Since the 2008 – 2009 financial crash, many people think of subprime as a dirty word. However, subprime mortgages are still very popular amongst Canadians. According to the CMHC Residential Mortgage Industry Report 2025, more than 20% of all mortgages made in 2025 were subprime.

In this article we cover:

- What is a subprime mortgage?

- Who are subprime mortgages for?

- How do subprime mortgages work?

- Comparing subprime and prime mortgages

- Subprime mortgages and the 2008 financial crisis

- Canada’s COVID-19 mortgage payments deferrals program

- Frequently asked questions

- Final remarks

What is a subprime mortgage?

A subprime mortgage is a mortgage that lenders offer to borrowers whom they believe are less likely to repay their loan. These mortgages are usually offered to borrowers with impaired credit profiles. This typically means that the borrower has at least one of the following:

- A low credit score,

- Past missed payments,

- High debt levels,

- Bankruptcy history or

- Non-traditional income sources.

In Canada, your credit profile is maintained by one of two major credit bureaus: Equifax or TransUnion. Before approving you for a mortgage, lenders will review your credit report and credit score through at least one of these bureaus to assess how risky it may be to lend to you.

Who are subprime mortgages for?

In Canada, your credit score is a three digit number between 300 and 900. It is calculated by one of two credit bureaus: Equifax Canada and TransUnion. Each of these companies uses a slightly different method to calculate credit scores. They each categorize credit scores into one of five groups that are used by lenders to determine your credit rating. These are shown in the table below.

| Classification | Credit Rating | TransUnion Range | Equifax Range |

|---|---|---|---|

| Subprime | Poor | 300 – 692 | 300 – 559 |

| Near-Prime | Fair | 693 – 742 | 560 – 659 |

| Prime | Good | 743 – 789 | 660 – 724 |

| Prime | Very Good | 790 – 832 | 725 – 759 |

| Super-Prime | Excellent | 833+ | 760+ |

As you can see, if you have a rating of “Fair” you would be considered “near-prime”. If you have a rating of “poor” lenders consider you a “subprime”.

If you are unsure whether you would qualify for a prime or subprime mortgage, you can check your credit score for free through services such as LoansCanada.ca.

Why is it called a subprime mortgage?

The term “subprime” refers to the creditworthiness of the borrower. By contrast, a “prime” borrower is someone that has a good credit score and an almost spotless credit report.

Whilst some people stigmatize those with a bad credit score, there are lots of reasons why your credit score might be bad. For instance:

- If you don’t have a long credit history in Canada (new immigrants, young people).

- You don’t typically use credit (e.g. you’ve always had the cash to pay upfront).

- You were late or defaulted on old credit card payments.

- And so on.

For more information read How To Get A Mortgage With Bad Credit in Quebec.

How do subprime mortgages work?

Subprime mortgages work in a similar way to prime mortgages in that borrowers receive a loan secured against real-estate and, the borrower agrees to repay the lender according to specific terms. The terms will include (as a minimum) the interest rate, repayment schedule, term length, amortization period, and potential penalties for breaking the mortgage early.

