Are you struggling to get a mortgage at the bank? Alternative mortgage lenders could be the solution.

In this article we look at what is alternative lending, how it works, what are the pros and cons, the different types of alternative lenders and who are the top players in the Canadian market for alternative lending.

Let’s start by understanding what actually is alternative lending, and how has it changed in recent years.

What is alternative lending?

Alternative lending refers to financing solutions offered to borrowers who may not qualify for loans from traditional banks or credit unions. While the term is not a formal legal category, it is commonly used within the financial industry to describe lending products designed for borrowers viewed as higher risk. For example, a person who is declined for a mortgage, car loan, or line of credit at a bank may still be approved by an alternative lender.

Alternative lenders are also sometimes referred to as B lenders, subprime lenders, or private lenders.

Quick note on alternative lenders vs A lenders

In recent years, many alternative lenders have expanded their product offerings to include mortgages aimed at lower-risk borrowers who could also qualify with a traditional bank. As a result, the distinction between traditional lenders and alternative lenders has become less clear-cut. For this reason, it is often more useful to think in terms of mortgage products and risk tiers rather than lender labels alone.

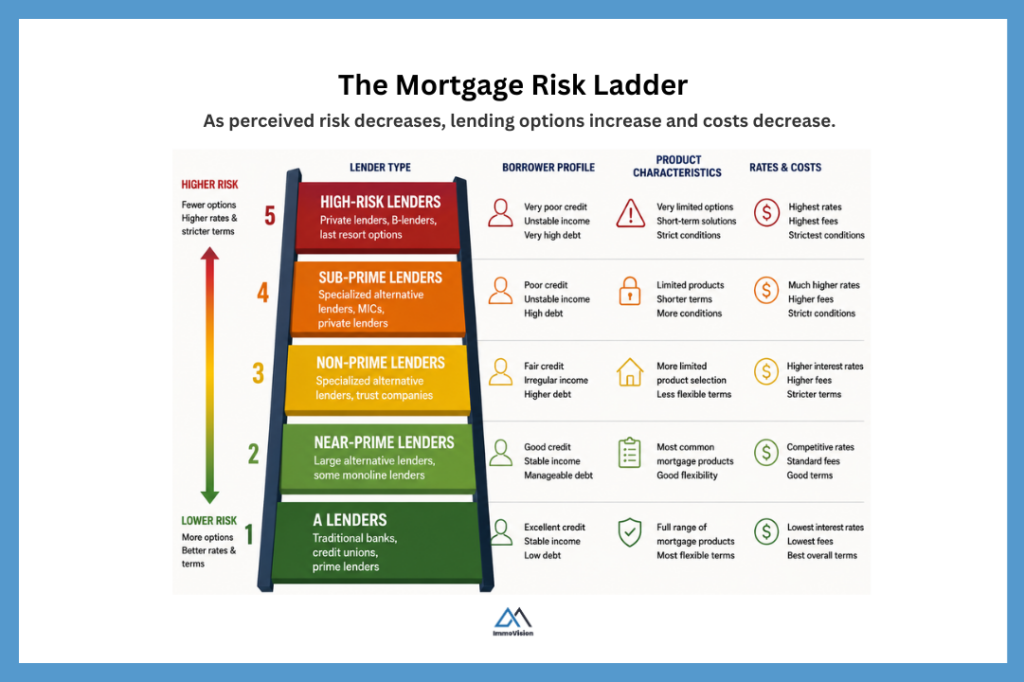

Borrowers with strong credit, stable income, and lower debt levels generally qualify for the widest selection of mortgage products and the most competitive rates. As a borrower’s perceived level of risk increases, fewer lenders may be willing to approve the mortgage, and those that do often charge higher interest rates or impose stricter terms.

Think of it like a “risk ladder.” At the bottom are traditional A lenders, which generally offer the best rates and terms to lower-risk borrowers. As perceived borrower risk increases, financing may still be available through alternative lenders, but usually with higher interest rates, additional fees, and stricter lending conditions.

How do lenders measure borrower risk?

In Canada, the credit bureaus are responsible for measuring borrower risk. There are two main credit bureaus in Canada: Equifax Canada and TransUnion. These companies collect credit information from Canadian citizens and use it to create a credit report and credit score.

