Millions of Canadians have mortgages with monoline lenders — often without even realizing it.

Despite this, the majority of borrowers still assume monoline lenders are somehow “riskier” than banks. In reality, Canada’s largest monoline lenders have become integral to the country’s mortgage system and compete directly with major banks on rates, products, and underwriting.

In this article, we will will look at:

- What exactly is a monoline lender?

- How popular are monoline lenders in Canada?

- What are the benefits of monoline lenders?

- How do monoline lenders work?

- How are monoline lenders regulated?

- What is the difference between monoline lenders vs banks?

- What are the pros and cons of working with a monoline lender?

- Who are the top monoline lenders in Canada?

- Frequently asked questions

- Final remarks

What is a monoline lender?

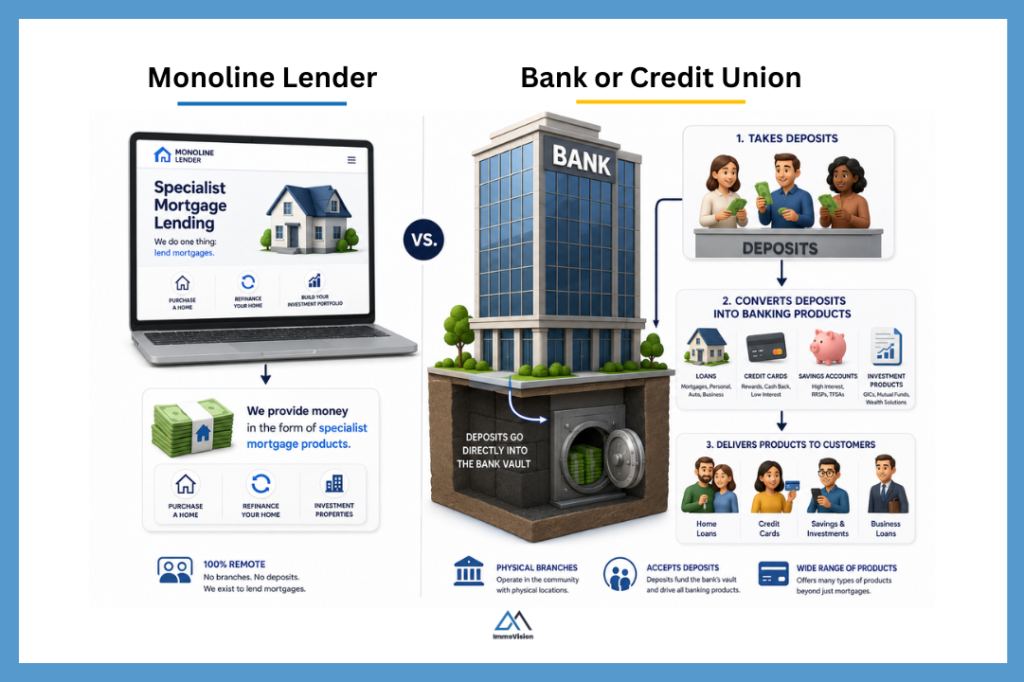

A monoline lender is a financial intermediary that specializes in residential mortgage lending. Put another way, it is a company that focuses almost exclusively on providing mortgages to Canadians.

Unlike traditional banks and credit unions, which accept customer deposits and use those funds to offer a wide range of financial products (including mortgages, credit cards, and personal loans), monoline lenders raise capital through institutional investors and capital markets. They use this money to originate loans.

Monoline lenders also typically operate without a physical branch, instead they rely heavily on mortgage brokers and digital channels to connect with borrowers.

How popular are monoline lenders in Canada?

