It is 100% possible to get a mortgage with bad credit in Quebec.

In fact, according to data from the Canada Mortgage and Housing Corporation, roughly 1 in 10 new mortgages in Canada go to borrowers with poor credit scores.

At the start of 2016, I personally got a mortgage with bad credit. At the time, I had a poor credit score of 630 and, even with this, I was still able to get a mortgage, and buy my first house on Montreal’s West Island for my family.

The lender gave me a 25-year mortgage at 4.14%, and my monthly payment ended up being hundreds of dollars less than what I had been paying in rent for a smaller, mould-infested apartment in Pointe-Saint-Charles.

In this guide, I’ll walk you through what I learnt through hundreds of hours of research, phone calls with mortgage brokers, lenders, and real-estate investors, so that you can know exactly how the mortgage system works in Quebec. This will allow you to understand how to use the system to your advantage, and get a mortgage even with bad credit.

Because once you understand how lenders actually think, you’ll know where to go, what options are available to you, and how to position yourself to get approved and even negotiate better terms.

But first off, let’s begin with the basics… what actually is a bad credit score?

What is considered a poor credit for a mortgage?

In Canada, a credit score is a three digit number between 300 and 900. It is calculated by one of two credit bureaus: Equifax Canada and TransUnion. Each of these companies uses a slightly different method to calculate credit scores. They also each organizes categorized credit scores into one of five groups that are used by lenders to determine your credit rating. These are shown in the table below.

| Credit Rating | TransUnion Range | Equifax Range |

|---|---|---|

| Poor | 300 – 692 | 300 – 559 |

| Fair | 693 – 742 | 560 – 659 |

| Good | 743 – 789 | 660 – 724 |

| Very Good | 790 – 832 | 725 – 759 |

| Excellent | 833+ | 760+ |

As you can see, anything above 743 at TransUnion and 660 at Equifax Canada is considered “Good”. Whereas credit scores below 692 at TransUnion and 559 at Equifax Canada are is considered “Poor”.

Generally speaking if you have a credit score that falls into the Good to Execllent categories, this is classified as good credit and you will not struggle to borrow money. However, if your score falls into the fair or poor category, you may still be able to borrow money, but it will be down to the lender, and their own internal policies.

Note: Credit scores fluctuate on a daily basis, based on a whole range of factors that we will discuss in this article. So before you write yourself as having bad credit, you should check what your score is today.

Get A Free Credit Report

Before you can even start looking at ways to improve bad credit, you need to know why your credit is bad… these answers are in your credit report.

Can You Get a Mortgage With Bad Credit in Quebec?

Yes, you can get a mortgage with bad credit in Quebec. However, it is important to understand how the system works, including the different types of lenders and what they look for.

Who Will Give You a Mortgage With Bad Credit?