Lenders use this report to assess how likely it is that a borrower will repay their debts, based on their past behavior. If the borrower is someone who always pays their debts on time, and does not have too much debt, then they will have a good credit report and a high credit score. However, if the borrower has always lives in debt, is regularly late or has defaulted on certain payments, then they will have a credit report and a low credit score.

Note: For more information on how to get a mortage with a bad credit score, read How To Get A Mortgage With Bad Credit in Quebec.

Pros & cons of alternative mortgage lending (at a glance)

Each alternative lender offers a different set of mortgage products designed for a range of borrower types. The list of available products depends on your mortgage risk profile and how quickly you need financing. Generally speaking, the faster you need the mortgage and the higher your perceived risk, the more you will pay.

That being said, as a general category, alternative mortgage lending comes with some pros and cons that it is good to be aware of.

ℹ️ Note

Alternative lending often works best as a short term, or what is known as a bridge solution, rather than a permanent financing strategy.

To work out a good strategy for how to use alternative lenders, it is a good idea to speak with a professional Mortgage Broker.

You can compare and find mortgage brokers using the Immovision Agent Finder tool.

Pros of alternative mortgage lending

Below are the pros of alternative mortgages.

Easier approval

The primary benefit of alternative lenders is that they have less strict lending criteria. While traditional banks and credit unions must operate within tight underwriting standards, capital requirements, and federally regulated mortgage stress test rules, alternative lenders are often able to work with borrowers who fall outside these guidelines.

All federally regulated lenders must follow guidelines established by the Office of the Superintendent of Financial Institutions (OSFI), including the B-20 mortgage underwriting guideline, which sets expectations around income verification, debt service ratios, and stress testing. In addition, high-ratio insured mortgages must comply with eligibility requirements set by Canada Mortgage and Housing Corporation (CMHC), including maximum amortization periods, minimum credit scores, and debt service limits.

Alternative lenders are generally able to apply more flexible internal policies, allowing them to approve borrowers with higher debt service ratios (GDS / TDS), non-traditional income, recent credit issues, past bankruptcies or consumer proposals, or complex self-employed income situations.

More flexible underwriting

In addition to having more flexible lending guidelines, alternative lenders are often more willing to take a broader view of a borrower’s financial situation, including how income is earned and documented.

For example, with self-employed borrowers, some alternative lenders can consider gross stated income rather than relying strictly on net taxable income. Rental income may also be treated more flexibly through rental offset or add-back programs, where a portion of the rental income is used to offset the associated mortgage payment. This can help reduce the borrower’s overall debt service ratios and improve qualification amounts.

In some cases, alternative lenders may also allow outstanding debts such as tax arrears, consumer proposal balances, or higher-interest obligations, to be consolidated into the new mortgage. By restructuring these payments into a longer amortized loan, the borrower’s monthly obligations may decrease, helping improve cash flow and qualification.

This flexibility can make it easier for self-employed borrowers, commissioned employees, seasonal workers, or applicants with non-traditional income sources that do not fit neatly within standard bank underwriting models to obtain financing.

Faster decisions

Traditional banks and credit unions usually operate within large institutional structures. Mortgage applications may need to pass through multiple departments, automated risk systems, compliance reviews, and federally regulated underwriting standards before funding is approved. This can slow the process down — especially for borrowers with non-standard income, credit challenges, or unusual properties.

By contrast, alternative and private lenders tend to have fewer approval layers and simpler risk assessments.

Useful as “stepping stone” financing

Whilst alternative lending can be a valuable solution for borrowers who do not qualify for traditional bank financing, it can also be more expensive due to higher interest rates and lender fees. As a result, many borrowers use alternative mortgages as “stepping stone” financing — a temporary solution that gives them time to rebuild credit, stabilize income, reduce debts, or improve their financial profile before refinancing with a traditional lender later on.

Lower cost mortgages

In recent years, some alternative lenders have created mortgage products for borrowers that qualify to work with the traditional banks and credit unions. This is especially the case amongst the monoline lenders. These are alternative lenders (such as MCAP, First National, and RMG Mortgages) who specialize in mortgages, often competing directly with the major banks for highly qualified borrowers by offering lower rates and mortgage-focused products.

