B lenders play an important role in Canada’s housing market. In short, they provide mortgage financing to borrowers who do not qualify with traditional banks or credit unions like RBC, Desjardins, or Scotiabank.

Whilst B lenders fill a very real gap in mortgage financing, borrowers tend to think of them as an untrustworthy financing solution. Oftentimes you will hear stories of B lenders who charge mythically high fees and interest rates compared to A lenders, and have oppressive or even insidious contractual terms.

In reality, B lenders compete for your business and (just like A lenders) they do this by creating mortgage products that are better suited to specific segments of the market.

Borrowers who take the time to explore the B lending market can sometimes find competitive rates, more flexible qualification criteria, and financing solutions that better match their financial situation — even if they would normally prefer to work with a major brand-name lender.

In this article, we will help you understand exactly what a B lender is, what their mortgage products typically look like, and which borrowers benefit most from them.

Free, No Obligation Mortgage Consultation

Book a call with a licensed mortgage broker, to get a game plan for your specific case.

What is a B lender mortgage?

In Canada, the term “B lender” is an informal industry label rather than a regulated classification. Generally it refers to financial institutions that provide mortgages to borrowers who do not qualify under the stricter lending criteria used by traditional banks.

Industry professionals often refer to this type of borrower as “subprime” or “near-prime” borrower. Subprime borrowers may have low traditional credit scores, non-traditional income, higher debt levels, or other factors that make qualifying with an A lender more difficult.

Whilst B lenders will not approve everyone that an A lenders rejects, they do have a more flexible qualification criteria. It is this flexibility, that helps borrowers with credit challenges get a mortgage.

Borrowers who qualify with A lenders may also want to investigate B lenders since certain types of B lenders (e.g. monoline lenders) often have better mortgage products than A lenders.

ℹ️ Note

Private lenders are not the same as B lenders. Private lenders will lend money to just about anyone provided that there is enough equity in the property to adequately secure the loan.