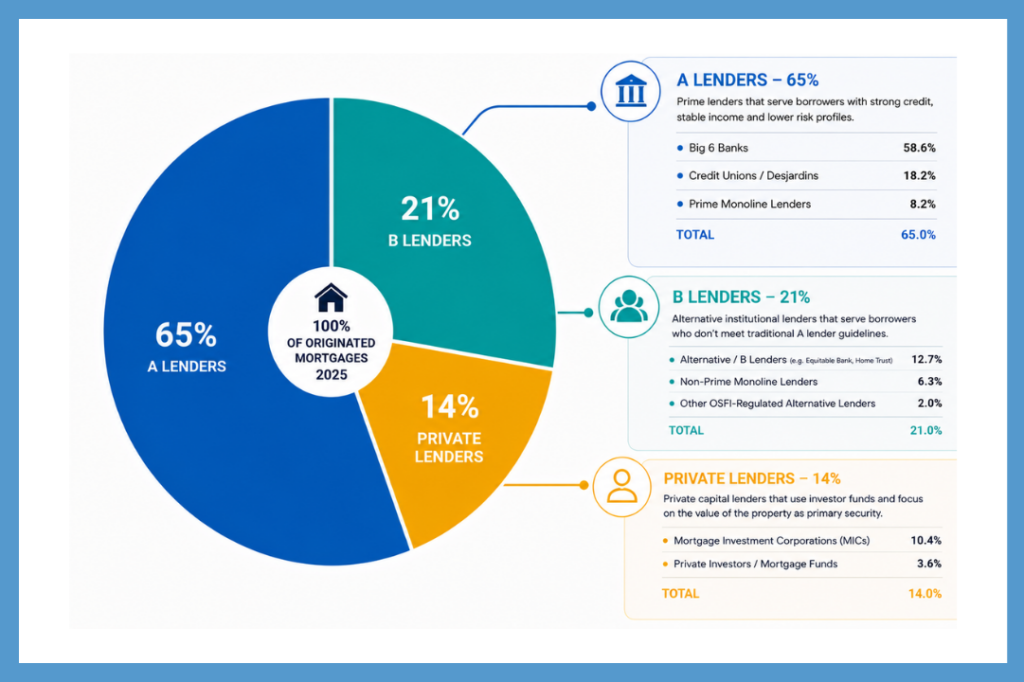

According to the CMHC Residential Mortgage Industry Report 2025, monoline lenders account for 24.9% of Canadian mortgages in 2025. This means that roughly 1.47 million Canadians households have mortgages with a monoline lender. This makes it one of the most popular categories of mortgage lender in Canada.

Note: We include Prime, non-prime (subprime) and Mortgage Investment Corporations (MICs) in out count of monoline lenders. More on this shortly.

What are the benefits of monoline lenders?

Monoline lenders have a number of advantages compared to traditional banks. The main advantages are:

- Flexible lending criteria: Monoline lenders are generally more flexible than traditional banks and credit unions when evaluating mortgage applications. This can help borrowers who may not fit the standard lending criteria used by major banks.

- Lower operating costs: Unlike traditional banks, many monoline lenders do not operate large branch networks. This reduces overhead costs and can allow them to offer competitive mortgage rates and products.

- Mortgage specialization: Monoline lenders focus primarily on mortgages rather than offering a wide range of banking products. Because of this specialization, they often provide highly competitive mortgage rates, features, and terms. Even if a bank approves your mortgage application, a monoline lender may still offer a better mortgage product for your situation.

ℹ️ Note

Monoline lenders primarily work through mortgage brokers. To find the right lender for your situation, it helps to work with a mortgage specialist who has access to a broad network of lenders and knows how to position your application effectively.

Find a broker now using the Immovision Mortgage Broker Finder.

How do monoline lenders work?

There is no single legal structure that defines a monoline lender in Canada. In practice, monoline lenders can use several different funding and operating models to originate mortgages.

The most common models include:

Let’s take a look at each of these now.