Of course, these products are not for all borrowers, but it does highlight how the “alternative lender” category is not a single uniform segment. Instead, it spans a tiered risk spectrum from near-prime and prime monoline lenders who compete directly with banks, through to B lenders and private lenders that serve higher-risk or non-traditional borrowers.

Downsides of alternative mortgage lender

Below are the downsides of alternative mortgage lenders.

Higher interest rates

In many cases, borrowers who are unable to qualify with a traditional lender can still obtain financing through an alternative lender, although the interest rate is usually higher due to the added flexibility and risk involved.

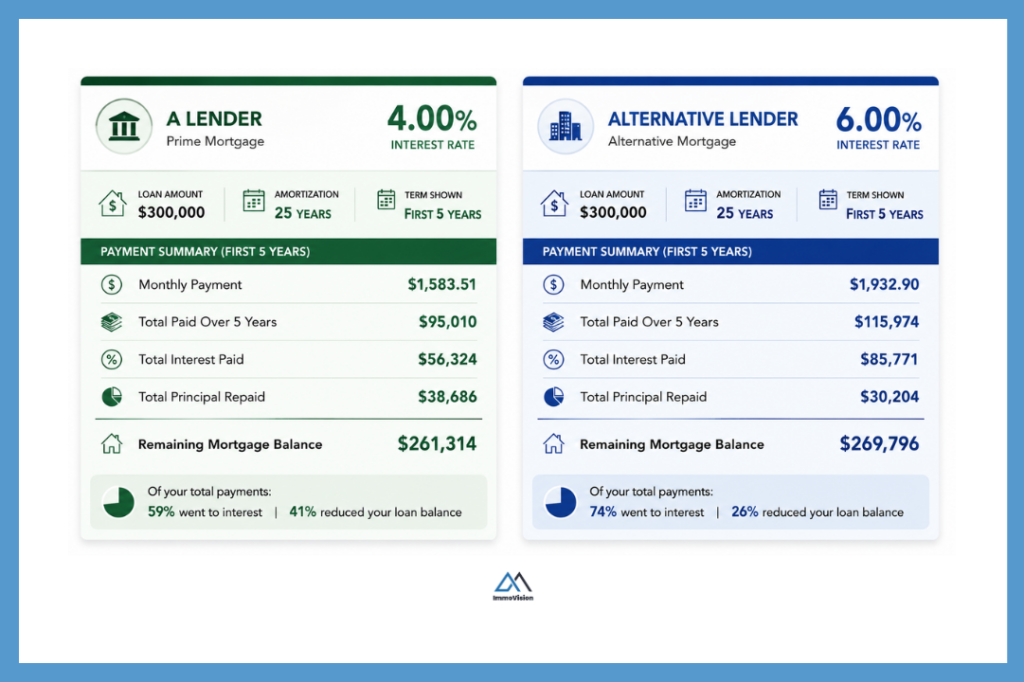

To see how this compares, let’s take two equivalent 25 year mortgages. The first one is from an A lender, offered at 4% and the second is from a alternative lender offered at 6%, both are for $300,000. The graphic below compares these two mortgages.

Notice that although the monthly payments are only $385 different, with the mortgage from the alternative lender, you will pay more than $29,000 extra over the 5 year period. This is why many borrowers use alternative lending as a temporary stepping stone and aim to refinance into an A lender mortgage once their credit improves, income stabilizes, or they qualify for better rates and terms.

A good mortgage broker will be able to help you create a plan to transition from an alternative lender to an A lender as your financial profile improves. This can save you tens of thousands of dollars in interest over time.

Higher fees

Alternative lenders may also charge additional fees for arranging and underwriting the mortgage. These fees are typically expressed as a percentage of the mortgage amount. Typically these fees will range from 0.5% to 2% with alternative lenders, and sometimes higher with private lenders.

In many cases, these fees can be added to the mortgage balance rather than paid upfront, although this depends on the lender and the borrower’s available equity. If the fees are added to the mortgage, interest is usually charged on those amounts as well. For example, if you are charged a 0.5% lender fee on a $300,000 mortgage, the fee would be $1,500, which may be added to your mortgage balance and repaid over time as part of your regular mortgage payments.