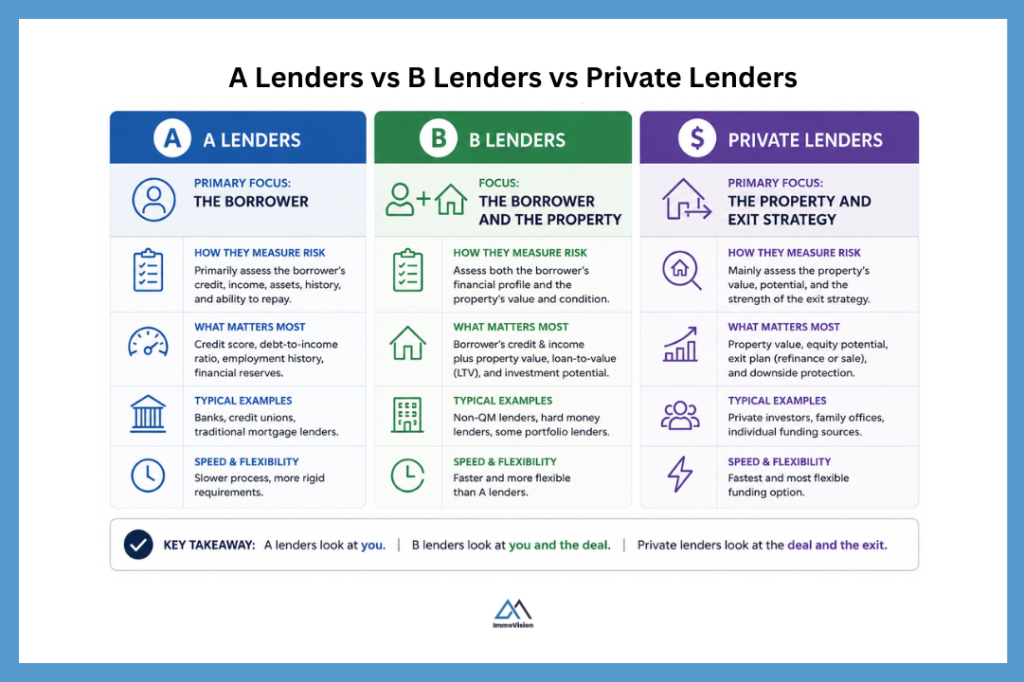

What is the difference between A lenders, B lenders and private lenders

The main difference between A lenders, B lenders, and private lenders is how they measure risk. A lenders primarily assess the borrower. B lenders assess the borrower and the property together. Private lenders mainly assess the property and exit strategy. Let’s take a closer look at how each work:

How A lenders work

A lenders typically include chartered banks (also called Schedule I banks), credit unions, and other federally or provincially regulated financial institutions. Chartered banks are regulated under the Bank Act and overseen by the Office of the Superintendent of Financial Institutions (OSFI). Meanwhile credit unions, are regulated at the provincial level rather than by OSFI. In Quebec, this is done by the AMF.

A lenders attempt to asses how likely it is for the borrower to repay their debts. To make this assessment, A lender will rely heavily on metrics such as credit score, debt service ratios, employment stability, and verified net income. They look at the borrower largely in isolation and, although they will appraise homes before issuing the mortgage to ensure they are not over-lending against its value, they are primarily trying to determine whether the borrower can reliably make the mortgage payments over time.

How B lenders work

B lenders include regulated non-prime lenders, trust companies, and non-prime monoline lenders. These institutions operate under different regulatory frameworks. Trust companies and federally regulated non-prime lenders are generally overseen by the Office of the Superintendent of Financial Institutions (OSFI), while some monoline lenders may operate under provincial regulation or through funding partnerships with federally regulated institutions.

B lenders use decision-making criteria similar to A lenders; however, they are generally more flexible and consider not only the borrower, but also the property itself. This means they may be more willing to approve borrowers with weaker credit, non-traditional income, or higher debt ratios when the property is strong, the down payment is larger, or there is significant equity in the deal.

How private lenders work

Private lenders are typically subject to less prudential regulation than banks and many institutional lenders, and therefore their focus is almost exclusively on the property value and the downpayment made by the borrower. The lenders simply wants to know that they will be able to get their money back if the borrower defaults. This means that they are happy to accept just about anyone provided that there is enough equity in the home to cover their risk.

To see how this works, consider the following example.

Let’s say that you have $250,000 for a downpayment on a $500,000 home. A private lender may agree to lend you the remaining $250,000 because the property itself provides a large safety cushion. In this case, let’s imagine the lender charges 9% interest plus a 2% lender fee. That would equal roughly $1,875 per month in interest and a $5,000 upfront fee.

Now assume that after 8 months you default on the mortgage. By that point, the lender has already collected about $15,000 in interest plus the $5,000 lender fee. If the lender forecloses on the property and forces a sale, they may choose to sell it quickly at 20% below market value. Even then, the home would still sell for about $400,000. From those proceeds, the lender could recover the $250,000 mortgage balance along with their legal and selling costs.

ℹ️ Note

Private mortgages are almost never a long term solution. They tend to be for individuals who have found their dream home and have a plan to refinance with an A lender or a B lender within 12 months as they expect their income and credit to improve.

What are the different types of B lenders in Quebec?

There are several different types of B lender that compete to lend money to subprime and near-prime borrowers. These include:

Within each category, each specific B lender has its own mortgage rates, qualification criteria, and lending approach. Some offer cheaper financing, but have more strict qualification criteria. Others offer more flexibility and faster financing, but at higher rates of interest. Let’s take a closer look!

❗ Important

Although B lenders often advertise flexible qualification options and easier approvals, their mortgage rates are typically higher than A lenders, but lower than private lenders. However, this does not mean that B lender products are inferior to A lender products, in fact we quite often see the opposite here.

