Definition of a Charge Off

A charge off means that a lender or creditor has written the account off as a loss, and the account is closed to future charges. Once the account becomes a charge off, the lender or creditor may transfer it to a debt collection agency. You are still legally obligated to pay a debt that becomes a charge off.

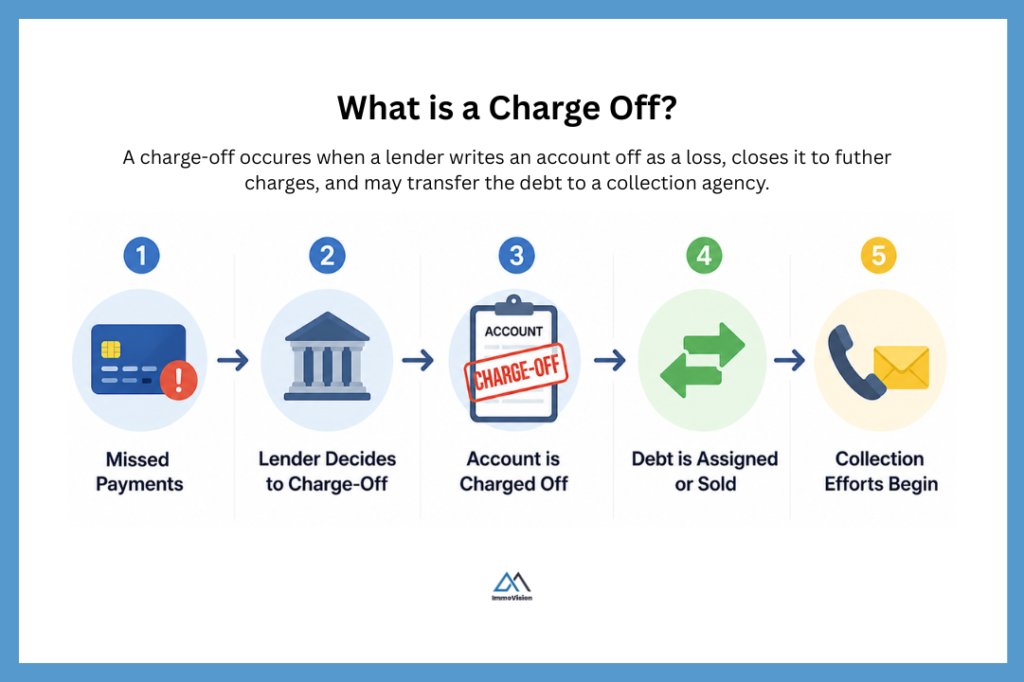

What is a Charge Off?

A charge-off occurs when a lender or creditor writes an account off as a loss, closes it to further charges, and may transfer the debt to a collection agency. The borrower still owes the debt, and the collection agency will typically follow up to recover the outstanding amount.

To understand how this works, imagine you owe money on a credit card or phone bill. The business sends multiple reminders, but you’re unable to make the payments. After a certain amount of time, the business (who at this point is actually lending you money, since you have not paid) decides that they are no longer going to get the money and so they decide to “charge off” the debt.

When this happens, the lender marks the account as a “charge-off” in its accounting records, closes the account, and stops allowing further charges. The lender may then assign the debt to a collection agency or sell it to a debt buyer. The collection agency will begin contacting you through calls, letters, or other methods to recover the balance. You still legally owe the debt, but you may now owe it to a collection agency or a new owner of the debt, depending on whether it was assigned or sold.

How Long Before A Charge Off Happens?

Creditors may mark a debt as a charge-off at any time without waiting for it to reach a specific age, such as 90 days. However, most lenders wait for around 180 days since the time when the account went delinquent. This is because it is cleaner from an accounting standpoint and, it gives them adequate time to collect up the debt.