The table below shows how the fees charged can impact your total mortgage amount.

| Mortgage Amount | 0.5% Fee | 1% Fee | 1.5% Fee | 2% Fee |

|---|---|---|---|---|

| $200,000 | $1,000 | $2,000 | $3,000 | $4,000 |

| $250,000 | $1,250 | $2,500 | $3,750 | $5,000 |

| $300,000 | $1,500 | $3,000 | $4,500 | $6,000 |

| $350,000 | $1,750 | $3,500 | $5,250 | $7,000 |

| $400,000 | $2,000 | $4,000 | $6,000 | $8,000 |

ℹ️ A Note on Mortgage Broker Fees

Mortgage brokers are typically compensated by the lender through a commission when the mortgage funds. With traditional “A lender” mortgages, borrowers usually do not pay the broker directly. However, with alternative or private lending, a broker fee may also apply. This will typically be around 0.5% to 1.5% of the mortgage amount, depending on the complexity of the file.

More equity required

Alternative lenders typically require at least a 20% downpayment for a home or, put another way, a Loan-To-Value ratio of 80%. The reason that alternative lenders do this is to manage their downside risk.

When you apply for a mortgage from an alternative lender, they assess you and the property. This is because, they want to know (A) what is the likelihood of the you repaying the loan through interest payments and (B) to assess what happens if you default. In scenario where you default on the loan, the lender will need to sell your home to recover their money.

In Quebec, the way this works is that the property is typically sold and the proceeds are used to repay the mortgage balance, interest arrears, and legal costs. Any remaining equity is returned to the borrower. However, if property values decline or costs are high, the borrower may receive significantly less equity than expected, which can result in a substantial financial loss.

Shorter terms

Many alternative mortgages have shorter terms of 1 to 3 years.

For example, if you borrow $300,000 with a 25-year amortization and a 1-year term, you will need to qualify for refinancing or secure another lender within 1 year. If you are unable to refinance or repay the mortgage at the end of the term, the lender may demand full repayment of the outstanding balance. In some cases, this could ultimately result in the lender taking legal action or forcing the sale of the property to recover the funds owed.

Most alternative lenders will often offer a renewal or refinancing option at the end of the term, provided the borrower still meets their criteria. However, if the borrower is unable to transition back to a traditional lender, this can create a cycle of renewals at higher rates and fees, effectively extending reliance on alternative financing.

Risk of dependency cycle

At renewal, many borrowers assume they will simply be able to switch back to a traditional lender. However, A-lenders still review the application against strict qualification rules. If credit score, income stability, or debt levels have not improved enough, the application may still be declined.

In some cases, the higher cost of alternative financing can actually slow the progress needed to qualify for an A-lender mortgage. Larger monthly payments leave less room in the budget to pay down other debts or build savings. In some cases, this can also lead to higher reliance on credit cards or lines of credit to cover everyday expenses, which increases your credit utilization ratio. Since credit utilization is a key factor in credit scoring, this can cause your credit score to drop.

And, while home equity is helpful, it usually cannot fully make up for weaker credit or unstable income in the way many borrowers expect. A lenders will still focus more on your credit situation than on the amount of equity that you own in the property.

Comparing Alternative and Conventional Mortgages

The table below shows the key differences between alternative and conventional mortgages.

| Category | A-Lenders (Conventional Mortgages) | B-Lenders (Alternative Mortgages) |

|---|---|---|

| Income Verification | Require ~2 years of stable income (T4s, NOAs, full documentation) | Often accept ~6–12 months of bank statements or flexible income proof (especially self-employed) |

| Credit Requirements | Strong credit required; recent missed payments, collections, or restructuring usually disqualify | More flexible with credit issues (missed payments, past credit events, lower scores may still be acceptable) |

| Debt Ratios | Strict GDS/TDS ratio limits based on standard underwriting rules | More flexible, assessed case-by-case based on overall risk profile |

| Down Payment / Equity | Can allow lower down payments (including insured mortgages in some cases) | Typically requires higher equity (often ~20%+) to offset risk |

| Underwriting Focus | Historical stability: credit history, income consistency, and predictability | Current situation: equity, property value, and near-term repayment ability |

| Approval Criteria | Rules-based and rigid | Flexible and discretionary |

Different types of alternative mortgages

There are three main types of alternative mortgage lender are: trust companies, monoline lenders, and Mortgage Investment Corporations (MICs). Each of these offer different types of mortgage product for you to choose from. Some A lenders, also offer types of alternative mortgages. For example, HomeEquity Bank (which is a Schedule 1 bank) offers something called a reverse mortgage.