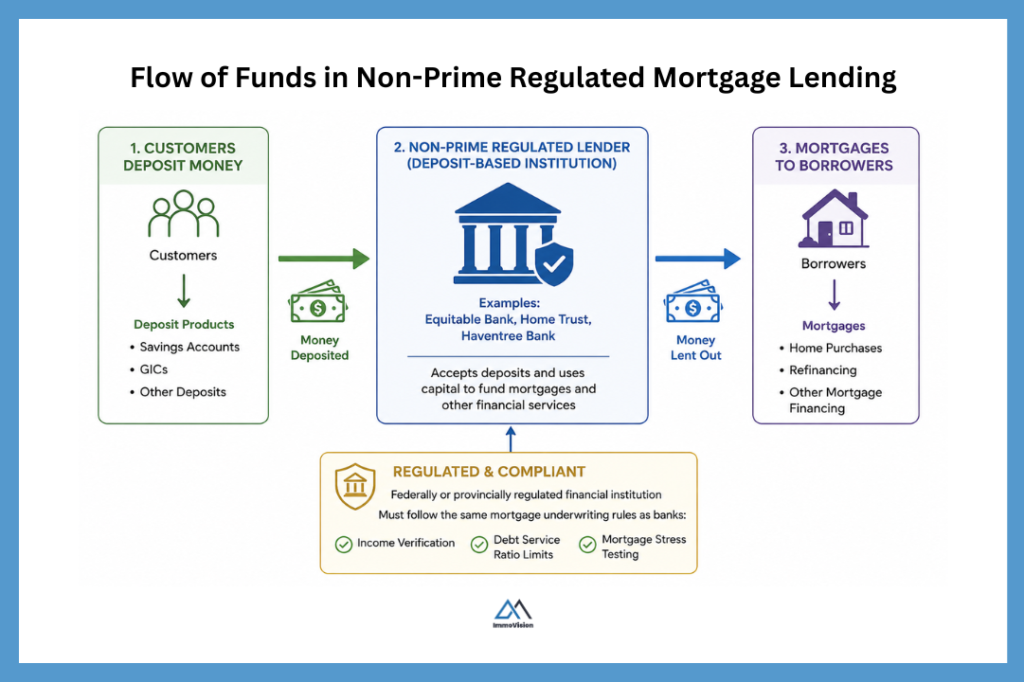

Non-prime regulated lenders

Non-prime regulated lenders are institutions that issue mortgages to borrowers who do not meet the requirements of traditional banks. Examples include: Equitable Bank, Home Trust, and Haventree Bank.

Although non-prime regulated lenders generally use more flexible internal underwriting standards than major banks, they are still regulated financial institutions. As such, they must comply with the same broad mortgage underwriting requirements that apply to traditional banks. The Bank Act sets out these rules which include income verification, debt service ratio limits, and mortgage stress testing standards.

Like traditional banks, these lenders operate using a deposit-based business model. They accept deposits from customers through products such as savings accounts and GICs (Guaranteed Investment Certificates), then use this capital to fund mortgages and other financial services.

Trust companies

Historically, trust companies were businesses that exclusively handled trusts, estates, inheritances, and fiduciary asset management for families and wealthy individuals. However, over time many evolved into deposit-taking financial institutions that accept deposits in the form of GICs and then used these deposits to give out mortgages. Examples include, Home Trust Company, Equitable Bank, and Fairstone Bank.

Trust companies operate a business model similar to non-prime regulated lenders and are also subject to strict mortgage lending regulations. These requirements are established through federal legislation such as the Trust and Loan Companies Act and, in some cases, the Bank Act, with oversight provided by OSFI.

Subprime monoline lenders

Monoline lenders are financial institutions that specialize primarily or exclusively in mortgage lending. This means that unlike traditional banks, which offer a range of services such as chequing accounts, credit cards, and so on, monoline lenders focus mainly on residential mortgages. Because of this specialization, monoline lenders sometimes have some of the best and most flexible mortgage products on the market.

