Use the Immovision Rental Property Calculator to quickly estimate the potential profitability and performance of a rental property, including cash flow, returns, and long-term growth.

Purchase Information

Income

Operating Expenses (Annual)

Sale / Exit Strategy

Rental property investments in Montreal

A rental property investment is a property that an owner buys to rent out to tenants and earn regular income. In this setup, the owner retains legal ownership and responsibility for maintenance, property taxes, and compliance with local housing regulations.

The investment objective is to hold the property for a period of time, rent it out during this period to generate consistent cash flow that will cover any mortgage payments and maintenance, and then sell the property for a profit or long-term appreciation.

How to use the Rental Property Investment Calculator?

Immovision’s Rental Property Calculator helps you estimate the cash flow, returns, and overall profitability of a rental property. This will help you to compare investment opportunities like a professional property investor, so that you can confidently pick the best investments and avoid wasting money on poor opportunities.

To start, we want to figure out the total profit we can expect from our investment property. To do this, we need to consider five key factors:

Purchase costs

The purchase costs include the price you pay for your home plus closing costs, repairs and any mortgage costs.

The purchase price of the property is the amount that you pay for the property. In Canada, you need to a 20% downpayment for most investment properties. This is unless you buy a plex (duplex, triplex, or fourplex) and live in one unit as your primary residence. In this case you may qualify for as little as 5% down. However, if you invest less than 20% of the purchase price as a downpayment, you will need to pay for CMHC mortgage default insurance.

The closing costs are the costs that you incur to close the deal. In Montreal, this will include expenses like notary fees, pre-purchase inspections, land transfer tax, latent defect insurance and so on.

You should also factor in any repair or renovation costs that you need to make the property rentable. In Quebec, landlords have a legal obligation to provide and maintain a habitable rental unit. This is established under the Civil Code of Quebec (Articles 1854–1862). Repairs can be added to the After Repair Value (ARV), which estimates the property’s market value once all renovations are completed and it is fully ready for sale or rent. It represents the price the property could reasonably sell for or be appraised at once it is fully renovated and ready for the market.

Lastly, if you buy the rental property with a mortgage, you need to factor in the cost of your mortgage. This is determined by the amount you borrow, your interest rate and over what timeframe you borrow the money.

Projected rental income

The projected rental property income is the estimated amount of rent you expect to collect from tenants over a given period. To calculate this, you should look at current rents for similar units in your area by comparing listings and recent rentals to estimate realistic rent amounts.

In Quebec, rent increases are regulated by the Tribunal administratif du logement (TAL) and are generally only allowed at lease renewal. Landlords must give at least three months’ written notice of any proposed increase. There is no fixed maximum rent increase, but the TAL publishes annual guidelines based on factors such as inflation (CPI), taxes, assessed value, insurance, and operating costs. For leases renewing between April 2, 2026, and April 1, 2027, the baseline suggested increase is about 3.1%, before additional adjustments.

You must also make an allowance for a vacancy rate. This is the percentage of time your rental property is expected to be unoccupied. This will reduce the total rental income you can collect over a given period. The overall vacancy rate in the Greater Montreal region was about 2.9% in 2025, meaning only a small share of units are unoccupied at any time. However, vacancy rates vary according to specific property type and location. For example, two bedroom units in downtown Montreal and other high-demand areas typically have lower vacancy rates than single-family homes (detached, semi-detached etc.) on the outskirts.

Ongoing expenses

Rental property investment is not a passive income strategy. It requires time, work and ongoing expenses. The property investor takes on the role of the landlord and all of the responsibilities associated with it. The general responsibilities of a landlord in Quebec include:

- Property maintenance

Landlords must ensure the rental property remains in good, habitable condition at all times. This includes things like heating, plumbing, electrical systems, structural integrity, and urgent repairs, as required under Quebec civil law. - Legal compliance and tenant rights

Landlords must comply with Quebec rental laws and the rules of the TAL. This includes things like lease terms, rent increase procedures, notices, repossession rules, and respect for tenants’ rights to peaceful enjoyment of the property. - Operational and financial obligations

Landlords are responsible for managing the property on an ongoing basis, including paying property taxes and insurance, covering maintenance costs, responding to tenant requests, and absorbing vacancies or unexpected expenses.

Note

Projected equity gain

Projected equity gain is the estimated increase in the value of the property over time, based on assumptions about market appreciation and mortgage principal repayment. In simple terms, it represents how much additional ownership value you expect to build, either because the property becomes more valuable or because your mortgage balance decreases as tenants help pay it down.