In this section, we cover what are the different types of alternative mortgage that are currently available in Canada.

Alternative residential mortgages

All alternative lenders offer alternative residential mortgages.

Although their are different types of residential mortgage, they all work roughly the same way. You borrow money today, and then you pay it back in monthly instalments. Each instalment is made up of principle and interest payments.

These residential mortgages work exactly the same way as those issued by A lenders however, they differ in the terms that you can expect and the types of borrowers who use them. The table below compares typical residential mortgages from A lenders vs alternative lenders.

| Feature | A-Lender Residential Mortgage | Alternative Residential Mortgage |

|---|---|---|

| Interest Rates | Lower | Higher due to increased lending risk and underwriting flexibility |

| Down Payment / Equity | Can allow lower down payments to as low as 5% on properties worth less than $500,000 (with CMHC loan insurance) | Usually requires more equity (often 20%+) |

| Mortgage Terms | Commonly 3–5 years | Often 1–3 years |

| Fees | Usually no lender fees | Typically include lender fees of ~0.5%–2% of the mortgage amount, plus possible broker fees |

| Early repayment fees | Often substantial. Fixed-rate mortgages may charge the greater of 3 months’ interest or an Interest Rate Differential (IRD), which can amount to thousands of dollars | Usually simpler and more predictable. Many alternative lenders charge approximately 3 months’ interest, though terms vary by lender |

| Common Use Case | Long-term financing | Temporary or transitional financing |

Reverse mortgages

A reverse mortgage is a type of loan available to Canadian homeowners aged 55 and older that allows them to borrow against the equity in their home without needing to make regular monthly mortgage payments. Instead, the loan balance grows over time through accumulating interest and is typically repaid when the homeowner sells the property, moves out permanently, or passes away.

Note: For more information on how a reverse mortgage works, read how does a reverse mortgage work in Canada.

Construction loans

A construction loan is a type of mortgage that provides financing for the construction of a new home or major renovation project. Unlike a traditional mortgage, where the full amount is advanced upfront, construction loans are typically released in stages as different phases of the project are completed.

In Quebec, construction financing is commonly structured through “draws,” where the lender advances portions of the mortgage after inspections confirm that specific construction milestones such as the foundation, framing, or finishing work have been completed. During construction, borrowers are normally only required to make interest payments on the amounts that have already been advanced.

Bridge loans

Bridge loans are short-term loans designed to help homeowners finance the purchase of a new property while waiting for the sale of their existing home to close. The loan “bridges” the gap between the purchase date of the new property and the receipt of funds from the sale of the current property. Bridge loans are typically short in duration, often a maximum of 90 days, and usually carry higher interest rates than standard mortgage financing because of their temporary nature.

In most cases, bridge financing is secured against the borrower’s existing home and is repaid once the sale closes. In Quebec, the lender’s security is typically registered as a hypothec on the property in the Quebec Land Register. At closing, the notary will repay the bridge loan directly from the sale proceeds before the remaining funds are released to the seller. In this way the lender ensures that the loan is repaid in full from the proceeds of the sale before any remaining funds are released to the seller. This reduces the risk of default during the transition period between properties.

Second mortgages

A second mortgage is a loan secured against a property that already has an existing mortgage registered on it. It sits in “second position,” meaning the first mortgage lender is repaid first if the property is sold or if the borrower defaults, and the second mortgage lender is repaid from any remaining equity. Depending on the terms in the mortgage, the borrower will make two payments each month: one to the first mortgage and one to the second mortgage.

