Credit Score Definition

A credit score is a three-digit number that represents your creditworthiness and how likely you are to repay borrowed money on time.

Note: Whilst credit scores work roughly the same way in the USA and Canada, there are some key differences. This guide looks at how the Canadian systems works.

Imagine that one of your friends comes up to you and asks to borrow some money.

Depending on who that friend is, you probably have a pretty good idea about if they will pay you back or not. Now image three total strangers approach you and ask to borrow some money. Which of these strangers is most likely to pay you back?

This is the problem that lenders face everyday. When strangers ask them to borrow money for a mortgage, a car, or a short term pay day loan, the lender needs a way to assess how likely it is that the person will pay them back on time, and in full.

This is where credit scores come in.

What is a Credit Score?

Your credit score is a three digit number that represents how risky it is to lend money to you, based on how you’ve managed borrowed money and financial obligations in the past. In Canada, your score will typically fall somewhere between 300 and 900.

If you are reliable, and always pay your debts on time and in full, then you will likely have a good credit score. If you are unreliable, and often pay your debts late, or sometimes not at all, then you will likely have a low credit score.

You can check your credit score for free @ LoansCanada which offers one of the most reliable and easy-to-use credit score tools in Canada.

Why is Your Credit Score Important?

Your credit score is the primary metric that a bank, or another lender, will use to assess your creditworthiness. This means, that your credit score helps lenders determine how likely it is that you will pay them back on time and in full.

If you have a high credit score, then businesses and private individuals are more likely to lend you money. Whereas, if you have a low credit score, then lenders will either refuse to lend you money or will only approve you at higher interest rates and stricter terms. This means that it makes it harder and more expensive to borrow money for things like a mortgage, if you have a bad credit score.

✨ Tip

Did you know that lenders aren’t the only ones who look at your credit score? Landlords also review your credit score to help them decide whether they can trust you to pay your rent and bills on time and in full.

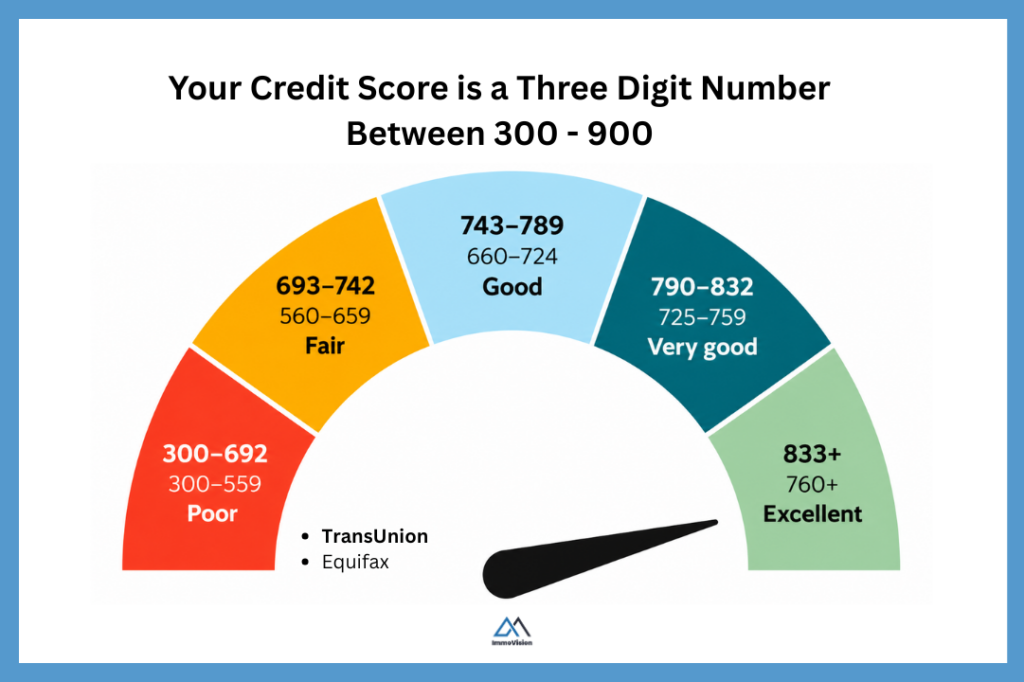

What is Considered a Good Credit Score in Canada?