Securitization model

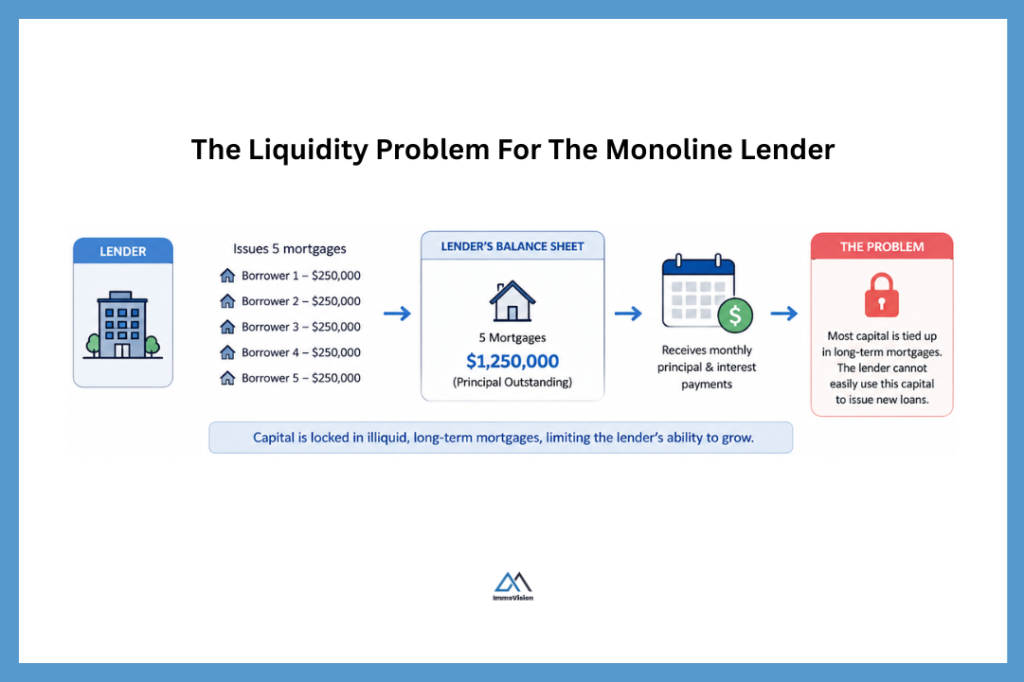

The most common way that monoline lenders work is through a securitization model. In this setup, the monoline lender will first raise an initial pool of money from the capital markets and/or private institutional investors. They then lend this money out to borrowers for their mortgages. Once they have lent out most or all of their capital, they “securitize” the mortgages and sell them to investors in order to free up more capital and continue issuing new loans.

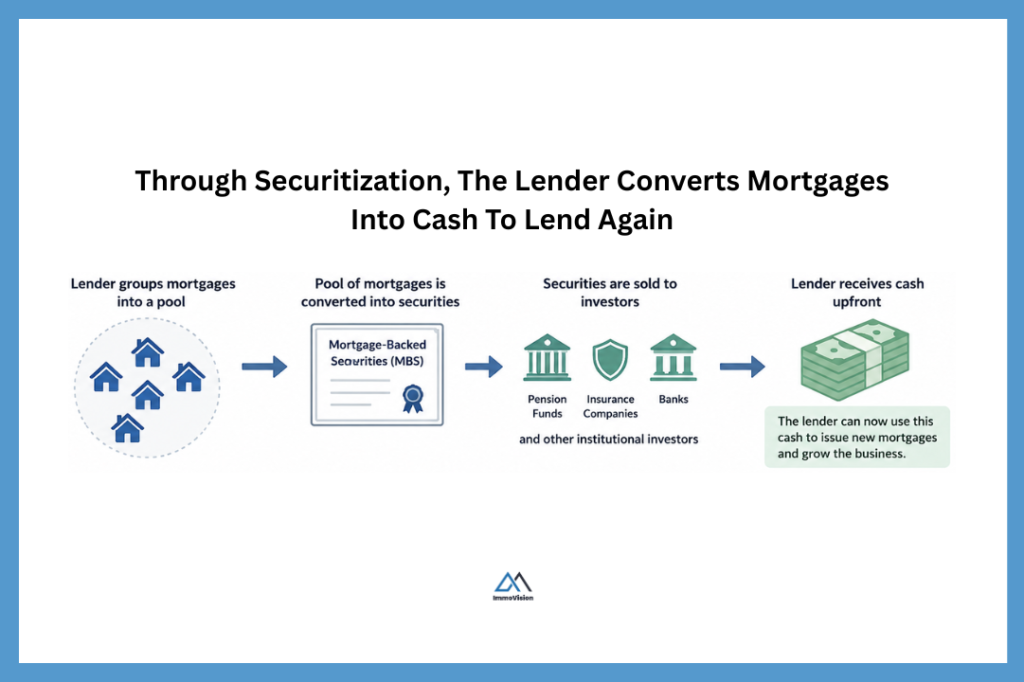

What is securitization?