However, even if debt does not reach the status of a charge off, it may still have an impact on your credit score. This is because in Canada, lenders report missed payments using a rating scale from R1 (best) to R9 (worst). As an account becomes more delinquent, its rating worsens over time:

- R1 – Paid on time

- R2 – 1–30 days late

- R3 – 31–60 days late

- R4 – 61–90 days late

- R5 – 91–120 days late

- R7 – Special arrangement (e.g., payment plan)

- R8 – Repossession (secured loans)

- R9 – Sent to collections, written off, or uncollectible

As you miss payments, your account typically moves from R2 → R3 → R4 → R5. At each stage, lenders report increasing delinquency to the credit bureaus. Each time the lender reports a stage of delinquency, the negative impact on your credit score becomes more severe, with R9 being the most severe.

Will a Charge Off Impact Your Credit Score?

Yes—a charge-off will significantly impact your credit score. From our research, we found that charge offs tend to drop your credit score from between 50 – 150 points.

Typically, serious impact to your credit score happens when a creditor marks the debt as a charge off, assigns it an R9 rating, and transfers it to a collection agency who will pursue you for the money. However, the credit bureau will still give you a negative hit to your credit score for every increasingly delinquent R rating reported.

How Does a Charge Off Show Up on my Credit Score in Canada?

In Canada, a “charge-off” usually doesn’t appear as a single, clearly labeled item. Instead, it shows up in a few different ways on your credit report, depending on the credit bureau’s terminology and how the lender reports the account.

- R9 (worst rating): The lender or collection agency reports the account as an R9 to the credit bureaus. This is the most severe credit rating. It indicates that you have not repaid the debt as agreed and / or the lender has sent the debt to collections.

- In collections: If the lender sends or sells the debt to a collection agency, you’ll typically see a separate collections account on your report. This is one of the most visible indicators of a defaulted or charged-off debt.

How Long Does a Charge Off Stay on Credit Reports?

Typically a charge off will remain on your credit report for up to ~6 years in Canada (depending on the bureau and province rules).

In Quebec, both major credit bureaus (Equifax Canada and TransUnion Canada) report that a charge-off can stay on your file for up to six years. This six-year period generally begins from the date you first became delinquent on the account and not from the date the lender officially wrote off the debt.

You can change the status of your charge off. For instance, if it is an R9 then you can pay off the debt and this will turn the R9 into an R5 which, is essentially a “paid collection”. This just means that you have paid off the debt.

⚠️ Important

Even if you enter a payment plan on an account marked R9, regular payments usually do not change the rating. The only way to change the rating is to settle the debt.

For this reason, many debt specialists suggest negotiating a reduced lump-sum settlement instead of making lots of partial payments over a long time horizon.

If I Pay Off the Debt Will the Charge Off Remain On My Credit Report?

Yes! Even if you pay off the debt, a charge off will remain on your credit report. However, when the collection agency or debt buyer reports it as paid to credit bureaus, the charge off will change to a “paid status”. This will update your R9 status to an R5 status. This status will stay on your credit report for up to six years, even after you pay it off.

How to remove a charge off from your credit report?

In Canada, the law requires that credit bureaus ensure that the information on your credit report is accurate. This means that if any information is incorrect, they must investigate and correct it. However, it also means that lenders and credit bureaus cannot simply remove a charge off, if it is accurate. This requirement comes from the Personal Information Protection and Electronic Documents Act (PIPEDA).

Because of this requirement for accuracy, the only way to remove a charge-off from your credit report is if there is a factual error or the information cannot be properly verified. To remove a genuine error, you can take the following steps:

- Step 1: Identify the error

- Step 2: Gather supporting docs

- Step 3: File a dispute with the credit bureau

- Step 4: Wait for a response

Step 1: Identify the error

The most common mistakes include:

- Inaccurate personal details: Errors in your name, address, or date of birth that can lead to a credit bureau assigning you someone else’s credit information (or vice versa).

- Wrong account information: Incorrect balances, payment histories, or account statuses (for example, showing a missed payment when you paid on time).