In Canada, your credit score is calculated by the two major credit bureaus: TransUnion and Equifax. These are private companies that collect, track, and report information about your credit history to lenders.

Both credit bureaus group credit scores into a few simple ranges that lenders can easily understand. Depending on your score, you’ll fall into one of these ranges. For example, if your score is between 700–800, then this is considered a good credit score.

Both credit bureaus have slightly different scoring ranges and classifications. The table below shows these credit ranges, and what most lenders determine those ranges to mean.

| TransUnion Score Range | Equifax Score Range | Credit Rating | What It Means |

|---|---|---|---|

| 300–692 | 300–559 | Poor | Low credit score. Approval is unlikely, and loans usually come with high interest rates. |

| 693–742 | 560–659 | Fair | Below-average credit. You may qualify, but expect higher rates and stricter terms. |

| 743–789 | 660–724 | Good | Good credit score. Most lenders will approve you at standard interest rates. |

| 790–832 | 725–759 | Very Good | Strong credit profile. Higher approval odds and access to better loan terms. |

| 833+ | 760–900 | Excellent | Excellent credit score. Qualify for the lowest interest rates and best lending options. |

How is Your Credit Score Calculated?

In Canada, your credit score is calculated by one of two major credit bureaus: TransUnion or Equifax. These are private companies that collect and maintain detailed records of your financial history.

They gather large amounts of data about your past behavior from sources such as banks, credit card companies, and debt collection agencies. This information is stored in giant data warehouses which are, essentially massive collections of structured financial records.

Using this data, the credit bureaus apply proprietary mathematical formulas to calculate your credit score. TransUnion primarily provides scores based on the FICO model as well as its own internal scoring model, CreditVision. Equifax, on the other hand, uses both the VantageScore model and its own proprietary system, known as the Equifax Risk Score (ERS).

The exact methods behind these formulas are not publicly disclosed and, each model uses different data inputs and weighs factors such as missed payments, on time payments, length of credit history differently. This is one of the reasons why you will receive different scores depending on which bureau or scoring model is used.