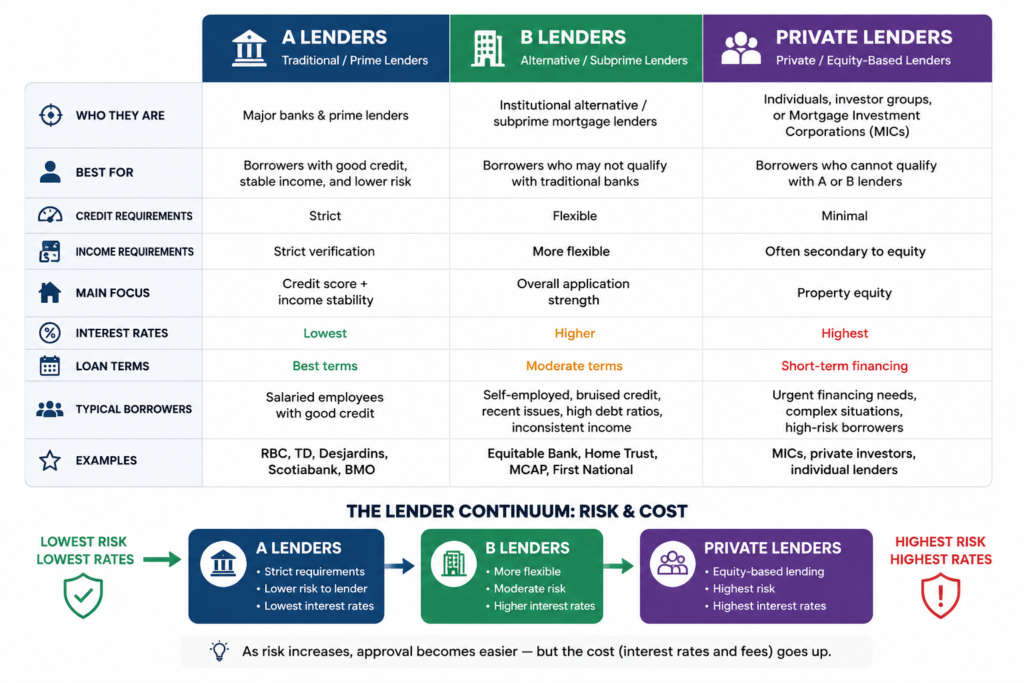

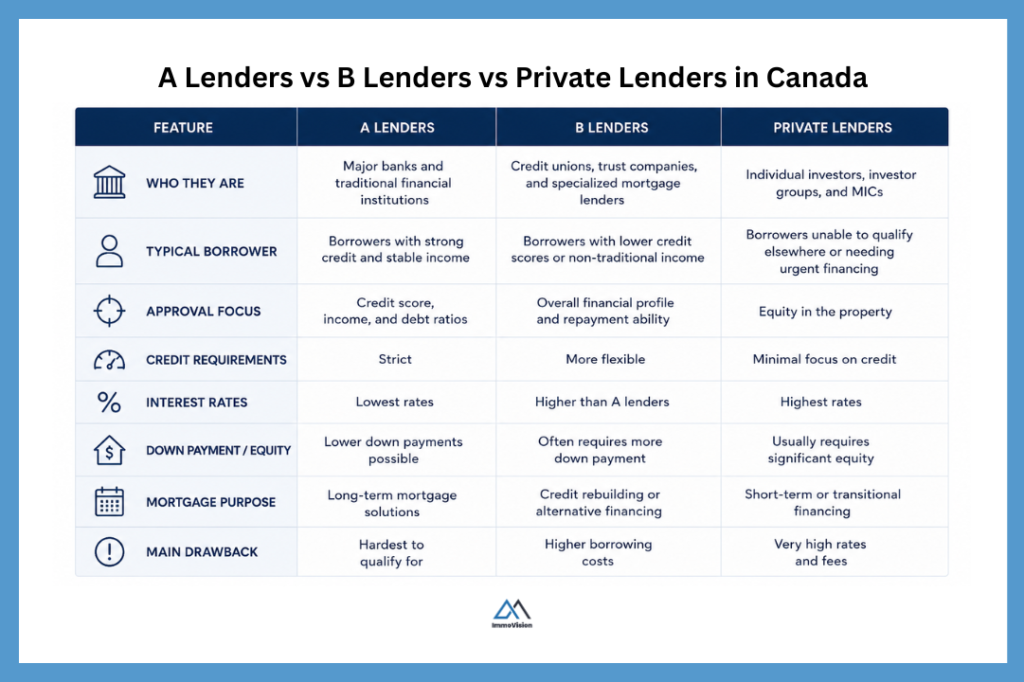

In Canada, there are three main categories of mortgage lenders:

- A Lenders are traditional financial institutions, such as major banks and prime lenders. These lenders work with borrowers who have good credit, stable income, and are lower risk. Examples include Royal Bank of Canada and Desjardins Group.

- B Lenders, also known as alternative lenders or subprime lenders, are institutional mortgage lenders that work with borrowers who may not qualify with traditional banks. This can include borrowers with bad credit.

- Private lenders are individuals, investor groups, or Mortgage Investment Corporations (MICs) that lend money primarily based on the equity in the property rather than the borrower’s credit score or income.