Securitization is when the lender groups illiquid assets into securities that they can sell to institutional buyers.

For example, let’s say that a monoline lender issues five mortgages, with 20 year terms to five different homeowners in Quebec. Let’s also say that each mortgage is for $250,000 and they charge 4% interest on the mortgage.

At this point, the monoline lender has issued $1.25 million of mortgage loans. The borrowers will make monthly payments to the lender (interest + principal) of roughly $7,500 across all five loans. This means that it would take roughly 14 years for the lender to recover its original $1.25 million cash outlay through cumulative mortgage payments.

This creates a liquidity problem for the lender because, their money is locked into mortgages that will be repaid gradually over many years.

A banker called Lewis Ranieri developed securitization as a way to solve this problem. Lewis realized that instead of waiting years for borrowers to repay their mortgages, the lender can group the mortgages together and convert the expected future cash flows into tradeable securities. He then sold these securities to institutional investors like pension funds, insurance companies, or banks, that have excess capital and are seeking relatively predictable investment returns. This process of converting individual mortgages into tradable securities is called “securitization”.

The large institutional investors receive income generated by the underlying mortgage payments, while the monoline lender receives cash upfront from selling the securities. The lender can then use this cash to issue new mortgages and continue growing its business.

ℹ️ Note

In Canada, many monoline lenders securitize insured mortgages through programs connected to the CMHC, such as National Housing Act Mortgage-Backed Securities (NHA MBS).

Mortgage Investment Corporation

A Mortgage Investment Corporation (or MIC) is a Canadian business structure that allows groups of high net worth individuals to lend money for mortgages.