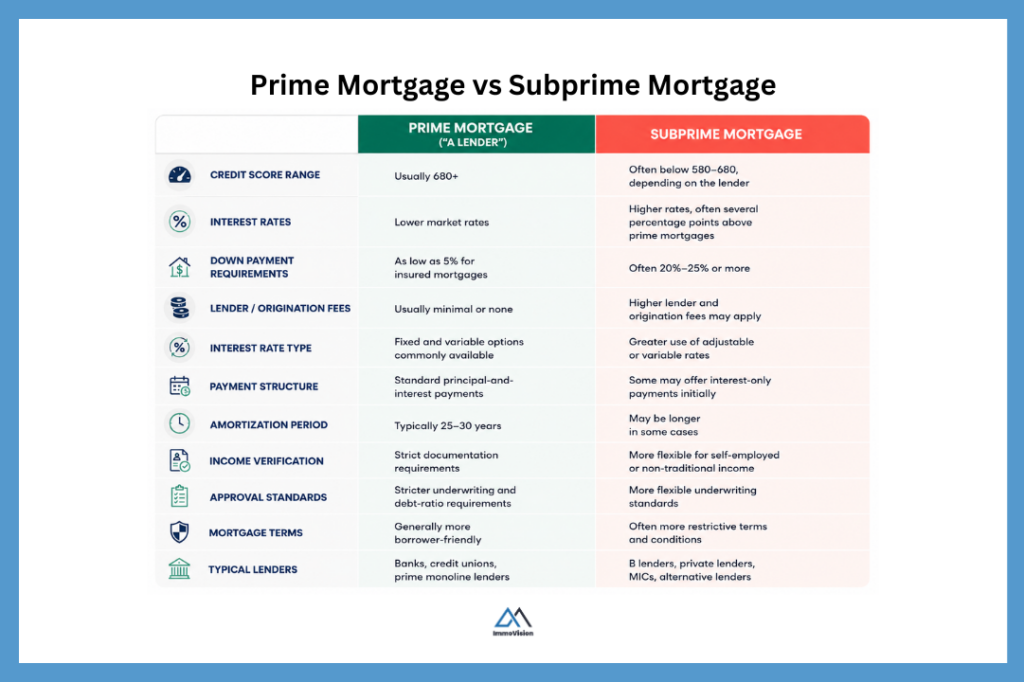

While subprime mortgages differ in their details, compared with traditional “A lender” mortgages they typically have:

- Higher interest rates, often several percentage points above conventional mortgage rates

- Larger down payment requirements, sometimes 20%–25% or more

- Higher lender and origination fees, which can increase closing costs

- More restrictive lending terms and conditions

- Greater use of adjustable or variable interest rates

- Interest-only payment structures during the initial years of the mortgage

- Longer amortization periods in some cases

- More flexible income verification standards for self-employed or non-traditional borrowers

Comparing subprime and prime mortgages

Each prime and subprime lender offers different types of mortgage products. These differ greatly from one and other, and are all used for different purposes. However, the broad differences between prime and subprime mortgages are:

Compare Your Mortgage Options Now

Subprime mortgage rates and qualification criteria are not always publicly advertised, and offers can vary significantly between lenders.

A licensed mortgage broker can quickly assess your credit profile, compare multiple lender options on your behalf, and help you understand what you may qualify for — without affecting your credit score.

In many cases, borrowers discover they have more options than expected, even with imperfect credit or non-traditional income.

Subprime mortgages and the 2008 financial crisis

Subprime mortgages gained a very bad reputation during the 2008 global financial crisis. During this period, many mortgage brokers and lenders issued residential subprime mortgages to borrowers with weak credit or limited ability to repay the loans long term.

At the same time, the U.S. Federal Reserve kept interest rates historically low for much of the early 2000s, making borrowing cheaper and helping fuel a rapid rise in housing prices. Many borrowers relied on low introductory “teaser” rates or rising home prices to refinance their mortgages before payments increased.

Eventually, interest rates began to rise and many adjustable-rate subprime mortgages reset to much higher payment amounts. As a result, many subprime borrowers could no longer afford their monthly mortgage payments and began to default on their loans.

At the same time, rising defaults reduced demand in the housing market and pushed home prices lower. Falling home prices made the situation even worse because borrowers could no longer refinance or sell their homes to pay off the mortgage.

When lenders foreclosed on these properties, they were often unable to recover the full value of the loan because the homes were now worth less than the outstanding mortgage balances.

How was Canada impacted?

Canada’s subprime mortgage market was impacted by the 2008 financial crisis, but far less severely than the United States. This was because the Canadian mortgage market was much more tightly regulated.

Canada did enter a recession in 2008, but this was largely because of its close economic relationship with the United States. As more and more American households went into default, the American consumers and the government cut back on spending to the bare essentials. This reduced the demand for Canadian exports such as manufactured goods, automobiles, lumber, and energy products.

The slowdown caused layoffs and reduced business activity across parts of the Canadian economy, even though Canada’s banking system remained far more stable than the U.S. financial system.