Each type of lender uses its own method of assessing risk and qualifying borrowers. They will also offer different interest rates, length of mortgage, and charge different fees. Understanding these differences is important because the easiest mortgage to qualify for is not always the best financial decision.

The table below gives you a high-level comparison of A lenders, B lenders, and private lenders, who they typically lend to and what are their mortgage approval requirements.

Free Consultation With a Specialist

Navigate the system with a professional mortgage broker who understands both traditional and alternative lenders. They can help you compare options and find the best solution based on your situation.

Five proven ways to get a mortgage with bad credit

Here are five ways that you can do to get a mortgage with bad credit:

- Add a co-signer or guarantor

- Reduce the lenders risk

- Work with B lenders and private lenders

- Work with a mortgage broker (not a bank)

- Improve your credit score

1. Add a co-signer or guarantor

One way to get approved for a mortgage with bad credit is to use a co-signer or guarantor.

- A co-signer is someone who agrees to take legal responsibility for the mortgage alongside you. This means that if you fail to make the payments, the lender can also require the co-signer to repay the debt. The co-signer is also a part legal owner of the property which means that their name will appear on the property title.

- A guarantor is similar to a co-signer in that they agree to repay the mortgage if you fail to make the payments, however they do not legally own the property.

There are various pros and cons to co-signers vs guarantors however, the main thing to consider is that this is a big commitment from the co-signer or guarantor. Both the co-signer and the primary borrower must have a good pre-existing relationship since, if the primary borrower missed a payment, or defaults relationships can become very strained.

Tip

Do not ask someone to become a co-signer or guarantor unless you are confident that you can make every payment on time. If you miss payments, it can damage both your finances and theirs.

| Pros of Using a Co-Signer or Guarantor | |

| Pro | Helps borrowers qualify for a mortgage even with bad credit. |

| Pro | Can help you access better interest rates and mortgage terms. |

| Pro | May allow you to borrow more money by improving your GDS and TDS ratios. |

| Downsides of Using a Co-Signer or Guarantor | |

| Con | A co-signer’s name is usually added to the title of the property. This is generally not the case with a guarantor. |

| Con | The mortgage becomes a liability for the co-signer, which can reduce their borrowing capacity and affect their credit profile. |

| Con | If the primary borrower misses payments or defaults, it can negatively affect the credit score of both the co-signer and guarantor. |

2. Reduce the lenders risk

When you have bad credit, to get approved for a mortgage you must convince the lender that they are unlikely to lose money.

There are several ways to do this, but the most common is to put down a large down payment.

Let’s say you borrow $500,000 to buy a single-family home in Canada and put down $25,000. The lender now has $475,000 at risk. If you default two years later, the bank may need to foreclose on the property and sell it to recover the loan balance. In Quebec, forclosed homes tend to sell at 15% below market value. So in this case, the bank will expect to sell your home for $425,000. This means that they will expect to lose tens of thousands of dollars if you default.

Now compare that to a borrower who puts down $175,000 instead. In that case, the mortgage amount is only $325,000. Even if the property later sells for 15% below market value in a foreclosure, the lender would still recover the full mortgage balance after the sale of the property. In other words, the lender’s downside risk is dramatically lower. In this situation, approving the mortgage becomes a much more reasonable business decision for the bank.

3. Work with B lenders and private lenders

Whilst A lenders will likely not give you a mortgage with bad credit, B lenders and private lenders are able to. This is because these types of lenders have different ways of assessing risk and qualifying borrowers.

There are three main types of B lenders: monoline lenders, trust companies, and specialized mortgage companies. In each case, B lenders generally use more flexible lending criteria than traditional banks. This means they are willing to work with borrowers who may have lower credit scores or higher perceived risk. To compensate for this additional risk, they usually charge higher interest rates than traditional banks, although their rates are often still much lower than credit cards or the rates that you get from private lenders.

Private lenders meanwhile include: individual investors, investor groups, and Mortgage Investment Corporations (MICs). These lenders focus primarily on the equity in the property rather than the borrower’s credit score or income. Private lenders essentially don’t care how reliable you are in terms of debt repayment instead, they look to protect themselves be ensuring that if you do default, they still make money. Because of this, they are generally only prepared to give mortgages for short-term or transitional financing rather than long-term mortgage solutions.