A second mortgage is typically set up as a home equity line of credit (HELOC) or home equity loan. The second mortgage is generally smaller than the first mortgage since it uses the equity already built up in the home. The interest rates on the second mortgage are also higher to compensate for the additional risk of the mortgage being in second position.

Before a second mortgage can be registered, the first mortgage lender usually has to agree to it. This is because the first lender wants to make sure their loan stays in “first position,” meaning they will still be repaid first if the property is ever sold or goes into default.

At the same time, the second mortgage lender also has to formally accept that they are in “second position” behind the first lender. This agreement is called a postponement, and it confirms the repayment order between the two lenders.

When a property has more than one mortgage registered on it, it can also make it more difficult and expensive to switch lenders later. At renewal, new lenders typically require all existing mortgages to be paid out or consolidated, which is why borrowers with multiple loans on the same property may end up refinancing at higher rates or with fewer options available.

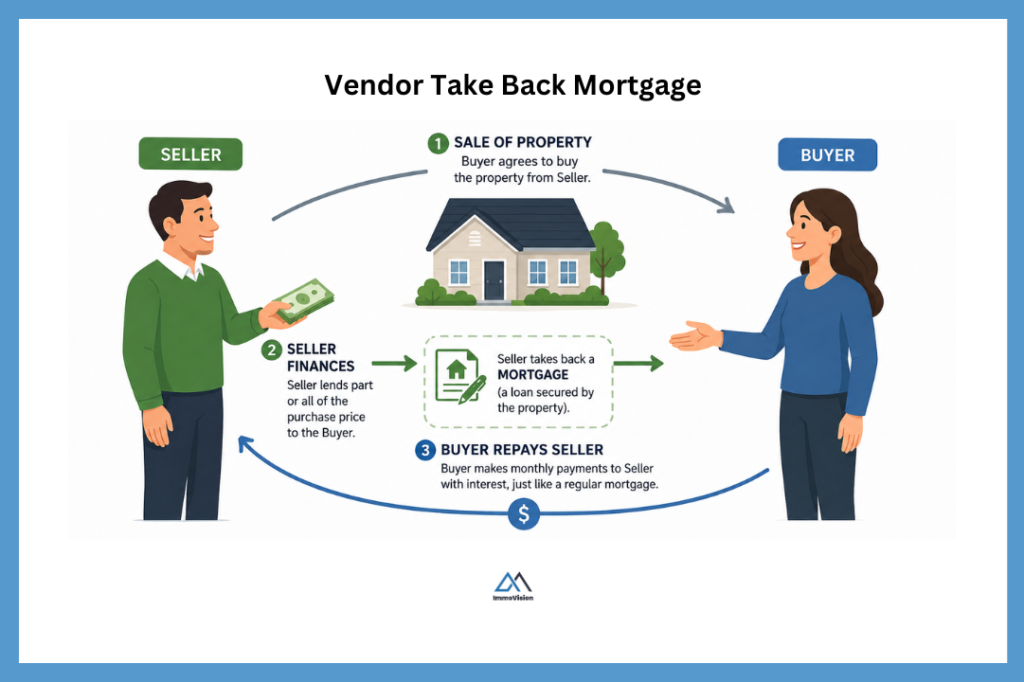

Vendor take-back mortgages

Vendor take-back mortgages, otherwise known as VTB mortgages, are seller-financed loans, where the seller of a property acts as the lender and “takes back” a mortgage from the buyer instead of (or in addition to) a traditional bank loan.

The way it works is that, if a buyer can’t (or doesn’t want to) get full financing from a bank, the seller agrees to lend part or all of the purchase price. The buyer then repays the seller over time with interest, just like a normal mortgage.

VTB mortgages are often used when a seller wants to attract more buyers or sell faster, especially when buyers face financing gaps after signing a promise to purchase.

Who Are The Prime and Alternative Lenders In Canada?