Note

Cost of selling

The total cost of selling a property in Quebec includes things like real estate broker commissions, minor repairs and renovations, prepayment penalty and other mortgage fees, certificate of location, pre-listing inspection fee and taxes. The largest cost of selling is usually the real estate broker’s commission. In Montreal, the commission is normally around 4% of the sale price, but it can be negotiated if you shop around, sell during a high-demand market, or use a flat-fee brokerage.

Note

How to calculate your return on investment

When you use the Immovision Rental Property Calculator, it doesn’t just give you one number, it gives you a complete picture of how a rental property investment is expected to performs. Each metric that we generate helps you answer a critical question about the investment opportunity.

| Metric | What It Tells You |

|---|---|

| Total Profit | How much money could you make from the property overall, including eventual sale. |

| Internal Rate of Return (IRR) | How fast you will break even and grow your investment over time. |

| Cash-on-Cash Return | How efficient your rental property is at generating cash relative to the money you invested. |

| Capitalization Rate (Cap Rate) | How efficiently your rental property generates income relative to its purchase price. |

| Year-by-Year Breakdown | How income, expenses, and profits might change throughout the life of the investment. |

Let’s dig deeper so we can understand each of these metrics clearly.

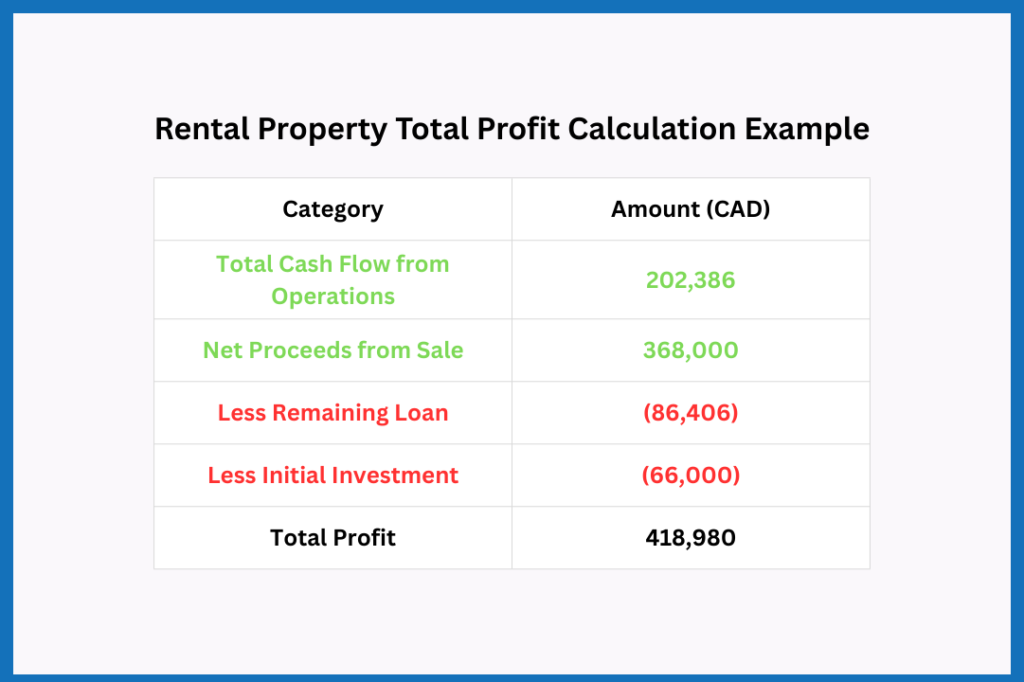

Total Profit (Answers: How much money could you make?)

Total profit is the net amount of money you expect to make from a rental property after accounting for all income, expenses, and equity gains over the life of the investment. Total Profit tells you how much money is on the table, but the other metrics tell you how good the investment actually is.

It is calculated as Total Cash Flow from Operations plus Net Proceeds from Sale minus the Remaining Loan Amount minus the initial investment. You can expand each of the headings in the Rental Property Calculator to see more details on the calculation.