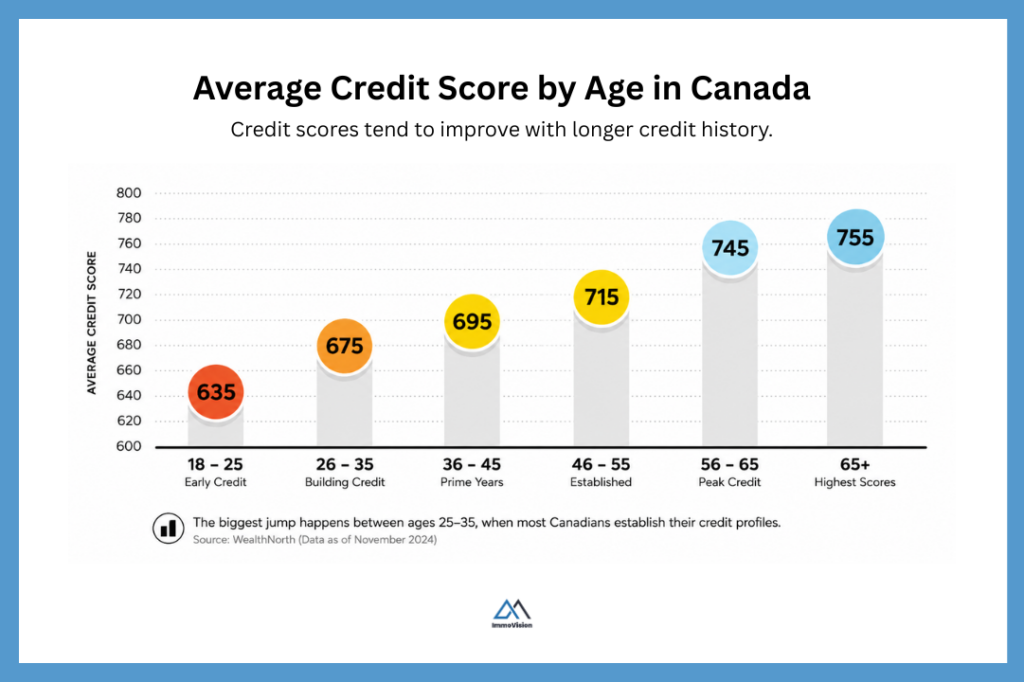

What is the Average Credit Score in Canada?

As of November 2024, the average credit score in Canada was 760, according to the Fair Isaac Corporation (FICO®), one of the most widely used credit scoring companies globally.

This places the majority of Canadians in the “very good” range. However, for most lenders, anything above 660 is still generally considered a strong score.

The average credit score also varies widely depending on age and time in Canada. For instance, younger Canadians with less established credit histories tend to have lower scores, compared to older Canadians or those with longer, more established credit profiles. For instance, 18 – 25 year olds tend have on average the lowest credit score of 635 and, Canadians who are 65+ tend to have the highest.

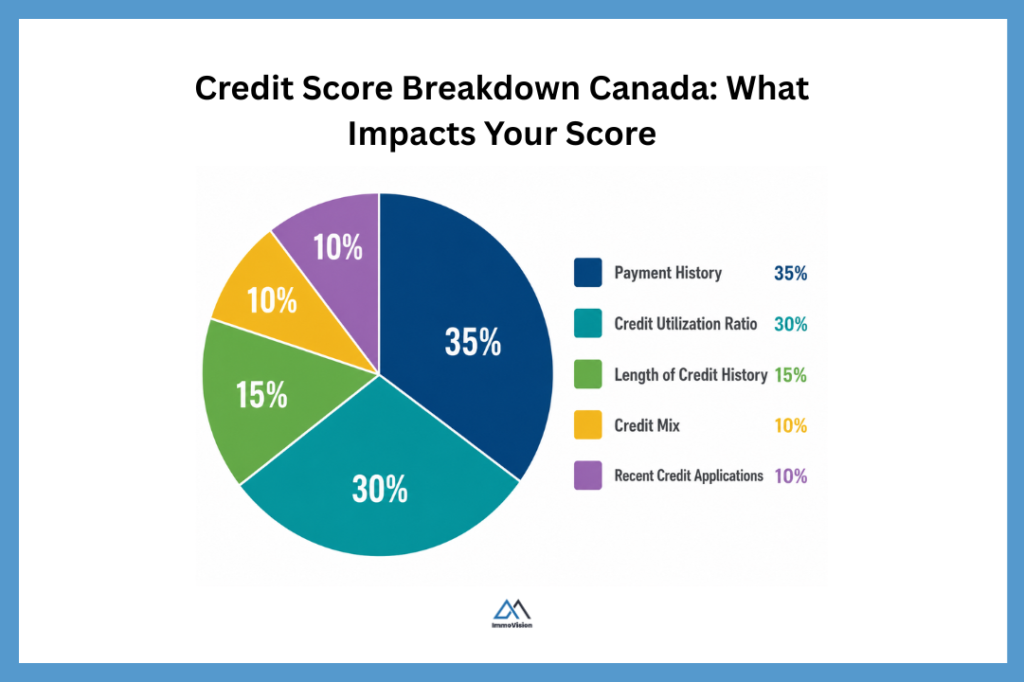

Factors That Influence Your Credit Score

Your credit score fluctuates based on a variety of factors. The top five factors that impact your credit score are:

- Payment History

- Credit Utilization Ratio

- Length of Credit History

- Credit Mix

- Recent Credit Applications

Not all factors carry the same weight—some have a much bigger impact on your credit score than others. The graphic below shows how each factor contributes to your overall score. These figures are based on Equifax Canada’s weighting of factors, which is similar to TransUnion.