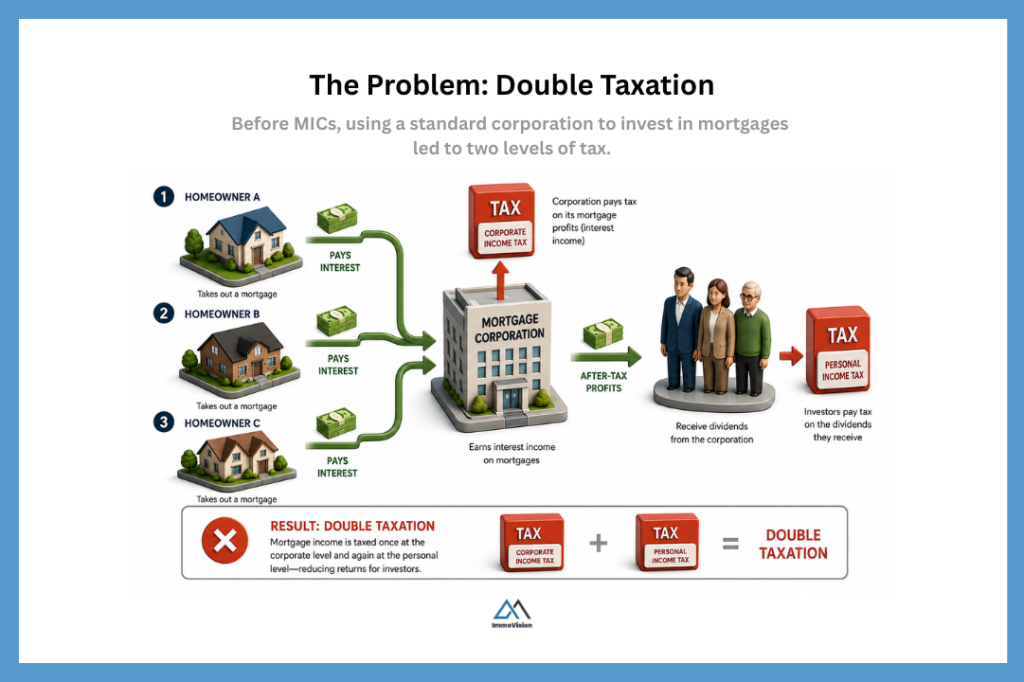

MICs became popular after the Income Tax Act created the structure in 1973. Before this, it was difficult for private investors to participate directly in mortgage lending because it required significant capital, underwriting expertise, and administrative infrastructure. While investors could theoretically pool money through a standard corporation, this created double taxation: first corporate tax on mortgage profits (interest paid on the mortgages), then personal tax on investor dividends.

MICs were designed to solve this problem by allowing mortgage income to flow through directly to shareholders, avoiding taxation at the corporate level.

Most MICs lend to borrowers who fall outside traditional bank standards, such as self-employed borrowers, real estate investors, or borrowers with weaker credit. As a result, MICs generally operate in the highest-risk segment of the mortgage market.

They manage this risk by charging higher interest rates, requiring lower loan-to-value (LTV) ratios, and keeping mortgage terms short — often between 6 months and 2 years. The short terms create faster turnover, which reduces the need for securitization because capital is returned relatively quickly.

White-label origination platform

A white-label mortgage origination platform is a company that provides the the backend infrastructure needed for another business to offer mortgages under its own brand without building the lending operation itself.

For example, let’s say a group of mortgage brokers already has a steady flow of borrowers. In this case, they could use a white-label origination platform to handle things like underwriting, compliance, processing, and funding relationships, while the brokers focus mainly on finding clients and structuring deals.

There are many variations of this model, where the customer-facing brand does more or less of the actual mortgage origination and operational work. In some cases, the brand is mostly a marketing and distribution layer, and in others it behaves like a full lender while only outsourcing the underlying infrastructure.

How are monoline lenders regulated?

Canadian regulators normally break financial regulation into two broad groups:

- Prudential regulation

- Market conduct / consumer protection regulation

Prudential regulation focuses on the safety and soundness of financial institutions. Its goal is to ensure that banks and other deposit-taking institutions remain financially stable and capable of meeting their obligations to depositors, creditors, and the broader financial system. This includes rules around capital requirements, liquidity requirements, stress testing, and so on. At the federal level, prudential regulation of banks is primarily governed under the Office of the Superintendent of Financial Institutions (“OSFI”) and the Bank Act.

Market conduct / consumer protection regulation focuses on how financial institutions behave toward consumers and the marketplace. This includes areas such as fair dealing, disclosure obligations, advertizing practices and so on. In Québec, many of these responsibilities fall under the Autorité des marchés financiers (“AMF”).

Depending on their structure, monoline lenders may fall under federal or provincial oversight. Some operate as federally regulated trust companies supervised by the Office of the Superintendent of Financial Institutions (OSFI), while others operate under provincial mortgage and securities regulation frameworks.

❗Important

The person who connects you with monoline lenders is called a mortgage broker and in Quebec, they are regulated by the AMF.

What is the difference between monoline lenders vs banks?

Many articles simplify the difference between monoline lenders and banks by saying that monoline lenders do not take deposits. While technically true, the distinction runs much deeper. The two operate fundamentally different business models. Here is a summary of some of the differences:

| Monoline Lenders | Banks |

|---|---|

| Raise money to lend from investors and capital markets. | Raise money to lend primarily through customer deposits. |

| Specialize primarily in mortgage lending. | Offer multiple financial products such as chequing accounts, credit cards, investment accounts, and personal loans. |

| Typically do not operate large branch networks. | Operate physical branch locations. |

| May accommodate borrowers who do not meet traditional bank lending requirements. | Often have stricter lending criteria that can make borrowing inaccessible to some borrowers. |

| Often offer greater prepayment flexibility and lower prepayment penalties. | May charge higher penalties for breaking a mortgage early. |

| Typically register mortgages as standard charges because they tend to focus on simpler standalone mortgage products rather than broader banking relationships. | Can register mortgages as either collateral charges or standard charges, often using collateral charges to support products like HELOCs and bundled borrowing. |

What are the pros and cons of working with a monoline lender?

