Are you considering downsizing for retirement? Before you make this decision, there are several things that you need to consider because, the truth is that downsizing for retirement is really not about square footage, it is whether downsizing supports the type of lifestyle that you want to live in retirement.

In this article, we will help you think through this decision by giving you some advice we have heard from clients who are considering downsizing. This will include:

- Financial cost of downsizing for retirement

- Alternatives to downsizing for retirement

- How downsizing affects your retirement lifestyle

- Frequently asked questions

- Final remarks

Financial cost of downsizing for retirement

For many Quebecers, the home they live in is their largest asset. After decades of mortgage payments, renovations, and rising property values, many people now hold more wealth in their homes than in their RRSPs or other investments. As such, it’s natural to think that selling and downsizing will unlock that equity, put cash into your bank account, and lower utility bills and property taxes.

However, as we are about to see, selling isn’t the only way to access your home’s value, and downsizing for retirement comes with significant costs. In this section, we briefly compare the costs of downsizing versus staying put. We will also share some of the most popular alternatives that Quebecers are using to sell their home in retirement.

What is the financial cost of downsizing?

When you consider the financial cost of downsizing, there are three main costs to consider. These are:

- The cost of selling your current home

- The cost of transitioning into your next home

- The ongoing carrying costs of the new property

Let’s compare each of these downsizing costs against the cost of remaining in your existing home.

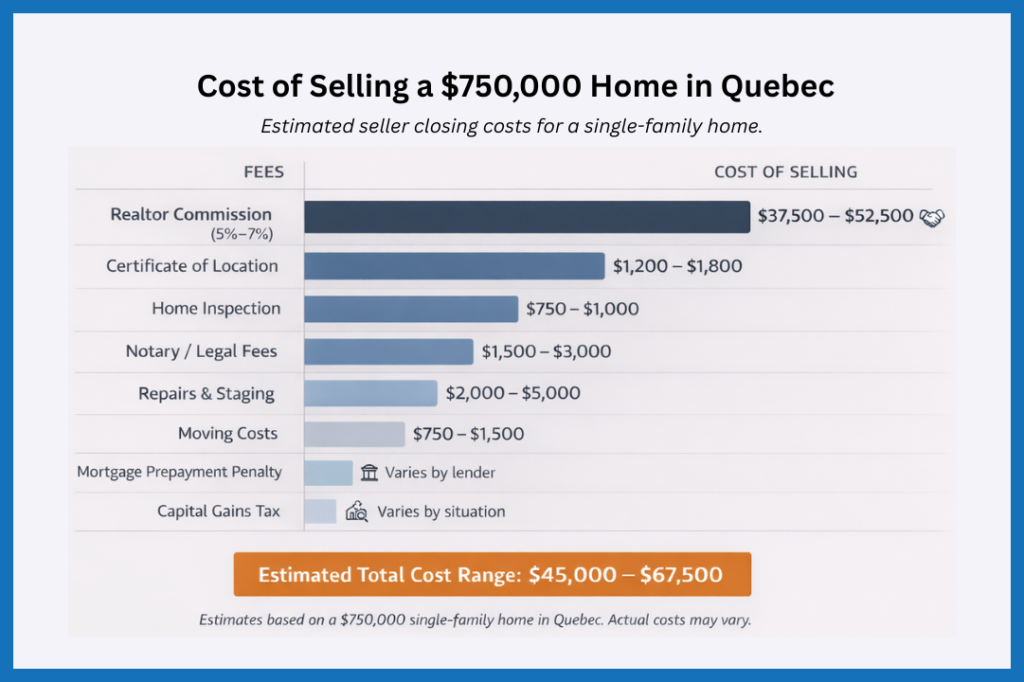

The cost of selling your current home

The average cost of selling your home is typically 5%–7% of the sale price. Below is an example of how this could the cost of selling might look for a single -family home (detached, semi-detached or townhouse) in Montreal.

