It’s just one thing that can go wrong when buying a house in Montreal, but it’s a big one.

You’ve found your dream home and, with a lot of excited discussion, you prepare and sign your offer to purchase, and send it to the home seller.

Within 24 hours, your realtor calls you and says that you’ve outbid the competition. In just a few moments the conversation changes direction. You now need to move fast, there is lots to do. First on the list; finalize your financing.

You call the bank to make the pre-approval that you received months earlier official. But the bank is now unwilling to lend you the money. Suddenly, your dreams of moving into your new home are at risk. And, depending on the conditions you set in your promise to purchase, there may even be more at steak.

In this article we cover what to do if your mortgage is denied at closing in Canada, with a specific focus on the province of Quebec. By the end of this article, you will have a comprehensive view of your options, and be able to decide what to do next.

Do you need help with your financing?

You don’t have to figure everything out on your own. If you’d rather skip the stress and get clear answers about your options, you can speak directly with a realtor now.

A good realtor can quickly tell you what solutions may be available based on your situation.

What to do if your mortgage is denied at closing.

Here are four steps to take if your mortgage is denied at closing. The steps outlined below are based on the Quebec real-estate market. However, many of the strategies and concepts discussed may also be useful if you are dealing with a mortgage denial at closing in another Canadian province.

Step 1. Review your promise to purchase

You should start by re-reading Section 5 and Section 6 of your signed Promise to Purchase. These sections tell you what you are legally required to do if your mortgage is denied at closing. Section 5 of the Promise to Purchase is your legally binding commitment to the seller regarding how you intend to pay for the property. Section 6 sets out the mortgage terms you have agreed to accept.

Some important points to understand:

- You may already have agreed to acceptable lending terms.

The mortgage conditions outlined in your Promise to Purchase determine the financing terms that you are expected to pursue. - You must make a good-faith effort to obtain alternative financing.

If your lender denies your mortgage before closing, you may be required to actively seek replacement financing that meets the terms set out in your agreement. - You are responsible for costs associated with obtaining alternative financing.

If an alternative lender charges mortgage origination fees, lender fees, or other financing costs, you may be required to pay them. - You must obtain financing before the deadline set in Section 6.2.

Missing this deadline can create additional risks and may affect your obligations under the agreement. - Leaving Section 6 blank can create significant risk.

If financing terms are not clearly defined, you may have fewer protections and could be pressured to accept financing with less favorable terms, such as a much higher interest rate or additional lender fees. - The seller may have rights if financing conditions are not met.

Depending on the wording of the agreement and the timing involved, the seller may be able to cancel the transaction, choose a lender on your behalf, or pursue other legal remedies.

Once you understand your situation and the terms of your purchase agreement, the next step is determine why your lender denied the mortgage in the first place. It is critical to identify what went wrong since, the solution will depend on the reason for the denial.

Step 2. Work out what went wrong

The next step is to speak with your lender to understand the reason why your mortgage was denied and determine whether there is any room to renegotiate or resolve the issue quickly.

Typically mortgage denial can happen if:

- Your home appraisal came in lower than expected

- Your credit score has dropped

- You made an offer on a home higher than your pre-approved amount

- Your down payment amount is lower than expected

There may be other reasons but, these tend to be the main ones. You should ask your lender to give you the exact reason (or collection of reasons), and take some time to reflect on how best to handle the situation before you attempt to negotiate with them.

Step 3. Look for alternative financing

While you reflect on how best to handle your lender, you should immediately start exploring alternative financing options. If for no other reason, this is so that you understand what backup options are available to you if your original financing cannot be reinstated. To do this, you should contact multiple mortgage brokers and clearly explaining that you need urgent financing support.

You should not disclose unnecessary details about your original lender’s decision. In fast-moving situations, oversharing can sometimes work against you, as lenders may interpret urgency as increased risk, and use this to justify charging a higher rate or offering you less favorable mortgage terms.

Instead, you should focus on presenting your current financial situation clearly and let the mortgage broker assess what options are available. Most brokers will get back to you within 48 hours with their best offers. You can compare this to what you committed to in your promise to purchase, and see if this is something that you are willing to do.

⚠️ Warning

If you are working with a realtor, or if you are unrepresented and dealing directly with the listing broker, they may suggest specific lenders or mortgage brokers. Some referral arrangements may involve compensation or referral fees between the mortgage broker and the realtor.

It is often a good idea to explore multiple financing options rather than relying solely on a referred lender, since comparing offers can help you assess rates, terms, fees, and determine whether the financing is the best fit for your situation.

If you need an independent referral, you can use the Immovision Broker Matching, which is designed to connect you with independent mortgage professionals using data-driven criteria.

