If your mortgage renewal date is approaching, you may be wondering whether you are getting the best deal possible from your lender. The good news is that renewing your mortgage is also an opportunity to negotiate a lower interest rate, reduce your monthly payments, and potentially save thousands of dollars over the next mortgage term.

In this guide, we explain everything you need to know about mortgage renewals in Quebec. This includes how the renewal process works, when to start preparing, how to compare offers, and what strategies you can use to negotiate a better rate with your lender.

Even a small difference in your mortgage rate can have a major impact over time, so taking the time to understand your options is well worth it.

ℹ️ Note

This article focus is on the mortgage renewal process in Canada, and more specifically in Quebec. Mortgage renewal rules and lending practices may be different in the United States and other countries.

What is mortgage renewal?

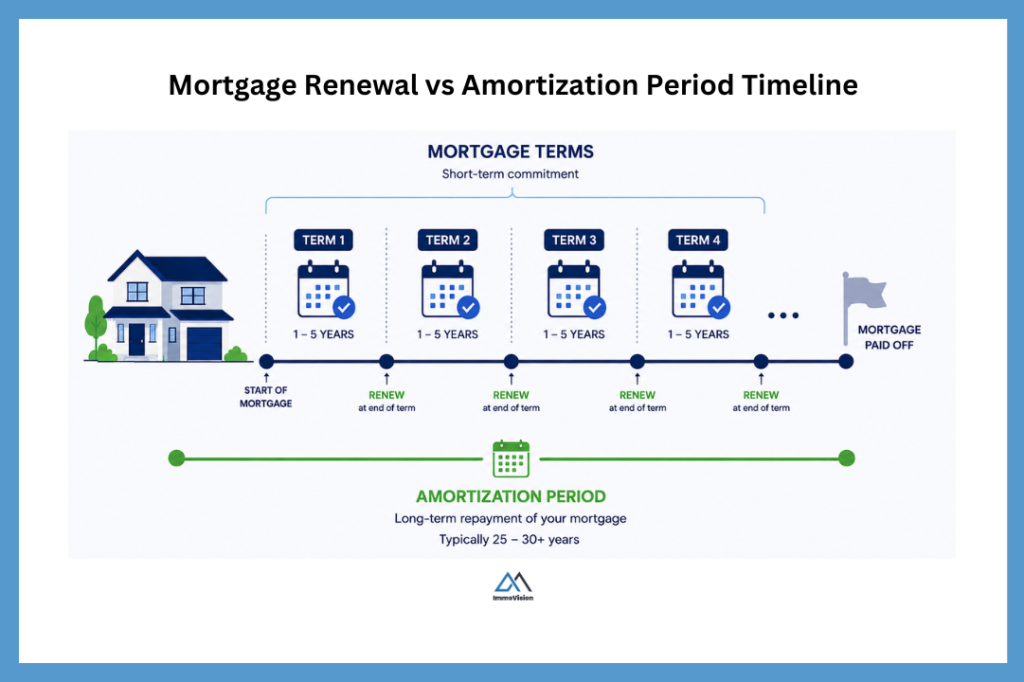

A mortgage renewal is the process of signing a new mortgage term with your current lender when your existing mortgage term ends, without changing lenders or borrowing additional money.

In Quebec, most mortgage terms last between 1 and 5 years, even though the full amortization period may be 25 years or longer. At the end of each term, borrowers must either: renew their mortgage with the same lender, refinance their mortgage, or switch to a new lender.

What happens during a mortgage renewal in Quebec?

Four to six months before your mortgage renewal date, your lender will typically send you a renewal offer outlining the proposed terms for your next mortgage term. This offer usually includes a new interest rate, term length, and estimated monthly payments. Depending on market conditions, the renewal rate may be higher than your current rate and could increase your monthly payments.

According to Canadian mortgage broker Alexander Gasenko, “the banks send renewal offers months in advance, normally with a higher than average rate, hoping that you, like most of their other customers, will blindly sign it without doing your homework”.

If you sign the offer — or in some cases take no action before the renewal date — your mortgage may renew under the lender’s proposed terms. While this can be convenient, the initial offer is not always the most competitive rate available. As Alexander explains “the banks first offer is normally not the best”.

Instead of accepting the first offer you should take the opportunity to compare rates, speak with a mortgage broker, and negotiate with your lender. Even a small reduction in your interest rate can lower your monthly payments and potentially save thousands of dollars over the next mortgage term.

ℹ️ Note

In Quebec, if your mortgage contract is with a federally regulated financial institution, such as a bank, the lender must provide you with a renewal statement at least 21 days before the end of the existing term. Your lender must also notify you 21 days before the end of your existing term if they won’t renew your mortgage.

How to negotiate your mortgage renewal?

