In Quebec, the purchase price for your home isn’t the final price.

In fact, several weeks after the transaction closes, you will receive an invoice at your new address from your municipality for the “welcome tax”.

This tax can add add thousands of dollars to the cost of buying a property in Quebec. It is especially hard to budget for because the amount that you have to pay varies based on the property’s value, location, and the municipality where it is located

In this guide, we’ll explain how the welcome tax works, how to estimate what you’ll owe, and whether you qualify for any exemptions or rebates that could reduce your bill.

- What is welcome tax?

- Why do Quebecers call it welcome tax?

- How to calculate the welcome tax

- When do you have to pay your welcome tax?

- Legal ways to avoid or reduce the Welcome Tax in Quebec

- Frequently asked questions

- Final remarks

Avoid Overpaying For Your Home

Research shows that the right real estate agent can reduce your closing costs by up to 60%. Use Immovision AI to identify top performing, local realtors so that you can avoid overpaying for your home.

What is the “Welcome Tax”?

In Quebec, the “welcome tax” is the nickname that Quebecers use for the Land Transfer Tax. Despite its friendly name, it is a municipal tax that must be paid whenever you purchase a property in Quebec.

The way it works is that when a property changes ownership, the municipality charges the tax and uses the revenue to help fund local infrastructure and public services, such as road maintenance, public transit, parks, libraries, and emergency services.

The welcome tax is a one-time payment that you must pay when you buy a property. However, it applies to every property purchase you make, not just your first home. Whether you are a first time buyer, upgrading to a larger home, or purchasing an investment property, you pay the welcome tax each time ownership of a property changes hands.

Why do Quebecers call it Welcome Tax?

Quebecers call the land transfer tax the “welcome tax” ironically. It is a nod to Minister Jean Bienvenue, who campaigned for the introduction of the land transfer tax in the 1970s. Jean’s surname “Bienvenue” literally means “welcome” in French. Because of this, the local French speaking Quebecers started calling it the “taxe de bienvenue” which translates to “welcome tax” and the nickname stuck.

How to calculate the Welcome Tax?

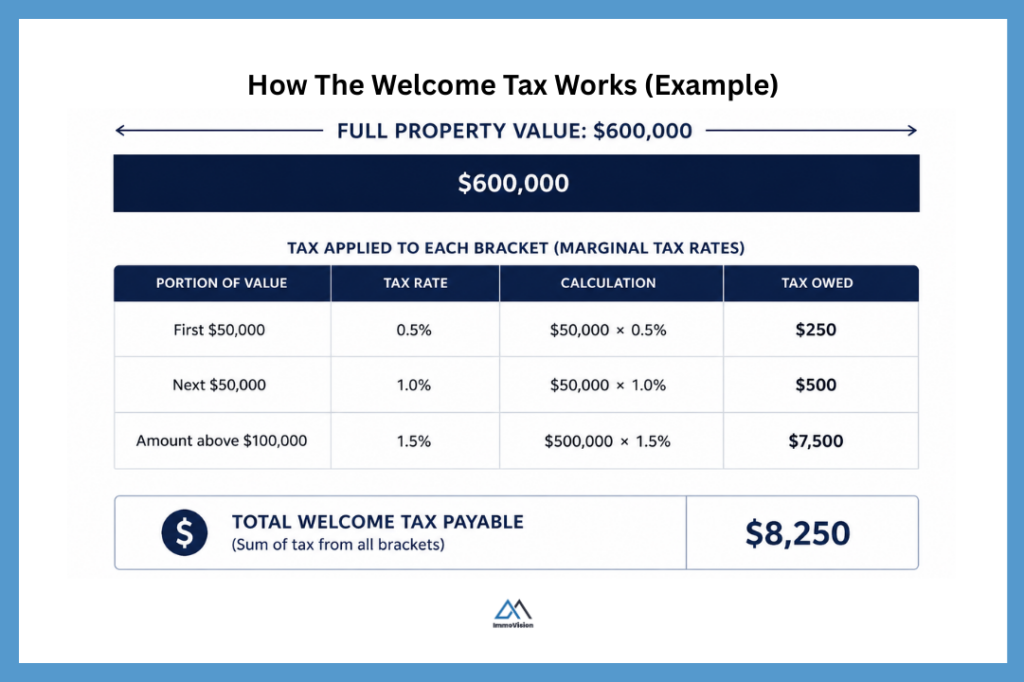

In Quebec, the welcome tax is a progressive tax, meaning that the more valuable the property, the higher the marginal tax rate that applies to portions of its value.