Step 4. Get creative

For example, let’s say that your home appraisal came in low, and your mortgage lender denies the full mortgage amount, leaving you with a financing gap. In some cases, a seller may be willing to reduce the purchase price or even offer you a vendor take back mortgage to help bridge the gap. There are also various primary and secondary lender structures that may be available through alternative or B lenders.

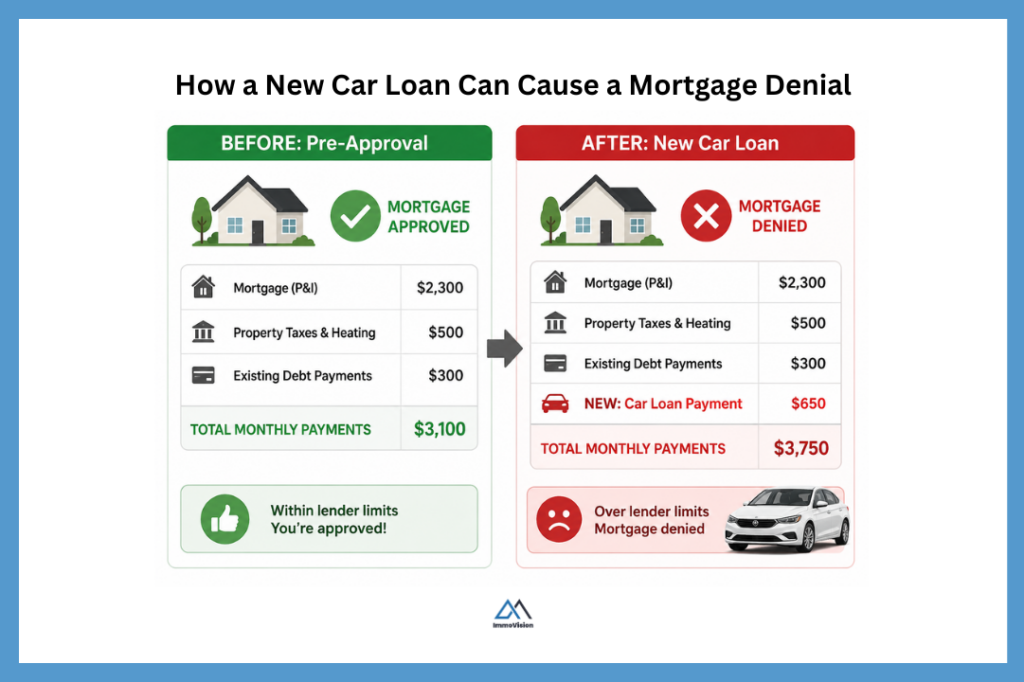

You may also be able to go back to your original lender and see if there is any room to negotiate. For example, buyers who experience a temporary drop in their credit score or debt service ratios after making a large purchase — such as buying a car right before closing — may still be able to negotiate with their lender by explaining the situation, reducing debts, increasing their down payment, or restructuring the mortgage application.

💡 Top Tip

For a complete list of options, it is often helpful to speak with someone who has dealt with this type of situation before. To find someone who can help, you can use the Immovision Agent Finder tool.

This AI-powered search platform helps match you with real-estate professionals who have experience handling situations like mortgage denials at closing and can help you explore possible solutions quickly.

To generate a list of brokers with this experience, simply type in phrases like:

- “mortgage denied at closing”

- “low appraisal financing gap”

- “bad credit mortgage”

- or “vendor take back mortgage”

How to protect yourself from mortgage denial at closing

Here are some steps you can take to protect yourself from mortgage denial at closing.

- Set a financing condition in your Promise to Purchase

- Do a CMA before bidding

- Don’t take on any new debt until the house purchase is complete

- Don’t make an offer you can’t afford

Set a financing condition in your promise to purchase

In Quebec, the Promise to Purchase is a legally binding contract. In this agreement, you agree to buy the home according to the terms set out in the agreement. This includes the financing terms that you are willing to accept in order to complete the purchase.

If your mortgage is denied at closing and the financing condition has been properly defined, you may be to get out of your promise to purchase without losing your deposit or facing legal consequences. However, if you have not included this condition, the seller may be able to force the transaction forward by finding alternative financing for you — potentially at terms that are significantly more expensive or not in your best financial interest.

Do a CMA before bidding

A lender may deny your mortgage if the home appraisal comes in too low, because lenders generally do not want to lend more money than the property is worth.

This means that if you bid, say, $500,000 on a property that is only worth $450,000, the lender may base the mortgage on the $450,000 appraised value instead of the purchase price, leaving you responsible for covering the difference yourself. To help avoid this situation, it is important to complete a CMA (or Comparative Market Analysis) before agreeing to a purchase price.