- Falsified or stolen accounts: Identify theft and fraud Identity can harm your credit score. Someone may open an account in your name and leave the debt unpaid under your profile. If you spot unfamiliar accounts, report them immediately and dispute them with the credit bureau.

- Uncorrected negative information: Charge offs stay on your report for up to ~6 years (unless due to an error or fraud). A credit bureau may forget to remove the information after the allotted time period.

Step 2: Gather supporting docs

When you dispute a charge off, you’ll need to provide evidence to support your claim. This can include receipts, account statements, or other relevant documents. You will need to provide:

- The name of the company linked to the item

- The account number in question

- A clear explanation of why you are disputing it

Providing complete and accurate information helps speed up the investigation process.

Step 3: File a dispute with the credit bureau

To file a dispute with a credit bureau, you first need to identify which credit bureau is reporting the error. You can then follow their specific dispute process online.

Equifax Canada

You can file a dispute with Equifax Canada either online or by mail.

Equifax Canada Co.

Consumer Relations Department

Box 190, Jean Talon Station

Montreal, QC H1S 2Z2

Transunion Canada

You can file a dispute with Transunion Canada either online, by phone, or by mail.

English: 1-800-663-9980

French: 1-877-713-3393 or 514-335-0374

TransUnion Consumer Relations

P.O. Box 338, LCD1

Hamilton, ON L8L 7W2

4. Wait for a response

The credit bureau will review your dispute and carry out an investigation, which may include contacting the creditor or lender that provided the information.

If the lender acknowledges a mistake, the credit bureau may remove the entry from your credit report. However, if the lender verifies that the information is correct, it will remain on your report unchanged.

Frequently Asked Questions

Can my account be charged off even if I’ve been making payments?

Yes, a lender may charge off your account if you do not satisfy the account terms such as, minimum payment requirements, payment due dates, use of account as agreed, and so on. A lender may also charge off the account if you file for bankruptcy.

How to remove a charge off from your credit report?

In Canada, the only reliable ways to remove a charge-off from your credit report are:

- If the information is inaccurate

- Wait ~6 years until the charge off is automatically removed

Many online resources say that you can pay or settle the debt to remove the charge off. However, this does not remove the charge off, it only updates the status to show it as paid or settled. This can improve your credit score, but it will not reset the account or erase the original negative history.

What is a charge off vs a write off?

Both of the terms “charge off” and “write-off” are accounting terms that a lender or creditor uses to reclassify debt. The two terms fundamentally refer to the same underlying event, but they are used in slightly different contexts:

- Charge-off is typically used in credit reporting

- Write-off is more commonly used in accounting and financial reporting within the lender’s internal books and financial statements

When a lender issues credit, the money that is owed to the lender is recorded as a receivable (an asset) on their books. This means that the lender expects repayment. If the borrower stops making payments and the account becomes severely delinquent, the lender will eventually determine that the debt is unlikely to be recovered. At that point, the lender removes it from active receivables and records it as a loss through a write-off (or reports it as a charge-off in credit reporting terms).

In this case, the debt is no longer treated as an active asset, but the borrower may still legally owe the money, which can then be pursued through collections or sold to a third-party collection agency.

What is a charge off vs a collection?

A charge-off is when a lender writes your account off as a loss after a period of non-payment, whereas a collection is when that debt is assigned or sold to a third-party agency that attempts to recover the money.

To understand how this works, imagine a lender marks your account as a charge-off. This means they no longer expect to be repaid and have updated your credit report accordingly, often with an R9 rating. At that point, the lender may either leave the account as is or transfer it to a collection agency.

If the account is sent to collections, the collection agency will then report its own entry on your credit report, indicating that the debt is now being actively pursued.

Final Remarks

A charge-off is one of the most serious negative items that can appear on your credit report in Canada.

The key thing to understand is that a charge off simply means that you have failed to repay what you owe within a reasonable time frame. It is not the end of your obligation. You still owe the debt, and it may continue to affect your credit through collections or ongoing reporting. However, over time, its impact will gradually lessen, especially if you take steps to rebuild your credit.