For example, imagine that you purchase a property worth $600,000. Your municipality does not tax the entire $600,000 at a single rate. Instead, they divide the property’s value into tax brackets. From there, they will tax the first portion at a rate of say 0.5%, the next portion at 1.0%, and the amount above that at progressively higher rates. We refer to this approach as a marginal tax system because each rate applies only to the portion of the property’s value that falls within its specific bracket.

ℹ️ Note

When calculating the welcome tax, the municipality will use the higher of the property’s purchase price or its municipal assessed value to determine the taxable amount.

To avoid overpaying for a home, it helps to understand its true market value before you make an offer. You can do that using the Immovision Home Value Estimator.

Municipal rates vs base rates

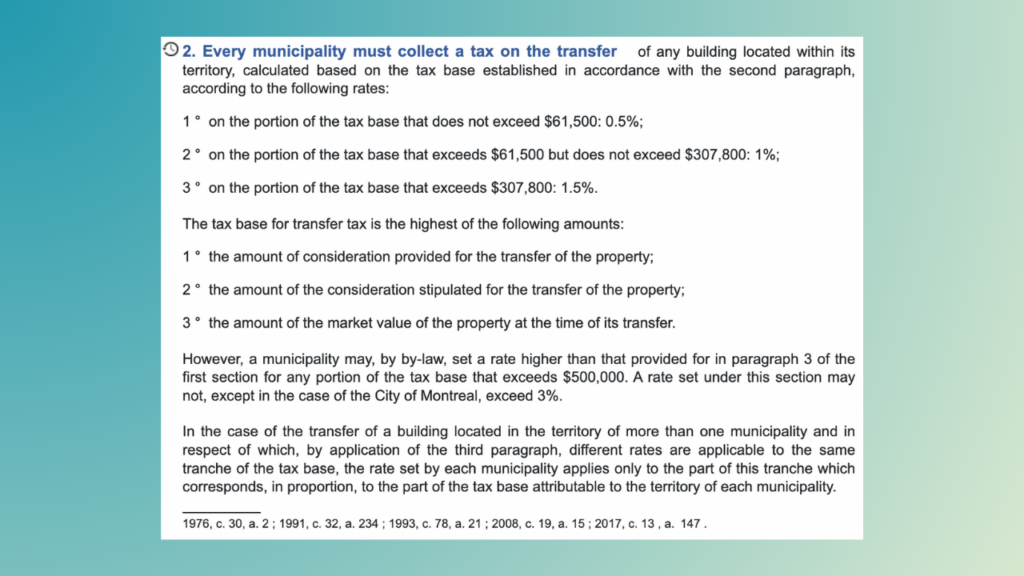

The Law Concerning Duties on Transfers of Immovables establishes the framework for land transfer taxes in Quebec. Under Article 2 of the Act, municipalities must charge the minimum provincial tax rates on property transfers. You can think of this like a minimum base rate that all municipalities must charge. However, municipalities have the authority to increase the rate applied to the portion of a property’s value that exceeds $500,000, up to a maximum rate of 3%. The City of Montreal is the only exception and is permitted to charge rates that exceed 3% on high-value properties.

Because of this rule, the welcome tax payable on a property can vary depending on where the property is located. And, if a property spans more than one municipality, each municipality applies its tax rate proportionally to the portion of the property located within its territory.

As you can see in the image above, the base tax rates are:

| Portion of Tax Base | Rate |

|---|---|

| Up to $61,500 | 0.5% |

| $61,500.01 – $307,800 | 1% |

| Over $307,800 | 1.5% |

Each municipality publishes their own welcome tax on their municipality websites, links below.

Free Welcome Tax Calculator

When do you have to pay your welcome tax?

Officially, municipalities say that you have 30 days to pay your welcome tax from the billing date, and you should receive the bill within 30 to 60 days of your purchase. However, many realtors will tell you that in practice it can take several months—and sometimes over a year—before you receive your bill.

If you have purchased a new construction, it can take even longer because the municipality may need to update its property assessment records, register the completed building, or process the final transfer information before issuing the tax bill.

If you haven’t received your bill within 6 months of your home purchase, it is generally a good idea to contact your municipality directly. This is because, in some cases, the notice may have been sent to the wrong address, delayed in processing, or simply lost in the mail. However, if this happens to you, your municipality may still charge late fees if a bill goes unpaid after its due date.

ℹ️ How to get in touch with your municipality?

To get in touch with your municipality just Google for their contact information or use the contact details below.

- City of Montreal: Call 311 or 514-872-0311 (from outside Montreal)

- Laval: Call 311 or 450-978-8000 (from outside of Laval)

- Ville de Longueuil: Call 311 or 450 463-7311 (from outside Longueuil)

- Brossard: Call 450 923-6311

- Quebec City: Call 311 or 418 641‑6311 (from outside Quebec City)

- Gatineau: Call 311 or 819-595-2002 (from outside Gatineau).