Below is a comparison table showing the pros and cons of A lenders, B lenders, and private lenders.

ℹ️ Note

You generally won’t find B lender and private mortgage options on comparison sites like Ratehub or other online rate tools. Instead, you typically need to work with a mortgage broker, since brokers have access to alternative lenders and specialized lending programs that are not publicly advertised.

4. Work with mortgage broker (not a bank)

A mortgage broker is a licensed professional who helps borrowers compare mortgage options from multiple lenders. Unlike a bank employee, who can only offer products from their institution, a mortgage broker can often connect you with A lenders, B lenders, and private lenders.

This is especially important if you have bad credit, are self-employed, or have recently experienced financial difficulties. In these situations, it is not just about getting approved, you actually need to find the right mortgage strategy for your specific case.

Put another way, an easier-to-qualify-for mortgage is not always the best financial option. For example, some higher-risk mortgages come with higher interest rates, additional fees, and very short terms.

Private mortgages are a good example of this. Many private lenders offer terms of only 6 to 12 months. This means that the mortgage is usually intended as a temporary solution while you improve your financial situation (debt service ratios, credit score, and so on).

Because of this, it is important to have a clear exit strategy before accepting a higher-risk mortgage. A good mortgage broker can help you understand the true cost of the loan and what steps you need to take to eventually refinance into a lower-cost lender.

5. Improve your credit score

The last option is to improve your credit score. This will ultimately give you access to A lenders. However, the time that it will take to rebuild your credit and qualify for better mortgage options will depend on how severe your credit issues are and what is causing them. In some cases, you might be looking at several years. However, there are some things you can do to improve your credit in the short run. We cover all of this and more in the next section: how to improve bad credit.

How to improve bad credit?

If you have bad credit, the first step is not to panic—it’s to understand your situation and build a plan.

Here’s a simple 4-step approach:

1. Get your credit report

Start by pulling your credit report. This will help you to identify what is causing your credit score to be so low. A simple way to get your report for free is through services like Loans Canada.

2. Identify what’s hurting your credit

Review your report carefully to spot any issues. This could include missed payments, high balances, collections, or other negative records.

3. Build a strategy to repair your credit

Once you understand the problem, you can create a plan to address it—whether that means paying down debt, catching up on missed payments, or resolving collections.

4. Find a short-term financing solution (if needed)

If you need financing now, there are still options available. Some lenders are more flexible and can work with lower credit scores while you rebuild.

In the next section, we’ll break down the most common causes of bad credit, how each one affects your score, and a few short strategies to repair your credit in each case.

What causes a bad credit score?

If you want to improve your credit score, the key is to first understand what causes a bad credit score. Bad credit scores can be caused by a several different things. The main ones are:

- Unpaid accounts (e.g. Delinquencies, Charge offs, Defaults)

- Judgments (court orders for unpaid debt)

- High credit utilization ratio

- Consumer proposal or bankruptcy

- Collections

- High volume of inquires

Let’s take a look at each of these and find out how to address and fix them properly.

1. Unpaid Accounts

One of the main ways lenders assess your creditworthiness is by looking at how you’ve handled credit in the past. Your credit report lists all your accounts and shows whether you have ever missed a payment (i.e. been delinquent) or defaulted on a debt. You should review each account carefully to understand what it says about your payment history.

In Canada, unpaid accounts use an “R” rating system, which means that accounts are graded based on the severity of missed payments. The system works as follows:

- R1 – Paid on time (or within 30 days)

- R2 – 31–59 days late

- R3 – 60–89 days late

- R4 – 90–119 days late

- R5 – 120+ days late

- R7 – Making regular payments through a special arrangement (e.g. consumer proposal)

- R8 – Repossession

- R9 – Sent to collections, written off, or bankruptcy (worst rating)

If you pay down overdue balances on any accounts that are in the R2 – R5 range this will improve your credit score. However, if you have an account that is R7 – R9, you can only bring this back to an R5. For instance, if you have an account with an R9 status, if you pay this off in full, it will be restored to an R5 status. However, oftentimes, paying off an R9 in full is not the best strategy since, if the account is already with a collection agency, you can negotiate a settlement for less than the full amount owed.

