumer proposal or bankruptcy, working with a mortgage broker that specializes in alternative lending may give you the best chance of approval.