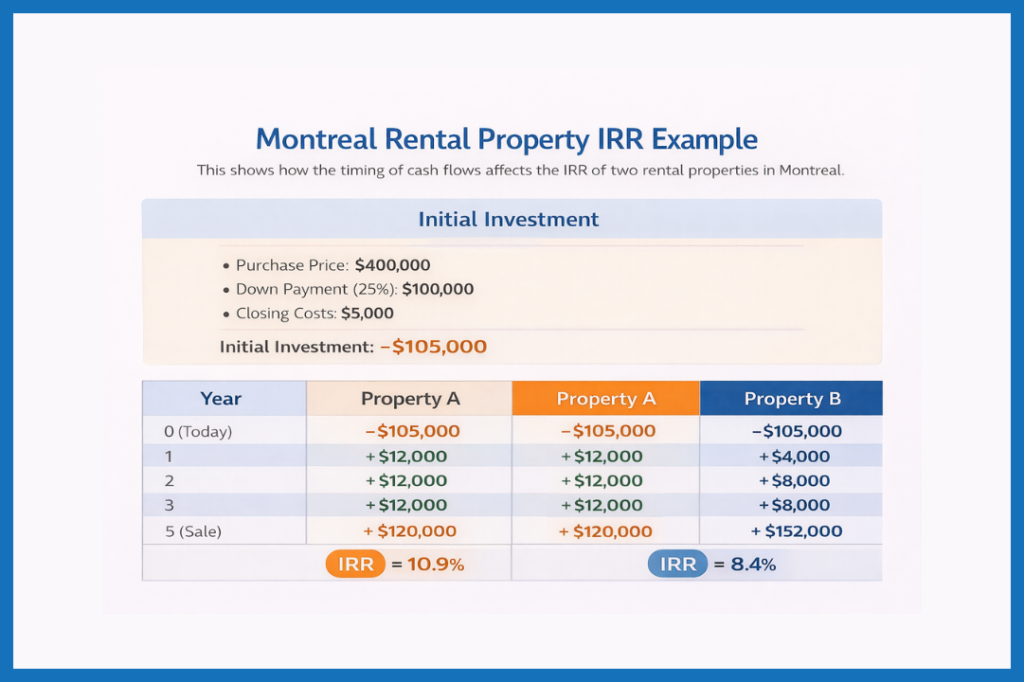

Internal Rate of Return (IRR) (Answers: How fast will you break-even?)

The Internal Rate of Return, or IRR, is the discount rate that makes the Net Present Value of your investment equal to zero. This is an important metric because it tells you how fast you expect to get your money back (break-even) on your rental property investment.

For example, let’s say that you have two investment opportunities in Montreal (Property A and Property B). Both properties have the same purchase price, downpayment and closing costs, but the timing of cash flows are different.

As you can see in the image above, the cash flows for Property A are consistently higher than Property B however, the final sale price for Property B is higher. This means that while you get the sale total cash profit from both investments, Property A returns more of your money faster than Property B. And, as such Property A has a higher IRR because gets you to a NPV of zero faster.

This is why property investors use IRR — it lets them compare opportunities and understand which investment recovers their money faster.

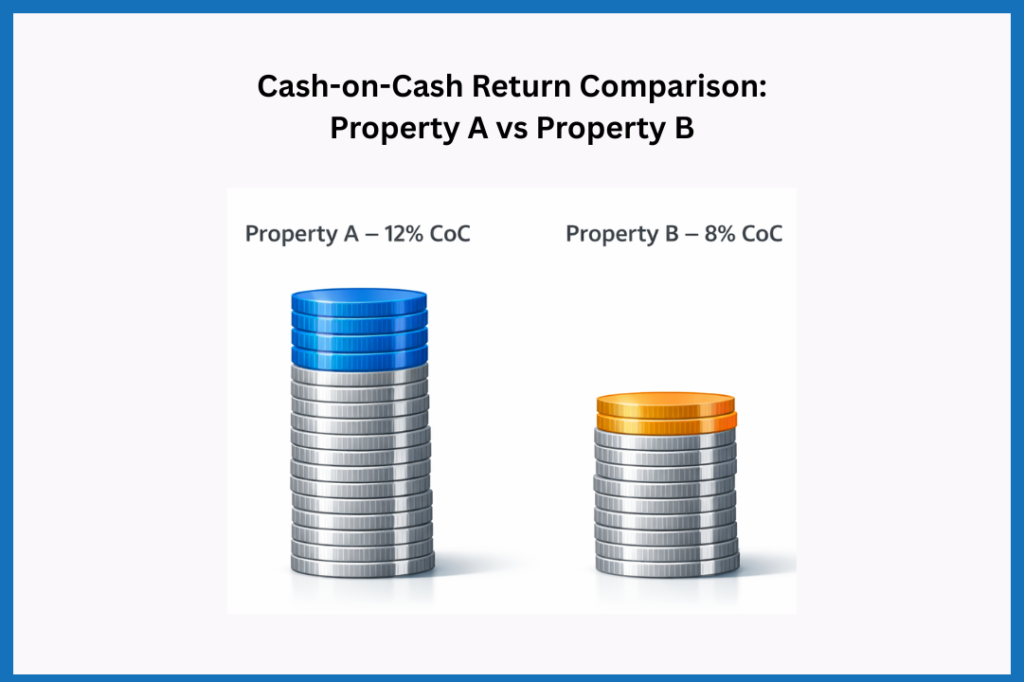

Cash on cash return (Answers: How efficient is your rental property at generating cash?)