Legal ways to avoid or reduce the Welcome Tax in Quebec

Quebec’s welcome tax is governed primarily by the Act respecting duties on transfers of immovables. Chapter III of the Act contains several statutory exemptions, while additional relief may be available through provincial tax measures and municipal rebate programs.

Based on our review of these rules, we found five scenarios where the buyer may be able to avoid or reduce their welcome tax. These are:

- Transfer between spouses or common-law partners

- Direct family transfers (parent ↔ child, grandparent ↔ grandchild)

- Transfers due to death (inheritance)

- Transfers between an individual and their corporation

- Municipal home-buyer programs

Transfer between spouses or common-law partners

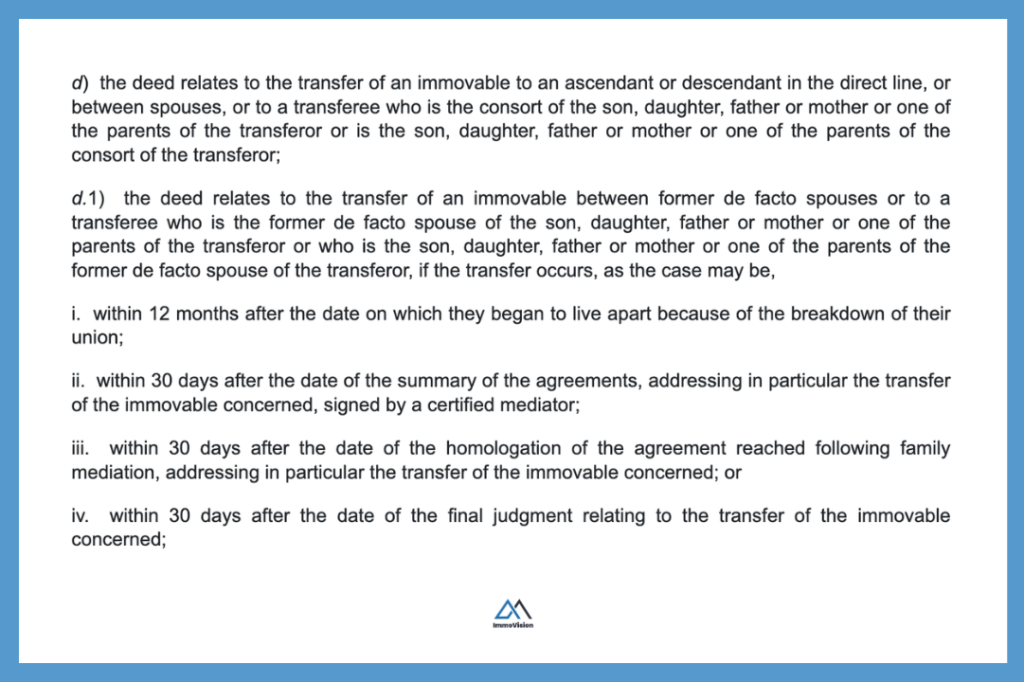

In Québec, transfers of an immovable between spouses (married or in a civil union) are generally exempt from land transfer duties. This exemption also extends to certain transfers between family members connected through the spouses, such as sons-in-law and daughters-in-law, fathers-in-law and mothers-in-law.

Common-law, de facto spouses are also covered by this exemption provided that they transfer the deed of sale from one to the other within 12 months of the date of their separation.

These rules are set out in Clauses 20d) and d.1) that are shown in the image below. This rule state that there shall be an exemption from the payment of transfer duties when:

Direct family transfers

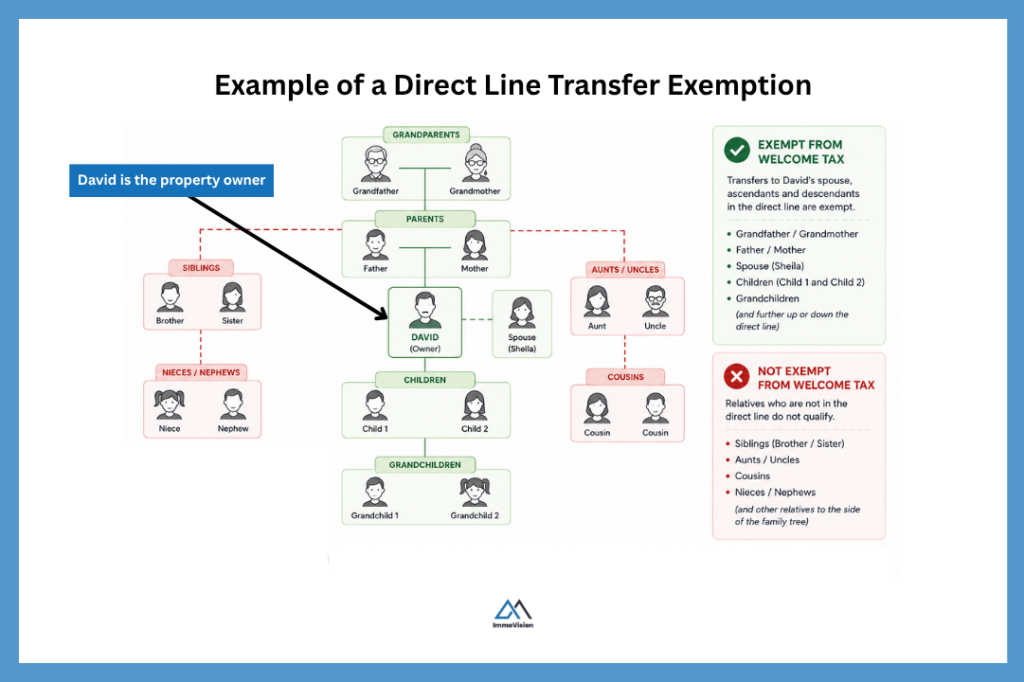

Under Section 20(d) of Québec’s Act respecting duties on transfers of immovables, certain transfers between close family members are exempt from Welcome Tax.

The law refers to these relatives as “ascendants” and “descendants in the direct line.” In plain English, this means family members who are directly related through parents and children.

For example, a transfer between a parent and child, grandparent and grandchild, or great-grandparent and great-grandchild is generally exempt from land transfer duties. The exemption works in both directions, meaning the property can be transferred from the older generation to the younger generation or vice versa.

The key requirement is that the individuals must be directly related by line of descent. Relationships such as siblings, cousins, aunts, uncles, nieces, and nephews are not considered part of the direct line and do not qualify for this exemption.

Transfers due to death (inheritance)

When someone dies in Québec, a notary (or liquidator) prepares a Declaration of Transmission by Death. The notary uses this document to formally register the transfer of property from the deceased to their heirs in the land register.

In most cases, the municipality does not charge Welcome Tax on the inheritance. This is because the transfer occurs by operation of law and is not considered a sale. For example, when a parent leaves their home to their child, this transfer is generally exempt from land transfer duties. The property is simply transferred as part of the estate administration process, and ownership is updated through registration.

If the heir later sells the property to a new buyer, Welcome Tax would then apply to that new transaction. In this case, the new owner would pay the tax when they buy the home. In all cases, ownership is only officially updated once the Declaration of Transmission is registered in the Quebec land register.

ℹ️ Note

Complex situations involving corporate structures or indirect transfers may involve additional tax considerations, but inheritance itself is generally exempt from transfer duties.

Transfers between an individual and their corporation

If you own a corporation and you transfer your property to that corporation, the municipality generally treats this as a taxable transfer between two separate legal entities. This is because, even if you own 100% of the company, the law considers you and your corporation to be distinct legal persons.

Under certain conditions, however, this type of transfer may be exempt from land transfer duties. For instance, Section 19 of the Act respecting duties on transfers of immovables provides an exemption where the transferor owns at least 90% of the voting rights of the corporation immediately after the transfer.

If you meet this condition, you may qualify for an exemption under the Act.

If this is not the case, then the transfer will generally be subject to land transfer duties calculated on the fair market value of the property, even if no money actually changes hands. We recommend speaking with a tax professional or notary before completing this type of transaction.

Municipal home-buyer programs

Some municipalities offer programs that partially or fully reimburse welcome tax.

Examples may include:

- First-time buyer incentives

- Programs for families with children

- New-construction purchase incentives

The rules vary by municipality and should be verified locally. In Montreal, the program you can apply to is called the Home Purchase Assistance Program.

Avoid Overpaying For Your Home

Research shows that the right real estate agent can reduce your closing costs by up to 60%. Use Immovision AI to identify top performing, local realtors so that you can avoid overpaying for your home.

Frequently asked questions

In addition to welcome tax, the government of Canada also charges a federal Goods and Services Tax (GST) on all new or substantially renovated property sales. The Quebec provincial government also charges their own Quebec Sales Tax (QST) on new or substantially renovated property sales.

Final remarks

Welcome tax is a land transfer duty you must pay when you buy a property in Quebec. It is usually the largest expense in a buyer’s closing costs.

Although paying this tax can feel steep, it funds improvements and services in the area where you buy. In addition, there are tax rebate programs to help offset the cost.

To see the impact of the welcome tax on your closing costs, use the Immovision closing cost calculator. This will help you to accurately budget for the cost of buying a new home.

Work with a local expert

Planning to buy soon? The right local expert will help you calculate your total closing costs and identify rebate programs so that you can avoid overpaying for your home.