✨ Credit Repair Tip

If you owe money on multiple fronts:

- Start by listing all outstanding balances from lowest to highest

- Pay off the small debts first (the $50–$100 amounts) and work your way up

- For larger debts, contact the collector and negotiate a reduced settlement in exchange for closing the account as paid or settled, and always get this agreement in writing

- To free up cash, consider selling unused items (e.g. on Facebook Marketplace). Many people have $1,000–$5,000 worth of items they can sell and use toward paying down debt

2. Judgements (court orders for unpaid debt)

A judgment is when a court officially decides that you owe a debt and orders you to repay it. This usually happens when you fail to repay a debt and the creditor takes legal action to recover the money owed.

Judgments can significantly impact your credit because they may appear in more than one place on your credit report. The underlying debt may show up as a defaulted or collection account in your accounts section, and the judgment itself will appear in the public records section.

In practice, judgments typically remain on your credit report for about 6 years with Equifax and 6 to 7 years with TransUnion, depending on the bureau and the province.

| Province | Time on Equifax Report | Time on TransUnion Report |

| Ontario | 6 years | 7 years |

| Quebec | 6 years | 7 years |

| Price Edwards Island | 6 years | 10 years |

| Newfoundland and Labrador | 6 years | 7 years |

If you have a judgement on your credit report, we suggest that you take the following steps to repair your credit.

Step 1. Verify the judgement

You must first verify that the judgment is accurate and that it should still appear on your credit report. This means that the judgment belongs to you, the amount is correct, and that the reporting period has not yet expired.

If the information is either inaccurate or the reporting period has expired, you can dispute it. To do this, you will need to contact the credit bureau with supporting evidence and a clear explanation of why the judgment should be removed.

Step 2. Pay or settle the judgement

If the judgement is accurate, the next step you will need to either pay or settle the judgement. The best way to do this depends on who the judgement is with.

If the judgment is accurate, the next step is to either pay or settle the debt. The best way to approach this will depend on who the judgment is with, as different types of creditors have different levels of flexibility and enforcement options. Most judgments tend to show up in one of the following categories:

- Government debts

- Financial instituions / private lenders

- Businesses or individuals

- Secured creditors / liens

Of these, the hardest to negotiate are government debts. Here the focus is usually on setting up a payment plan and paying in full.

Step 3. Ensure proper updating

Once you have paid off the judgment, the next step depends on the province. In most cases, the creditor must file a formal confirmation that the debt has been satisfied.

In Quebec, this process follows the Civil Code of Québec. Here, even if the debt has been paid, it is not automatically removed from the public record or your credit report. To update the record, the creditor must file a document confirming that the judgment has been paid. This is often called a “quittance” (release) or satisfaction, and it formally records that the debt has been cleared.

In practice, creditors do not always file this document promptly. To deal with this, you should request the quittance directly from the creditor and keep proof of payment. If they do not cooperate, you can use your documentation to follow up with the court or dispute the status with the credit bureaus to have the record updated.

Step 4. Actively rebuild credit

There are lots of things that you can do to improve a bad credit score. Below are three of the top things:

- Get a secured credit card: A secured credit card is a type of credit card that requires you to put down a cash deposit upfront, which acts as your credit limit. For example, if you give the bank $500, they will issue you a credit card with a $500 limit. You can then use it like a normal credit card. To get a secured credit card, contact your bank and ask if they offer secured credit cards and what their application process is, or explore options from other lenders that specialize in credit-building products.

- Keep utilization low: Lenders want to see that you don’t rely heavily on credit, as this can make you appear riskier. To track this, they look at your credit utilization ratio. This tells them how much of your available revolving credit you are currently using. It is best practice to keep your utilization below 30% on your revolving lines of credit (like credit cards).

- Pay everything on time: Set up automatic payments to avoid any further negative marks on your credit history.