The cost of transitioning into your next home

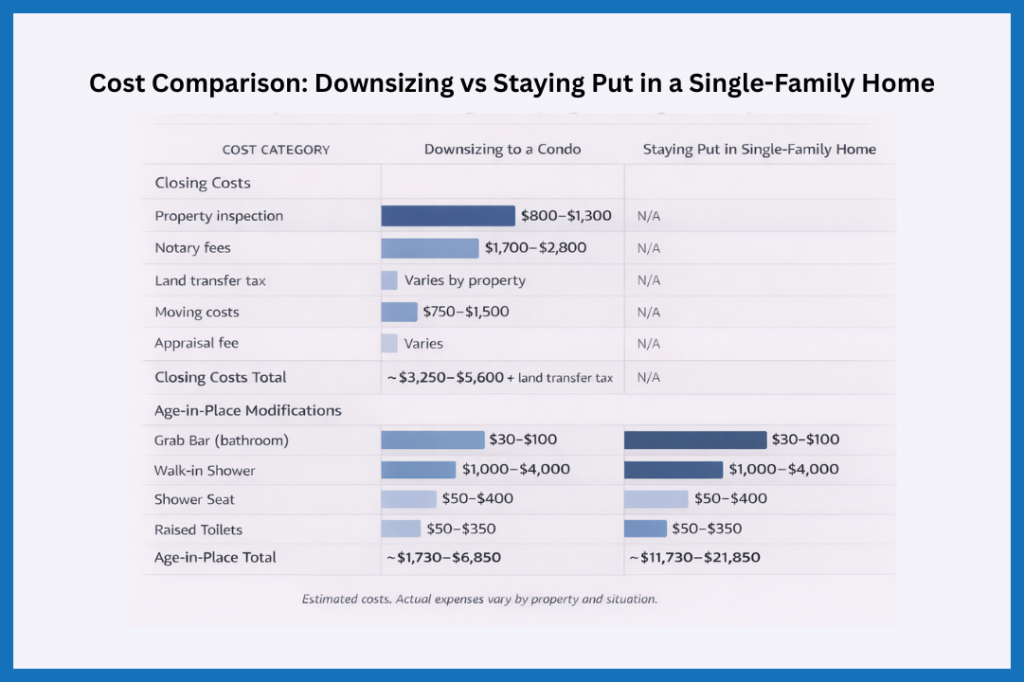

On top of the usual selling costs, you will also need to factor in the cost buying a new place or, moving into rented accommodation. The cost of buying includes the standard closing costs and any age-in-place renovations that you need to make to your new home such as walk-in shower, access ramps, a raised toilets and so on.

Alternatively, if you choose to stay put, you will most likely still need to make age-in-place modifications to your existing home. Below is a comparison of the type of costs you may experience when downsizing to a condo vs staying put in a single-family home. As you can see, when you factor in land transfer tax, the cost of moving is likely to be roughly the same as making modifications to your existing home.

Calculate your exact land transfer tax

The ongoing carrying costs of the new property

Downsizing does not automatically reduce your monthly housing costs. If you downsize and live in a new property for 20 – 30 years, then during this time, you will face rising property taxes, condo or maintenance fees, utility costs, and (very likely) the need to complete essential and major repairs and renovations to your new home.

Many homeowners wrongly assume that moving means escaping the expenses they already know are coming up in their current home such as the roof replacement, plumbing upgrades, or bathroom remodel. In reality, every property comes with its own surprises, and repairs can costs just as much as in your previous home. As such, the long-term costs of downsizing depends heavily on the type of property you move into and the quality of its construction.

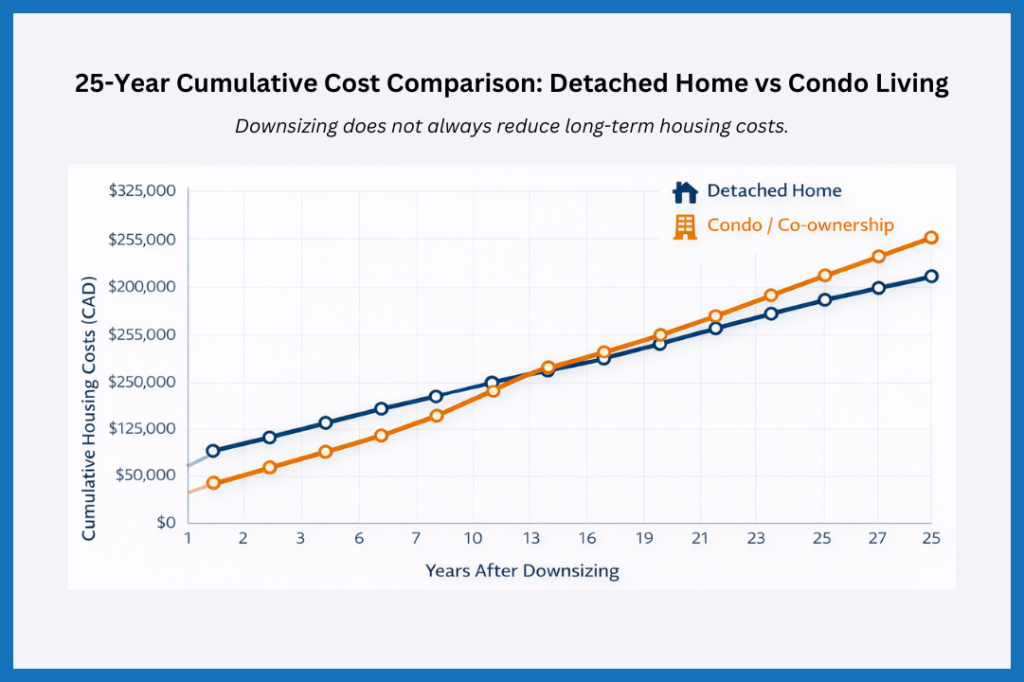

For instance, consider the following scenario. You move out of a detached home and into a divided co-ownership. If the co-ownership management has not looked after the property well, you may need to make substantial contributions to the contingency fund over the next 25 years. This can come in the form of special assessments or rising condo fees. Below is an example of how much costs might vary over a 25 year period. In the financial model we have assumed that the carrying costs for a detached home are higher in the first few years, so as to account for immediate maintenance. After this period of time, the cost of condo living increases as condo fees and the number of special assessments rise.