Cash-on-cash return tells you what percentage of your invested cash comes back to you each year as actual cash from the property. For example, imagine that you have two rental property investment opportunities: Property A and Property B. Both properties will require the same $100,000 investment however, you estimate that Property A can generate you $12,000 per year vs Property B that can generate you $8,000 per year. In this case Property A will have a higher cash-on-cash return.

Note

In other words, it focuses on how much real money comes into your pocket each year per dollar you put in, ignoring any future profit from selling the property.

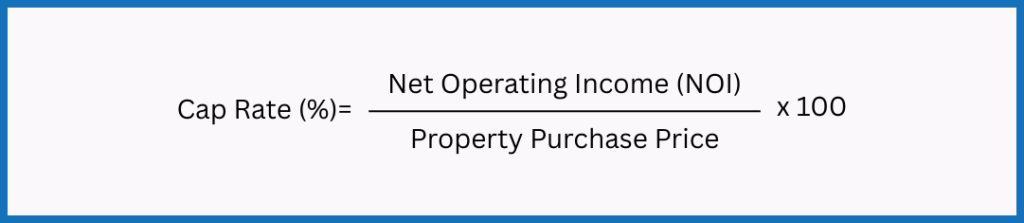

Capitalization rate (Answers: How efficiently your rental property generates income relative to price?)

Capitalization rate, or cap rate, is the cash that you collect in rent, minus operating expenses divided by the purchase price of the property. This tells property investors how efficiently a property generates income relative to its purchase price.

For example, imagine two properties: one costs $1 million and generates $10,000 per year in net rental income, while another costs $500,000 and generates $5,000 per year. At first glance, the first property produces more cash, but when we calculate the capitalization rate, we see both properties return the same relative income:

- Property A Cap Rate = $10,000 ÷ $1,000,000 = 1%

- Property B Cap Rate = $5,000 ÷ $500,000 = 1%.

In this example, even though Property 1 generates more cash in absolute dollars ($10k vs $5k), both properties are equally efficient at generating income relative to their price. As such, the cap rate shows the percentage return on the property’s value, not the total cash flow. So if you were comparing purely on cap rate, neither of these opportunities is “better”, they are just equally efficient. Other factors like financing, potential appreciation, or cash-on-cash return would then help you decide.

Note

Year by year Breakdown

The Year-by-Year Breakdown in the rental property calculator shows how income, expenses, and profits change over the life of the investment. This helps you see when the property will start generating positive cash flow, how rent increases, the impact of vacancies, and how operating expenses affect your returns. It also clearly highlights when you might recover your initial investment. By breaking the numbers down annually, you can plan better, anticipate risks, and make more informed decisions about your rental property.

Frequently asked questions

In addition to the down payment, you’ll need to consider closing costs, which include notary fees, legal fees, land transfer taxes, and sometimes lender-related fees. Don’t forget property management fees if you plan to hire a manager to handle tenants and maintenance.

It’s also important to factor in the ongoing costs of holding the property, including mortgage payments, insurance, property taxes, utilities, and repairs. Some lenders may require mortgage insurance if your down payment is low.

Because these costs can add up, it’s better to be conservative in your estimates. Tools like a cash flow and growth forecast calculator can help you model different scenarios and see how much capital you’ll need upfront and how much cash flow you can realistically expect. Planning ahead ensures that your rental property remains a sustainable and profitable investment.

Final remarks

The Immovision Rental Property Calculator gives you a quick and easy way to calculate the expected cash flow, returns, and overall profitability of a rental property investment.

This information is critical since, with so many investment opportunities, it’s not enough to focus on price or rent alone. Instead, to compare investments effectively, you must understand key metrics such as Internal Rate of Return (IRR), Cash-on-Cash Return, Capitalization Rate, Total Profit, and Year-by-Year Cash Flow. Only with all of this information can you understand both short-term income and long-term growth potential.