ℹ️ Note

Most of the time, if the debt is relatively small, the lender will not pursue legal action. This is because the cost of going to court and enforcing a judgment is often too high relative to the amount owed.

There are also other ways lenders can recover their money without immediately going through the courts. For example, they may send the debt to a collection agency or secure the debt against your property by registering a legal hypothec.

In Quebec, this can include a construction hypothec (for unpaid contractors) or a legal hypothec for unpaid property taxes. These claims are registered against your property and can make it difficult to sell or refinance until the debt is resolved.

3. High Credit Utilization Ratio

Lenders want to see that you manage credit responsibly. One of the main ways they measure this is by looking at your credit utilization ratio. This is a measure of how much of your available credit you are currently using. For example, if your credit card has a $10,000 limit and you currently owe $10,000, then your credit utilization ratio is 100%.

Most people have two types of credit:

- Installment loans – these are your larger loans that are paid back over time in regular payments, such as mortgages, car loans, and student loans.

- Revolving credit – these are smaller amounts of credit that can be repeatedly borrowed and repaid, such as credit cards.

If you take out a large installment loan, your credit score may temporarily dip because your total debt load has increased and a new credit account has been opened. However, if you consistently make your payments on time, your score will often improve over time because you are demonstrating responsible borrowing behavior.

Revolving credit works differently. Lenders generally prefer that you use no more than 30% of your available revolving credit at any given time. For example, if your credit card has a $10,000 limit, you should ideally keep the balance below $3,000 before paying it off. Even if you pay the card in full every month, consistently carrying high balances can still negatively affect your credit score because it signals financial stress and heavy reliance on credit.

If your goal is to improve a bad credit score, one of the fastest things you can do is reduce your credit utilization ratio by paying down your revolving credit balances and keeping them below 30% of your available limit.

4. Consumer Proposal or Bankruptcy

Consumer proposals and bankruptcies show up on your credit report as R7 and R9 ratings respectively. A consumer proposal is a formal agreement where you negotiate with your creditors to repay a portion of your debts over time, whereas a bankruptcy is a legal process where you declare that you are unable to repay your debts and surrender certain assets for liquidation.

Both can have a significant negative impact on your credit score. However, lenders generally view a consumer proposal more favorably than a bankruptcy because it demonstrates that you made an effort to repay at least part of what you owed. A bankruptcy is considered more severe because it usually means the lender recovered little or none of the outstanding debt.

In Canada, a first-time bankruptcy typically remains on your credit report for 6 to 7 years after discharge, depending on the credit bureau and the province. Consumer proposals are generally removed from your credit report either:

- 3 years after you pay off all the debts included in the proposal, or

- 6 years after you sign the proposal (whichever is sooner)

If you decide to pursue a consumer proposal, you must work with a federally licensed insolvency trustee (LIT). These are professionals regulated by the Canadian government who are legally authorized to administer consumer proposals and bankruptcies in Canada.

5. Collections

If you default on a debt, the lender may transfer or sell the account to a third-party collection agency. When this happens, the debt may appear on your credit report as an R9 rating, a collection account, or both. Collection accounts can significantly lower your credit score because they signal that the original lender was unable to recover the debt under the original agreement.

In this situation, you generally have four options:

- repay the debt in full,

- negotiate a reduced settlement amount,

- include the debt in a consumer proposal, or

- wait and see whether the creditor escalates the matter through legal action.

The fastest way to begin rebuilding your credit is usually to repay the debt in full. However, many collection agencies are willing to accept a reduced lump-sum settlement because they would rather recover part of the debt immediately than spend additional time and money trying to collect the full amount later. Also, paying the entire balance may not be financially realistic, which is why negotiated settlements are common.

Before agreeing to any settlement, it is important to get the agreement in writing and confirm exactly how the account will be reported to the credit bureaus after payment.

6. High Volume of Inquires

There are two types of inquiry that you can run on your credit report: a soft inquiry and a hard inquiry. Soft inquires do not impact your credit score however, if you do too many hard inquiries within a short space of time, this can negatively impact your credit score.