A CMA is an estimate of a property’s market value based on the recent sale prices of similar homes in the area. A good CMA takes into account local market conditions, recent comparable sales, and unique property characteristics such as block foundations vs. concrete slabs, the condition of major systems, maintenance requirements, zoning, rental potential, renovations, and neighborhood-specific factors.

A strong CMA can help reduce the likelihood of a low appraisal by ensuring that your offer is supported by real market data. It can also reduce the risk of overpaying for a property and may provide evidence you can use to challenge a low appraisal if the lender values the property below the agreed purchase price.

Don’t take on any new debt until the house purchase is complete

One of the key factors lenders review when approving your mortgage is your debt service ratios — specifically your GDS (Gross Debt Service) and TDS (Total Debt Service) ratios. These ratios help determine whether you can realistically afford the monthly costs associated with the home.

Taking on additional debt during the home buying process can increase your monthly obligations and negatively affect these ratios. Even if you qualified initially, if you take out a new loan this can push your debt levels above the lender’s acceptable limits, which may result in your mortgage being reduced or denied.

This commonly happens when buyers make major purchases before closing, such as buying a new car, financing furniture or appliances, or opening new lines of credit. While these purchases may seem manageable on their own, the additional monthly payments can significantly impact your mortgage qualification.

For this reason, it is generally best to avoid taking on new debt, applying for new credit, or making large financed purchases until your home purchase has fully closed.

Don’t make an offer you can’t afford

Before you start house hunting, know your real budget. This includes your down payment plus your mortgage pre-approval amount. You should also understand what your monthly mortgage payments will look like and consider getting a mortgage rate hold, which can help protect you if interest rates increase while you’re shopping.

Buying a home is an emotional experience. In competitive markets like Montreal, buyers can feel pressure to stretch their budget or overbid just to secure a property. However, if you agree to pay more than you can realistically afford and your mortgage is later denied at closing, you may be forced to seek financing from alternative or private lenders to complete the purchase.

These lenders may charge significantly higher interest rates and additional costs. Combined with the already higher costs of homeownership compared to renting, this can place considerable financial pressure on you and turn your first few years of homeownership into a stressful experience rather than an enjoyable one.

Frequently asked questions

Depending on how the financing condition was drafted, you may be required to make a good-faith effort to obtain alternative financing from another lender. In some cases, this can include accepting financing with different terms, higher interest rates, or additional lender fees if those terms still fall within the conditions you agreed to in the contract.

You should also speak with your lender immediately to understand why the mortgage was denied. Common reasons include a low appraisal, changes to your income or employment, a drop in your credit score, increased debt levels, or issues uncovered during the lender’s final review.

In many situations, buyers are still able to complete the purchase by working with a mortgage broker, negotiating with the seller, increasing the down payment, or obtaining alternative financing through another lender.

This means that both the buyer and seller are typically obligated to complete the transaction according to the terms set out in the agreement. The Promise to Purchase includes important conditions relating to financing, deadlines, inspections, deposits, and other obligations.

Whether you can legally withdraw from the agreement depends largely on the specific conditions included in the contract. For example, a properly drafted financing condition may allow you to cancel the transaction if you are unable to obtain financing that meets the terms outlined in the agreement.

Because every situation depends on the wording of the agreement and the surrounding facts, it is often important to obtain professional advice if financing problems arise close to closing.

If your Promise to Purchase contains a properly drafted financing condition, and you made a genuine good-faith effort to obtain financing within the deadlines set out in the contract, you may be able to cancel the transaction without penalty if financing cannot be obtained on the agreed terms.

However, if the financing condition is vague, incomplete, expired, or missing entirely, the situation becomes much more complicated. In some cases, the seller may argue that you are still obligated to complete the purchase or attempt to claim damages if the transaction fails to close.

Before attempting to cancel the agreement, you should:

– Review the exact wording of your financing condition

– Confirm whether all financing deadlines were respected

– Gather written proof of the mortgage denial

– Speak with a real estate lawyer or notary as soon as possible

– Explore whether alternative financing solutions are still available

In some situations, buyers are able to negotiate a mutual cancellation with the seller, especially if financing problems are identified early and communicated properly.

Final remarks

Mortgages can be denied at closing for a whole host of reasons, including changes in your income, taking on new debt, issues with the property appraisal, credit score declines, employment changes, or problems identified during the lender’s final review.

There are usually solutions available, but unless you’re very familiar with home financing and mortgage negotiations, it’s often best to work with someone who handles these situations on a daily basis.

To find an agent with the right experience for your specific needs, you can use the Immovision Agent Finder Search tool. It’s a free AI-powered search tool that has been trained on millions of data points from sources such as OACIQ, Google Reviews, the Multi-National Listing Service, and much more. The search tool will find you a suitable real estate professionals based on your exact situation.