Payment History

The most important factor that impacts your credit score is your payment history. In short, your payment history is all about whether or not you pay your bills on time. This includes things like student loans, mortgage payments, car payments, and credit card payments.

The main thing that lenders want to know is, are you going to pay them back on time and in full. If you pay your bills on time every month, then your payment history will be flawless. However, if you are late on your payments, your credit score will drop. If you default on a payment entirely and the lender charges off debt and transfers it to a collector, your credit score will be negatively impacted in a significant way.

In Canada, all missed payments, or defaulted payments remain on your credit score for between 6 – 7 years.

Credit Utilization Ratio

Lenders want to see that you live in a financially responsible way. If you max out your lines of credit every month, and finance all major purchases with credit, then lenders will think of you as someone who relies heavily on credit. According to the statistical models, this behavior is associated with a higher likelihood of missed payments, which makes you a higher risk borrower.

There are two types of credit that most people have:

- Long term debt (or instalment loans) – like student loans, home mortgages, and car loans – are typically paid off in monthly payments made over time.

- Short-term revolving credit—like credit cards, lines of credit, and overdraft protection—is typically paid off in full at the end of each month.

If you’ve recently taken on a large loan, your credit score may dip at first, but as you pay it down, it can work in your favour. For example, if you bought a home with a $500,000 mortgage and have made only one payment, your score may be lower since most of the debt is still outstanding. By contrast, if you have paid off 80% of the mortgage, this shows a strong repayment track record and can positively impact your score.

For short term revolving credit, if you keep your credit usage below 30%, this signals that you are using credit conservatively and managing it well. For example, let’s say that you have a $10,000 limit on your credit card. You should aim to keep your balance below $3,000 (or 30% of your credit card limit). The lower that you keep it, the better your credit rating.

Length of Credit History (the Longer the Better)

Your credit history is the length of time that you have had each of your different accounts active. If you took out a student loan 12 years ago then that account is 12 years old. Similarly, if you got a new credit card 5 years ago and you kept it active, that account is 5 years old.

Your credit score looks at the average age of all your active accounts. Once an instalment loan is paid in full, it no longer counts to the length of your credit history. This means that, if it was an old account that you paid off, this will actually hurt your credit score.

✨ Tip

If you need to close a credit card, it is usually better to close a newer card rather than an older one. This is because older accounts help increase the average age of your credit history, which can positively impact your credit score.

Credit Mix

Lenders like it when you have a wide variety of active accounts. This is because, if you can handle a mix of different types of credit such as a mortgage, credit card, and car loan, it shows that you can handle different types of credit responsibly.

Of course, you should only use different types of credit if it makes sense for you. There is no point taking on more debt just for optics.

Recent Credit Applications

When you apply for a new line of credit—be it a mortgage, credit card, or car loan—the lender will run a “hard check” on your credit report. This means the lender is formally pulling your full credit report from one or more credit bureaus and recording that access on your file. This can cause a dip in your credit score because it signals that you may soon take on new debt, which increases your perceived risk as a borrower.

Not all credit checks are “hard checks.” There are also “soft checks,” which occur when your credit report is reviewed without a formal application for new credit. For example, let’s say you check your own credit score, or a landlord runs a background or a lender runs a pre-approval check. Soft checks are only informational and do not affect your credit score.

✨ Tip

Hard inquiries typically stay on your credit report for up to two years. In general, having one or two hard checks over that period is unlikely to significantly impact your credit score.

How to Check Your Credit Score (For Free)

It is easy to check your credit score and you can do this for free without hurting your credit score @ LoansCanada. We run credit checks all the time, and this platform offers one of the most reliable and easy-to-use credit score tools in Canada.

Since your credit score plays such an important role in your life, it’s a good idea to check it regularly. This will help you stay on top of your credit health, spot errors early, and take steps to improve your score over time.