This happens because, hard inquiries signal to lenders that you may be actively seeking new credit or taking on additional debt. Lenders interpret this signal as a sign that you may be under financial pressure, or becoming more likely to miss payments in the future, which increases your perceived lending risk.

Although hard inquiries only cause a short term dip, they stay on your credit report for up to three years. Check what your current credit score and inquiry history is, and if you’ve made too many inquiries recently, at Loans Canada.

Common Mistakes to Avoid When Buying a House with Poor Credit

When you are trying to buy a house with poor credit, things are already harder than they should be and this puts you in a vulnerable state. Frustration at the systems can force you to make quick and rash decisions without giving each option proper consideration and this can lean to mistakes that can cost you a lot of money.

In this section we are going to look at, common mistakes to avoid when buying a house with poor credit.

1. Falling for predatory loans

Mistake number one is falling victim to predatory loans. These are mortgage structures designed in a way that makes them extremely difficult to sustain or exit without refinancing under pressure.

For example, imagine a private lender offers you a $500,000 mortgage to buy a home, but requires a $200,000 down payment upfront. The loan is structured with a 12-month term: 4% interest for the first 6 months, then 10% for the next 6 months.

Here’s what that actually means in plain terms.

In the first year, you would pay your $200,000 down payment, plus roughly $26,000 in mortgage payments. The important thing to understand is that on a 25 year term, only about $5,000 of those payments goes toward reducing what you owe (your principal). The remaining $21,000 goes to interest, and gets paid directly to the lender.

At the end of the 12 months, you will then typically be required to either repay the remaining mortgage balance of $295,000 in full or refinance with another lender. Refinancing in this case may be very difficult. On top of this, you also need to factor in closing costs. On a $500,000 purchase, these are typically around 4% of the purchase price, or about $20,000.

All of this means that in the first year your costs will look something like this:

If you don’t pay this, then the lender can take your home, foreclose on you, take your home and resell it.

2. Overstretched budget

The standard financial advice is that you should spend no more than 30% of your monthly income on housing. This allows you still have enough disposable income for other expenses, investment opportunities, and savings.

However, B lenders and private lenders will qualify you for even more than 30% of your monthly income. When you factor in mortgage fees, monthly payment, closing costs, property taxes, home maintenance, buying and owning a house can end up costing you far more than you initially expect. This is why you should talk through the financial implications of a mortgage with either with a licensed mortgage broker or financial advisor before signing anything.

3. Making lots of applications

Oftentimes, borrowers contact several B lenders and private lenders at the same time and authorize each one to access their credit report. This can result in a sudden increase in hard credit checks appearing on the borrower’s credit file, which may lower their credit score.

Although B lenders and private lenders are generally more flexible when it comes to credit requirements, these additional hard checks are often unnecessary. In most cases, you should only authorize a credit check once you have chosen the company or individual you intend to borrow from.

4. Skipping pre-approval

Pre-approval is when the lender tells you how much money they will be able to lend you, at what rate, and at what terms. For example, the lender might say something like… “will give you $250,000 in mortgage, at an interest rate of 4% to be repaid in 25 years”. The pre-approval typically comes in a letter.

Getting pre-approval is a crucial step in the home buying journey since it will allow you to budget correctly for your house move. This means that you know what you can afford before you start visiting homes that are out of your price range, and making offers to buy.