Once you have your banks offer in hand, the next step is to get multiple offers on the table, and to see if you can get a better rate elsewhere. To do this, you should do the following:

- Check current market rates

- Counter your banks offer

- Get ready to switch lenders

- Make your final decision

1. Check current market rates

First, you should compare the rate your lender offered with current market rates to determine whether it is competitive. While you can search for mortgage rates online, the rates advertised are often promotional or generic rates used for marketing purposes. The actual rate you qualify for will depend on your specific financial profile, including factors such as your credit score, income, equity in your property, and property type.

Because of this, it is often best to speak with a mortgage broker, who will know which lenders are currently offering the most competitive rates for borrowers in a similar financial situation. A broker can compare offers from multiple lenders on your behalf, provide you with a range of available rates, and help you understand which options you are most likely to qualify for.

Need a mortgage broker?

Connect with a top Canadian mortgage broker and receive multiple competitive mortgage offers tailored to your situation within 24 hours.

2. Counter your banks offer

The next step is to counter your bank’s renewal offer. This is completely normal and your lender will expect this during the mortgage renewal process, especially if the lender did not initially offer you their most competitive rate.

You can negotiate by phone or email, although it is often helpful to start with a phone call and then follow up in writing afterward. Keep in mind that the bank representative is simply doing their job, so there is no benefit to being aggressive or confrontational. In most cases, a calm and professional approach will lead to better results.

A good strategy is to mention that you have received a competing offer from another lender and share the interest rate you were offered. To strengthen your position, it is helpful to obtain a written mortgage quote or approval from another lender. This shows your bank that you are seriously considering switching lenders if they cannot offer a competitive rate.

Banks understand that losing an existing mortgage client can be costly, so a competing offer may encourage them to lower your rate or improve your renewal terms.

💡 Top Negotiation Tip

In negotiations, the side that controls the timeline often has the advantage. Because of this, it is important to begin the renewal process early rather than waiting until the last minute.

Ideally, you should start comparing rates and negotiating with lenders 3 to 6 months before your renewal date. This gives you enough time to explore alternatives, negotiate effectively, and avoid feeling pressured into accepting a less favorable offer because your renewal deadline is approaching.

3. Get ready to switch lenders

During the negotiation process, it is important to be prepared to switch lenders if necessary. This means understanding both the process involved and the potential costs of making the switch.

In most cases, switching mortgage lenders is relatively straightforward — especially if you are working with an good mortgage broker. Your broker will typically handle most of the paperwork, coordinate with the lenders, and guide you through the process. In many cases, your main responsibility will simply be reviewing and signing the required documents. Your broker can also help explain the mortgage terms and answer any questions you may have before you sign.

There are usually some costs associated with switching lenders. These may include:

- Home appraisal fees,

- Legal fees for transferring the mortgage,

- Discharge or registration fees, and

- Administrative costs.

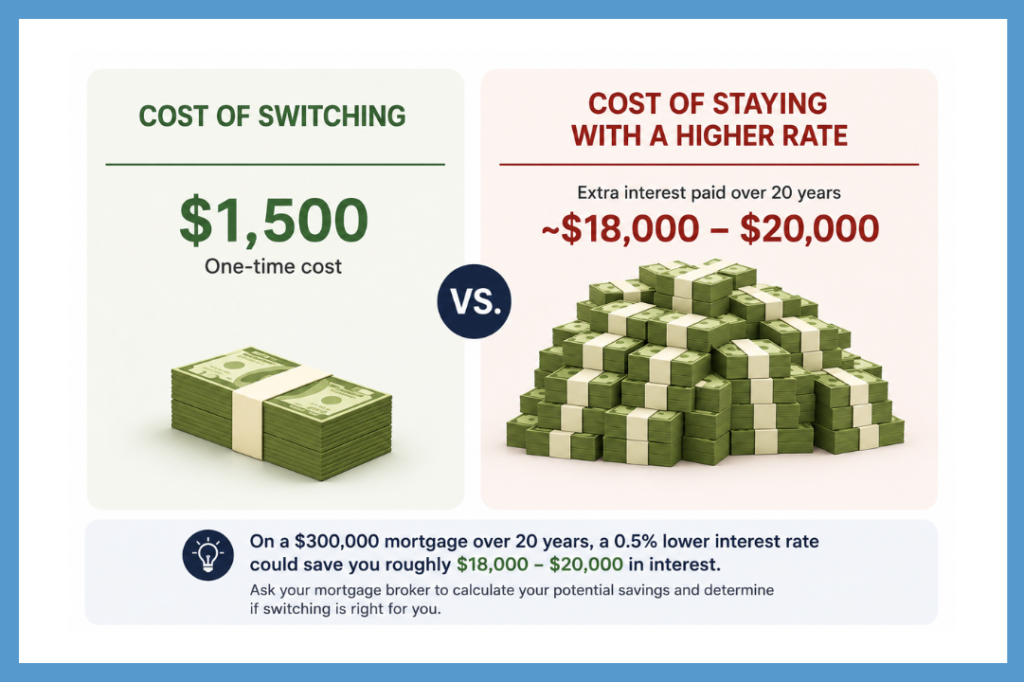

Depending on the lender and province, these costs can add up to $1,500 or more. However, even a small difference in interest rates can result in significant long-term savings.