How to Improve Your Credit Score

The best way to improve your credit score depends on why your score is low.

For example, if your score dropped because of a missed payment that resulted in an R9 rating on your credit report, your strategy will depend on how quickly you need to rebuild your credit and your current financial situation. That said, here are six proven ways to improve your credit score in Canada:

| Strategy | How It Helps Your Credit Score |

|---|---|

|

💳 Pay Off Your Debts On Time

|

The most effective way to improve your credit score is to consistently pay all your debts on time and in full. Payment history is the biggest factor affecting your score. If you’ve missed a payment, bring the account current as soon as possible. If it has been charged off, consider negotiating a settlement. Resolving these accounts can still improve your credit over time. |

|

📉 Keep Your Credit Usage Low

|

Aim to keep your credit utilization below 30% on revolving credit like credit cards and lines of credit. For installment loans, focus on steadily paying down balances. This shows lenders you can manage credit responsibly. |

|

🚀 Start Building Credit Early

|

Building credit takes time, so start as early as possible. Even a low-limit credit card, when used responsibly, helps establish your credit history and improves your score over time. |

|

🛠️ Fix Errors on Your Credit Report

|

Negative information can stay on your report for 5–7 years in Canada. However, errors like incorrect balances, duplicate accounts, or wrongly reported late payments can be disputed and removed. Regularly checking your report helps catch these issues early. |

|

📅 Keep Old Accounts Open

|

A longer credit history improves your score. Keep older accounts open—even if unused—to maintain the average age of your credit. Closing them can shorten your history and lower your score. |

|

🔍 Avoid Too Many Hard Checks

|

Hard inquiries occur when applying for credit and can slightly lower your score. Having more than 2–3 in a year may negatively impact your credit. These stay on your report for up to 2 years. |

Frequently Asked Questions

Payment History Changes:

If you’ve recently missed a payment or defaulted on a debt, this can significantly impact your credit score, especially if it’s reported as late. If the account hasn’t been charged off, you can often recover by bringing all payments up to date. However, if it has been charged off, you’ll need to repay the debt in full or negotiate a settlement to begin rebuilding your credit.

High Credit Utilization:

If you’ve recently taken on more debt or increased your credit card balances, your score may drop. This is because credit bureaus closely track how much of your available credit you’re using. A higher utilization ratio signals increased risk to lenders.

Hard Credit Checks (Inquiries):

When you apply for new credit and authorize a lender to perform a hard inquiry, it can slightly lower your credit score. Multiple inquiries in a short period can have a larger impact.

Closing Accounts or Paying Off Loans:

Closing a credit card or paying off an installment loan can affect your credit history and utilization. This may shorten your average account age or reduce your total available credit, both of which can cause a temporary dip in your score.

A hard check can lower your credit score slightly (typically a few points), and the record of the inquiry will stay on your credit report for up to 2 years. If you authorize multiple hard checks within a short period, the impact can be greater. This is because credit bureaus may interpret multiple applications as a sign that you’re taking on more debt, which increases your perceived risk to lenders.

A soft credit check (soft inquiry) occurs when your credit is reviewed without a formal application for credit. Common examples include checking your own credit score, pre-approval or pre-qualification offers, or a landlord running a background check.

This type of credit inquiry does not impact your credit score. In fact, regularly performing soft checks is a smart habit—it helps you monitor your credit health and ensures that when you apply for credit, you’re in a strong position to qualify for the best rates and terms.

Final Remarks

A good credit score gives you allows you to borrow money at the best rates. This means that, you will pay less to borrow the same amount as your peers. Conversely, a low credit score makes it harder to borrow money and, in some cases, you will be denied credit entirely.

Because your credit score can change on a regular basis, it is important to stay up to date with your credit report and score. This will allow you to know not only what your score is today, but also give you insights into how to improve your score before the critical moment when you need to borrow money.

You can check your credit score for free @ LoansCanada which offers Canadian’s a free tool to check your credit score.