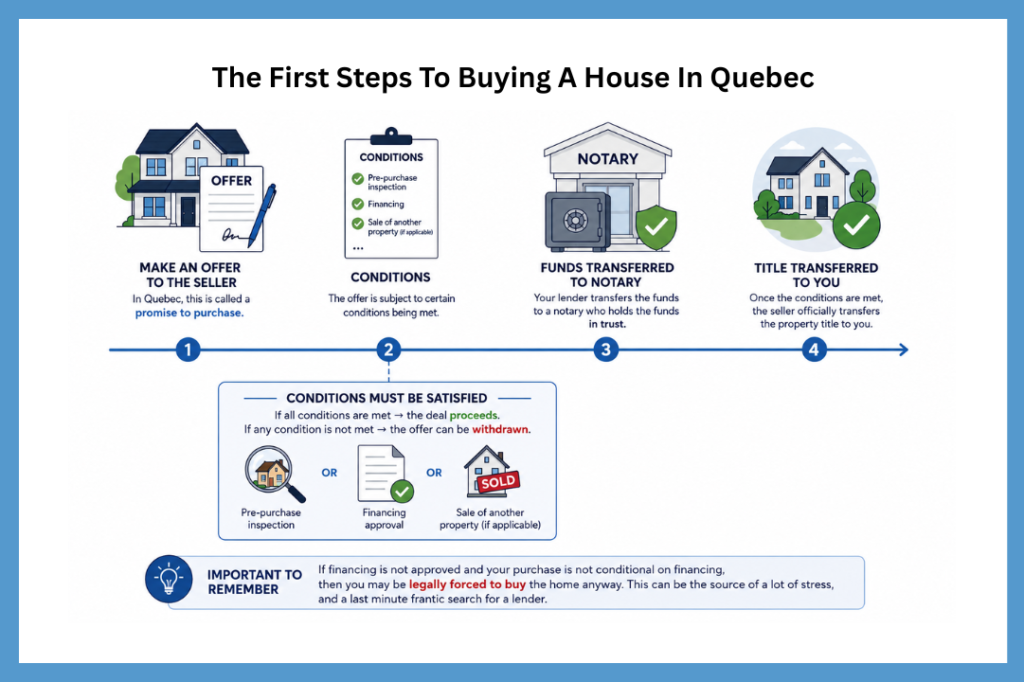

5. Missing conditions the promise to purchase

The first step to buying a house is to make an offer to the buyer. In Quebec, this is called a promise to purchase. Once this is done, you will go to your lender and ask them to transfer the funds to a notary who holds the funds in trust until the seller officially transfers the property title to you.

The promise to purchase is a legally binding agreement that it is very difficult to back out of. Essentially this says that you will buy the house at the price and on the terms agreed, once certain things (like a pre-purchase inspection, financing, or even the sale of another property) has taken place.

However, if the lender does not approve financing, and you have not made your home purchase conditional on financing, then you may be legally forced to buy the home anyway. This can be the source of a lot of stress, and a last minute frantic search for a lender.

Reputable no credit mortgage brokers in Montreal

If you have bad credit, working with the right mortgage broker can make a major difference. The brokers listed below specialize can help you get a mortgage with bad credit.

| Mortgage Broker | Specialty | Best For | Website |

|---|---|---|---|

| Team Levine | Alternative lending, refinancing, B lenders | Borrowers with bad credit or complex applications | Team Levine |

| Jason Zuckerman | Access to multiple lenders and flexible mortgage solutions | First-time buyers and low-credit borrowers | Jason Zuckerman |

| Morgan Englebretsen – Les Architectes Hypothécaires | Alternative mortgage solutions | Borrowers with non-traditional financial situations | Les Architectes Hypothécaires |

| Yelena Markus | Bad credit, self-employed, bank declines | Borrowers declined by traditional banks | Yelena Markus |

| Multi-Prêts Mortgages | Large broker network with B lender access | Comparing multiple lenders and rates | Multi-Prêts |

| Lauréat Finance | Private mortgage lending | Severe credit issues or urgent financing needs | Lauréat Finance |

Frequently Asked Questions

Generally, if a company advertizes loans that “guarantee approval”, they are just trying to get you on the phone and will then see what they can get you to buy something that they are selling.

Final Remarks

Although the details vary by province, it is possible to get a mortgage with bad credit in Canada. In each case, you should work with a mortgage broker who will help you to assess the options that you have. It is important to make sure that you understand everything that the mortgage broker explains to you, so that you don’t make a mistake that could end up jeopardizing your financial future.

Book a free consultation with a specilist below.

Free Consultation With a Specialist

Navigate the system with a professional mortgage broker who understands both traditional and alternative lenders. They can help you compare options and find the best solution based on your situation.