For example, on a $300,000 mortgage amortized over 20 years, a 0.5% lower interest rate could save you roughly $18,000–$20,000 in interest over the life of the mortgage. Compared to those potential savings, $1,500 in switching costs may be relatively minor.

Because every situation is different, ask your mortgage broker to calculate the potential savings for you and help determine whether the upfront cost of switching lenders is worthwhile based on your financial goals.

💡 Bonus Tip: Ask for a "Rate Hold"

If you find a competitive mortgage rate, ask your broker to place the rate on hold for you. In the mortgage industry, this is called a “rate hold.”

A rate hold allows a lender to guarantee a specific interest rate for a set period of time — often up to 120 days. You can think of it as a form of insurance against rising interest rates.

If rates increase during the rate hold period, you will still have access to the lower locked-in rate. On the other hand, if rates decrease, many lenders will still allow you to qualify for the lower rate instead.

Because of this, there is generally very little downside to securing a rate hold early, aside from the time required to complete the application paperwork with your mortgage broker.

4. Make your final decision

Now that you have all the available information, it is time to decide whether you want to switch lenders or accept your current bank’s renewal offer.

Your mortgage broker may prefer that you switch lenders because they will typically earn a commission on the new mortgage. Likewise, your bank will want you to renew with them so they can continue earning interest on your mortgage throughout the next term. However, this should ultimately be treated as a financial decision, meaning you should choose the option that is best for your situation.

Once you have made your decision, it is a good idea to clearly communicate it to both parties and explain your reasoning in a respectful and professional manner. Maintaining positive relationships with both your bank and mortgage broker can be beneficial, especially if you need them to work together to coordinate the switch of the mortgage.

Why some mortgages are harder to switch at renwal

Your lender may have registered your mortgage using a collateral charge. This means your mortgage may have been registered for an amount greater than your current mortgage balance. One benefit of this structure is that it can make it easier to access additional borrowing in the future, such as a home equity line of credit (HELOC) or other lending products secured against your home.

However, if you have used this additional borrowing capacity, switching lenders at renewal can become more expensive or more complicated. In general, all debts secured by the collateral charge will need to be repaid or transferred to the new lender before the mortgage can be moved.

If you have not borrowed any additional funds against your home, a collateral charge is less likely to create issues, although some lenders may still require additional legal work when transferring the mortgage.

To find out if your mortgage has a standard or a collateral charge, ask your lender, lawyer or notary.

Mortgage insurance rules when switching lenders

When you switch mortgage lenders at renewal, your new lender may require mortgage loan insurance if you increase the size of your mortgage or stretch out the amortization period (for example, going from 20 years back to 25 or 30 years).

If you have already insured your mortgage through Canada Mortgage and Housing Corporation (CMHC), Sagen, or Canada Guaranty, tell the new lender. In most cases, you can transfer the insurance policy to the new mortgage so that you do not have to pay the insurance premium a second time. To help with this, your current lender can provide the insurance certificate number, which helps the new lender confirm the existing coverage.

When switching lenders, you will also need to sign legal documents to transfer the mortgage registration. In Quebec, you will typically need a notary to help you sign legal documents.

Frequently asked questions

– Missed or late mortgage payments

– Major increase in debt

– Reduced income or job loss

– Poor credit score

– Property value concerns

– Separation/divorce affecting finances

– The lender tightening its lending rules

Depending on your situation, you may want to speak with your mortgage broker about switching to a B lender or another type of alternative lender. This can sometimes serve as a temporary solution while you address the issues that are causing concern for your current lender, such as a low credit score, high debt levels, missed payments, or unstable income.

If switching lenders is not possible, selling the property before the lender begins foreclosure proceedings is often the better financial option. By selling the home yourself, you may be able to preserve more of your equity and maintain greater control over the process.

To do this, you should contact a real estate agent as soon as possible and create a plan to sell the property fast. Acting early may help you avoid additional legal costs, protect your credit as much as possible, and recover any remaining equity from the sale of the home.

Final remarks

Mortgage renewal in Quebec typically comes around every 1 to 5 years and, it gives homeowners an good opportunity to review their mortgage, compare lenders, and potentially negotiate a better interest rate.

While many borrowers simply accept their bank’s first renewal offer, taking the time to shop around and negotiate can lead to meaningful savings over the next mortgage term.

At the same time, mortgage renewals are not always straightforward. Factors such as collateral charge mortgages, switching costs, mortgage insurance rules, and changing qualification requirements can sometimes make the process more complicated than expected. The best approach is to start early, compare multiple offers, and work with an experienced mortgage broker who can help you find the best rates, understand your options and negotiate on your behalf.

Need a mortgage broker?

Connect with a top Canadian mortgage broker and receive multiple competitive mortgage offers tailored to your situation within 24 hours.