However, it is important to realize that “monoline lenders” are a broad category that includes both prime monoline lenders (which offer rates similar or better to A lenders) and alternative or subprime monoline lenders (which tend to offer higher rates). This means that the rates, qualification requirements, and flexibility offered can vary significantly depending on which type of monoline lender you speak with.

Monoline lenders operate a different business model from deposit-taking banks. The way they work is, the monoline lender will first raise funding through capital markets and securitization programs rather than traditional deposits. They use this funding to issue mortgages. Once they have issued a large portfolio of mortgages, they bundle those mortgages into pools and sell them to investors as securities. This frees up capital, allowing them to recycle funds and originate more mortgages.

Some monoline lenders fall under federal regulation and must comply with the Bank Act and OSFI oversight, while others are operate under provincial frameworks or alternative lending structures.

Current B lender mortgage rates in Quebec

Most B lenders do not advertize their mortgage rates online. This is because B lenders often have a tailored approach to mortgage lending. To compare B lender mortgage rates, you will need to work with a mortgage broker who can access multiple lenders and negotiate on your behalf.

The table below shows a list of B lender mortgage rates in Quebec that we were actually able to find online and compares them to A lender rates.

This is not the a comprehensive list of all available B lender rates or B lender mortgage products however, it demonstrates that A lender rates tend to be lower than B lender rates. This means that your monthly mortgage payments will normally be higher if you use a B lender.

| Type | Equitable Bank | Home Trust | Haventree Bank | Laurentian Bank | Best A Lender Rate (Market) |

|---|---|---|---|---|---|

| 5-Year Fixed Rate | 4.09% | 6.49% – 8.49% | 6.99% – 8.99% | 6.25% – 7.50% | 3.69% – 4.50% |

List of B lenders in Quebec?

Who are B lenders best for?

If you do not qualify for a mortgage from an A lender, but you still want to get a mortgage, you will need to consider using a B lender. Typically we see the following types of borrowers work with B lenders:

- Savvy borrowers: Just because an A lender approves your mortgage does not mean you are getting the best deal. In some cases, B lenders offer more competitive or flexible mortgage products than traditional banks.

- New arrivals to Canada: If you are new to Canada, you will likely have no Canadian credit history. This can mean that you have a stockpile of cash, but A lenders will either ask for a very high downpayment (say 35%+) or refuse to lend you money.

- People with bad credit: A low credit score, or badly blemished credit report can quickly disqualify you from getting a mortgage anywhere other than a B lender.

- The self employed: Many self-employed borrowers report lower net taxable income due to business expenses, which disqualify you based on the the debt service ratio (TDS and GDS) criteria with A lenders. Conversely, B lenders will consider gross income, cash flow, or overall business strength when assessing an application.

- Real estate investors: Some B lenders offer mortgage products specifically designed to finance investment property purchases.

Which type of B lender is best for you?

In each case, the best type of B lender for you will depend on the reason why you did not qualify at the traditional bank in the first place. Generally speaking:

- Monoline lenders are often best for self-employed borrowers or applicants with complex income structures. This is because they typically use more flexible income assessment methods and may place greater emphasis on gross income or overall cash flow rather than strictly relying on net taxable income.

- Non-prime regulated lenders tend to work well for borrowers who fall somewhere in between, such as applicants with minor credit issues, higher debt ratios, or non-traditional financial profiles who still want access to more standardized mortgage products and regulated lending environments.

- Trust companies are often best for borrowers with credit challenges. This is because they tend to apply more flexible credit score requirements and take a broader view of the borrower’s overall financial situation.