Below are some of the pros and cons of working with a monoline lender compared to a traditional bank.

👍 Advantages of working with a monoline lender:

- Personalized services: Monoline lenders focus exclusively on mortgages. Because of this specialization, lenders can create better and more tailored mortgage solutions for their borrowers.

- Faster processing: Monoline lenders operate heavily streamlined and digitalized mortgage operations. This can result in faster funding timelines compared to some traditional banks.

- Greater payment flexibility: Many monoline lenders offer flexible mortgage features such as accelerated payment schedules, lump-sum prepayment privileges, and customizable payment options that can help borrowers pay down their mortgage faster.

- Lower pre-payment penalties and fees: Compared to many major banks, some monoline lenders charge lower penalties for breaking a mortgage early. This can be beneficial if you refinance, move, or pay off your mortgage before the end of the term.

- Better chances of approval: Monoline lenders are more flexible in the way that they access mortgage applications. This flexibility makes them a good fit for borrowers who are self-employed, have non-traditional income sources, or fall outside standard bank lending criteria.

- Standard charge: Many monoline lenders typically register mortgages as standard charges rather than collateral charges. Standard charges can make it easier and less expensive to transfer your mortgage to another lender at renewal.

👎 Disadvantages of working with a monoline lender:

- Difficult to access in person: Many monoline lenders operate primarily online or through mortgage brokers and may not have physical branch locations. Borrowers who prefer face-to-face banking may find this less convenient.

- One type of service offered: Unlike traditional banks, monoline lenders generally focus only on mortgages and do not usually offer services such as chequing accounts, credit cards, investment products, or business banking.

- Less flexibility for unbundled borrowing: Many banks allow borrowers to bundle mortgages with products like HELOCs and other credit facilities under a collateral charge structure. Monoline lenders may offer fewer integrated borrowing options.

- Broker dependent access: Many monoline lenders work primarily through mortgage brokers rather than directly with the public. As a result, the borrower experience can depend heavily on the quality, knowledge, and lender access of the mortgage broker being used

ℹ️ Note

A lot of people assume monoline lenders are “riskier” than banks. In Canada, that’s often not really true. The downsides tend to be more around convenience and product ecosystems rather than predatory or unsafe lending practices.

Who are the top monoline lenders in Canada?

The top monoline lenders in Canada are:

- First National

- MCAP

- RMG Mortgages

- Merix Financial

- CMLS Financial

- Marathon Mortgage

- Radius Financial

- RFA Bank of Canada

- XMC Mortgage Corporation

- Strive

Frequently asked questions

A few reasons why they are considered safe:

– They are regulated under Canadian mortgage and lending laws.

– Many fund mortgages through government-backed securitization programs like CMHC-insured mortgage bonds.

– They service billions of dollars in mortgages across Canada.

– They are commonly used by mortgage brokers and prime (“A”) borrowers.

They also sometimes offer:

– Lower penalty structures

– Better prepayment privileges

– And “standard charge” mortgages that are easier to transfer at renewal.

However, the lowest rate mortgage is not always the best mortgage. You must also consider things like term, refinance flexibility, rate increases, and whether you need any other products like a HELOC.

For borrowers, what matters less is the label itself and more the structure of the mortgage agreement. Whether the funds come from a bank, a monoline lender, a MIC, or even a wealthy family member, the core arrangement is similar: a lender provides financing secured against real estate, and the borrower agrees to repay the loan under specific terms. Depending on the structure of the deal, any of these lenders may have the legal right to foreclose if the borrower fails to meet those terms.

Final remarks

Monoline lenders have become one of the most important parts of Canada’s mortgage market. While many borrowers still associate them with “alternative lending,” the reality is that many monoline lenders compete directly with major banks and often offer superior mortgage products, lower penalties, and more flexible terms.

For borrowers willing to shop beyond the traditional banking system, monoline lenders can provide access to highly competitive mortgage solutions tailored to a wide range of financial situations.