Canada’s COVID-19 mortgage payments deferrals program

In 2020, when COVID-19 sent much of the world into lockdown, many businesses were forced to close temporarily. Millions of individuals lost their jobs or experienced major reductions in income. Because of this, homeowners faced a massive cash flow problem: they still had to make mortgage payments, but many suddenly had little or no income coming in.

The Government of Canada feared that widespread mortgage defaults and forced home sales could trigger a financial crisis similar to the one experienced in 2008 in the United States.

To avert this crisis, Canada’s federal government, banking regulators, mortgage insurers, and major lenders worked together to introduce mortgage relief measures. Many banks and mortgage lenders allowed borrowers to defer mortgage payments for up to six months. The federal government also created income support programs such as Canada Emergency Response Benefit (CERB), that paid $2,000 every four weeks to eligible workers who lost income because of COVID-19.

Deferred mortgage payments eventually had to be repaid, as the missed payments and accumulated interest were added back onto the mortgage balance. By contrast, CERB was a direct government income support benefit and generally did not need to be repaid unless a recipient was later found to be ineligible.

Frequently asked questions

A subprime loan is designed for borrowers with lower credit scores or weaker financial histories, such as past late payments or high debt levels. Since these borrowers are considered higher risk, lenders typically charge higher interest rates and fees to offset the chance of default. Subprime loans can help people access credit when they might not otherwise qualify, but they are usually more expensive over time.

– Higher interest rates: Subprime borrowers are considered higher risk, so lenders typically charge higher interest rates than prime lenders. This will impact your monthly mortgage payments.

– Higher fees: Subprime mortgages tend to come with higher fees compared to traditional A lenders. For instance, you may be charged administration fees to get your mortgage initially and for your mortgage renewal.

– Interest only loans: Some subprime mortgages come with an interest only introductory period. This means that for a period of time after you first get your mortgage, you may be paying only the interest and not the principle. This can make your total home purchase significantly more expensive.

– Adjustable or short-term rates: Certain subprime mortgages may start with low introductory payments that later increase significantly. Imagine that your monthly payments are at a rate of 5% and then after 12 months, they jump to 9%. On a $300,000 loan with a 25-year amortization period, this could increase your monthly payments from approximately $1,754 per month to about $2,518 per month.

Ultimately, subprime loans provide access to credit for borrowers who may not qualify with traditional lenders, but this access tends to come at a higher cost. That said, regardless of whether you borrow from a prime lender or a subprime lender, you can still be foreclosed on if you cannot keep up with your mortgage payments. In the end, responsible borrowing comes down to managing risk, understanding the terms of your mortgage, and ensuring that you can comfortably afford the payments both now and in the future.

If you are thinking about taking out a subprime loan, make sure you understand what you compare deals from multiple B lenders and take the time to work out what you are signing up for. The best way to do this is to carefully review the loan terms, calculate how much your payments could increase in the future, and speak with a qualified mortgage professional to get multiple offers on the table before making a decision.

Final remarks

Although subprime mortgages gained a negative reputation following the 2008 financial crisis, they remain widely used across Canada and fundamentally work the same way as traditional mortgages: borrowers receive a loan secured against real estate and agree to repay the lender according to specific terms and conditions.

However, like prime mortgages, subprime mortgage products can vary significantly between lenders. Interest rates, fees, repayment structures, penalties, and qualification requirements may differ considerably, making it essential to fully understand the terms of any mortgage offer before signing an agreement.

To obtain a subprime mortgage, most borrowers work with a licensed mortgage broker. A broker can help you compare offers from different B lenders, including monoline lenders, Mortgage Investment Corporations (MICs), and other regulated alternative lenders. They can also help you understand the costs involved, negotiate more competitive rates and terms, and guide you through the mortgage application process.

Compare Your Mortgage Options Now

Subprime mortgage rates and qualification criteria are not always publicly advertised, and offers can vary significantly between lenders.

A licensed mortgage broker can quickly assess your credit profile, compare multiple lender options on your behalf, and help you understand what you may qualify for — without affecting your credit score.

In many cases, borrowers discover they have more options than expected, even with imperfect credit or non-traditional income.