In Canada, Prime Lenders are anyone lends money to prime borrowers — those with good credit report and high credit scores. This includes banks, credit unions, prime monoline lenders and so on. Below is a table of the top prime lenders and their share of the total originated mortgages according to the CMHC Residential Mortgage Industry Report 2025.

| Lender Type | Examples | Share of Originated Mortgages |

|---|---|---|

| Big 6 Banks | RBC, TD, Scotiabank, BMO, CIBC, National Bank | 58.6% |

| Credit Unions | Desjardins, Vancity, Meridian, Coast Capital | 18.2% |

| Other Chartered Banks | Laurentian Bank, Canadian Western Bank | 5.9% |

| Prime-Focused Monoline Lenders | First National, MCAP, RFA, CMLS | Part of non-bank lender share |

| Estimated Majority Prime Market | ~85–90% |

Alternative lenders refers to anyone who will lend money to subprime borrower. This includes alternative federally regulated lenders, the subprime (or alternative) lending division of monoline lenders and Mortgage Investment Entities (otherwise known as MIEs or MICs). Below is a list of the top alternative lenders in Canada.

| Lender Type | Examples | Share of Originated Mortgages |

|---|---|---|

| Alternative Federally Regulated Lenders | Equitable Bank, Home Trust | 3.2% |

| Alternative Divisions of Monoline Lenders | MCAP Alt, RFA Alt, CMLS Alt programs | Included within non-bank lending |

| Mortgage Investment Entities (MIEs) & Private Lenders | MICs, private funds, syndicated lenders | 5.8% |

| Estimated Alternative Market | ~9–14% |

ℹ️ Note

Some lenders operate in both the prime and alternative mortgage markets. For example, MCAP primarily offers prime mortgages, but also has alternative lending products for borrowers who may not qualify under traditional bank guidelines.

Because CMHC groups many of these companies together under “non-bank lenders,” the market share figures cannot always be cleanly separated into strictly prime or strictly alternative categories. As a result, some lenders may appear in both tables.

How to find an alternative mortgage lender in Canada?

To find an alternative mortgage lender in Canada, you should speak with at least one mortgage broker — and ideally several. Mortgage brokers can access multiple lenders, help you obtain and compare offers, and explain the differences between products, rates, fees, and lending conditions.

⚠️ Warning

The real-estate industry often operates through referral relationships. If your realtor recommends a mortgage broker, there is a good chance the realtor will receive a referral fee, marketing benefit, or future business in return.

While this is common industry practice and not necessarily a problem, it clearly create incentives that influence who is recommended to you. For this reason, it is a good idea to speak with multiple mortgage brokers and compare offers independently.

For an independent list of mortgage brokers, along with performance statistics and reviews, you can use the Immovision Mortgage Broker Finder.

Frequently asked questions

To improve your chances of approval, you can:

– Reduce existing debts where possible

– Improve your credit score and payment history

– Increase your down payment or equity position

– Provide complete income and financial documentation

– Work with a mortgage broker who has access to multiple alternative lenders

Because every lender has different guidelines, borrowers who may not qualify with one lender could still be approved by another.

For more information on how to improve your credit score read, Credit Score Explained: What It Is, How It Works & Proven Ways to Improve Yours in Canada.

If you get a mortgage from an alternative lender, it is normally more expensive than getting a mortgage from an A lender. It will also normally come with more restrictive terms. This means that you need to be doubly careful to plan your finances and understand the terms of the mortgage before you accept financing from an alternative lender. It is also advisable to have a strategy in place to switch to a A lender within a couple of years improving your credit score so that you can refinance with an A lender within a short period of time.

For this kind of financial advice, you will either need to speak with a financial advisor or a mortgage broker who will help you to assess your options.

Final thoughts

Alternative lending plays an important role in the Canadian mortgage market. For many borrowers, it provides access to financing when traditional banks are unwilling or unable to approve the mortgage. This can include self-employed borrowers, people rebuilding credit, those with higher debt loads, or borrowers with more complex financial situations.

However, greater flexibility often comes with trade-offs. Higher interest rates, lender fees, shorter terms, and stricter equity requirements can significantly increase the overall cost of borrowing over time.

For many people, the most effective approach is to view alternative lending as a temporary financing strategy rather than a permanent solution. Used carefully, it can provide the time needed to improve credit, reduce debt, stabilize income, or resolve short-term financial challenges before transitioning to lower-cost financing.

The most important question is often not “Can I get approved?” but rather “What is the long-term plan after approval?” Understanding that strategy before signing a mortgage can potentially save thousands of dollars and create more options later.