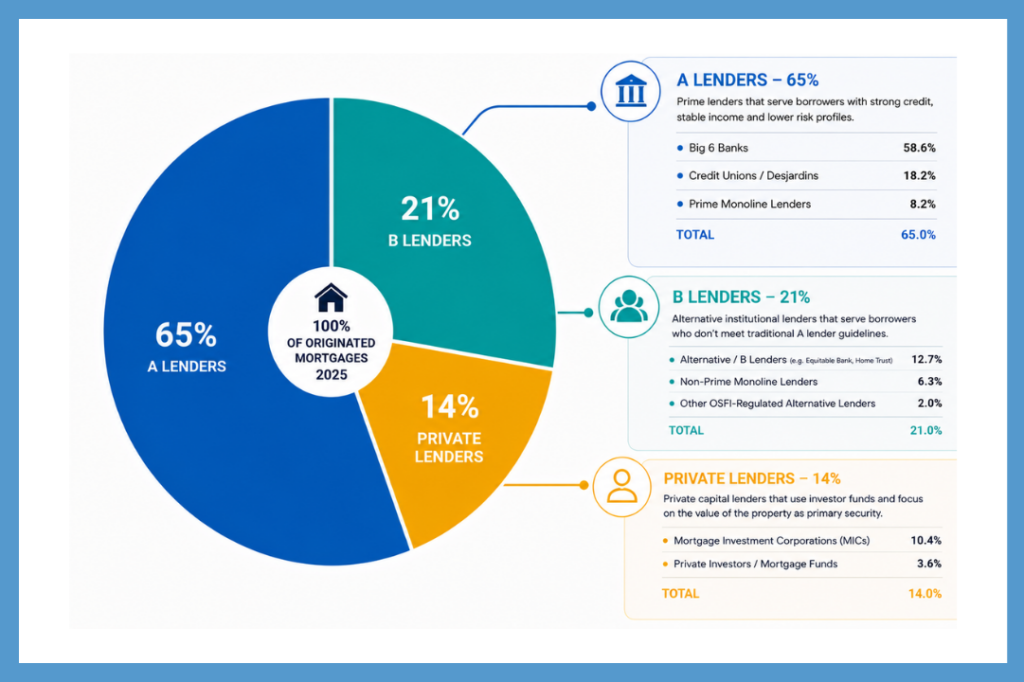

How popular are B lenders in Canada?

The Canadian Mortgage Housing Association (CMHC) reports there are three types of organizations who lend money: A lenders, B lenders, and private lenders.

According to the CMHC Residential Mortgage Industry Report 2025, the A lenders accounted for approximately 65% of newly originated mortgages in Q1 2025. B lenders accounted for 21%, while private lenders make up approximately 14% of the market. The graphic below shows how this breaks down.

Is it safe to use a B lender in Quebec?

Many borrower’s tend to favour working with A lenders because they feel safer working with a big brand name lender, who has physical locations. However, even when you work with a major bank such as Royal Bank of Canada, Bank of Montreal, or TD Bank, the mortgage contract still carries strict legal obligations. As such, if you fail to make payments or do not comply with the terms of the mortgage agreement, the lender can still apply interest penalties, report defaults to credit bureaus, and ultimately initiate foreclosure proceedings.

For this reason, B lenders only really represent more risk if you do not fully understand the terms of the agreement. As such, if you are considering working with a B lender, you should carefully review the mortgage contract, including the interest rate, fees, renewal terms, and any prepayment penalties, before signing. You should also ensure you understand how the lender calculates affordability and what conditions could affect your payments over time.

In most cases, working with a mortgage broker can help you compare options and clearly understand the total cost and structure of the mortgage before making a commitment.

Frequently asked questions

Final thoughts on B lender mortgages

B lenders are mortgage lenders who provide financing to borrowers that may not qualify with traditional A lenders. They compete for borrowers in higher-risk or more complex lending categories, such as self-employed individuals, borrowers with bad credit, or those with higher debt ratios.

Some B lenders also compete with A lenders by offering more flexible underwriting, faster approvals, or specialized mortgage products that better suit certain borrowers.

B lenders tend not to publish their products online, and so you must work with a mortgage broker to understand the products, rates and terms and fees and conditions. In all cases, whether you work with an A lender, B lender, or private lender, it is very important to read your contracts carefully.

Free, No Obligation Mortgage Consultation

Book a call with a licensed mortgage broker, to get a game plan for your specific case.