The best way to understand the potential costs of staying put vs moving is to work with professionals who can accurately estimate the cost of repairs and ongoing maintenance to your existing or new home, check historical property tax trends in your area, review the building’s financial statements and contingency fund (if buying a condo or co-ownership), and assess expected increases in insurance, utilities, and condo fees.

If you decide to buy somewhere new, make sure that you get a thorough pre-purchase inspection to identify structural, mechanical, or deferred maintenance issues.

You can then put this information into a cost control calculator to work out your projected 20–25 year housing costs under each scenario and make a fully informed decision.

Free Downsizing Financial Blueprint

[Start My Free Analysis →]

Alternatives to downsizing for retirement

As you can see, the cost of downsizing for retirement is not always lower just because you have cut the amount of square footage that you need to manage or, because you thought you could sidestep the maintenance and repairs you know are coming in your current home. All that being said, many people need access to cash in retirement. If you have built up significant home equity, it is logical to assume that selling your home provides the most direct way to access that cash, even if you would prefer not to move.

However, there are other ways to get equity out of your home without selling it. The most popular option here is either a reverse mortgage or home sharing.

Reverse mortgage

A reverse mortgage is a financial product that allows homeowners, typically aged 55 or older, to convert part of the equity in their home into cash without having to sell the property or make monthly mortgage payments. The loan is repaid only when the homeowner sells the home, moves out permanently, or dies.

For example, let’s say that you have a property worth $750,000. With a reverse mortgage, the lender will allow you to borrow a portion of your home’s equity — typically between 25% and 50%, depending on your age and the property value. The lender will typically give you the money as a lump sum, line of credit, or monthly payments. You do not need to make monthly mortgage payments, and the loan is repaid only when you sell the home, move out permanently, or pass away.

Note

Home sharing

Home sharing is when a homeowner rents out a part of their home such as a spare bedroom, basement, or accessory suite to a tenant, often a friend, family member, or another compatible resident. Statistics Canada found that among Canadians aged 75 and older, about 8 % (roughly 200,000 retires) share their homes with other family or non‑family individuals in retirement.

For retirees, homesharing can be a flexible way to access home equity through rent, maintain independence, and stay connected to their community without selling or downsizing. In this case, you may need to make some modifications or renovations to provide privacy and comfort for both yourself and your tenant. To make these renovations, you can consider various short term funding options such as a Home Equity Line of Credit (HELOC). The federal government also offers a Multigenerational Home Renovation Tax Credit (MHRTC) to help with the cost of creating a self‑contained secondary unit within your home.

How downsizing affects your retirement lifestyle

Now that you understand some of your financial options, it’s important to step back and consider the bigger picture. Retirement decisions are not just about numbers; they also involve lifestyle, identity, and how you want to spend your time. Many of us feel a natural pull to simplify in retirement. Over the years we accumulate things that later seem unnecessary, and reducing clutter can bring real relief and allow us to focus on what truly matters.

However, while cancelling a subscription might be simple, downsizing your home does not automatically bring greater happiness or peace of mind. Your home connects you to your community, anchors your daily routines, holds family memories, and gives you a sense of stability. Before making a move, it is worth reflecting on a few key questions about how a change might affect your relationships, lifestyle and future fit.

1. Relationships: Will downsizing strengthen or weaken your connections?

Retirement often increases the value of proximity to children, grandchildren, friends, and familiar neighbours. Before making a move, consider whether downsizing brings you closer to the people who matter most, or distances you from your support network.

Distance is not always about the physical space that separates you. It can also mean missing out on shared time. So think about if your new place will make it easier or harder for your family and friends to visit you. This could mean choosing a place with a spare room where you can have grandchildren sleep over or that is close to good transport links.

Before you make a decision, you can also re-explore your community as a retiree. Find out what is on offer in terms of social activities, clubs, classes, and local events. You may find ways to enjoy your community that you didn’t know existed.

2. Lifestyle: Does your new home support the way you want to live in retirement?

Ask yourself if there are things about your current space that you enjoy. And, if you decide to downsize, will your new home have these same features? For instance, many retirees like to garden, or enjoy their south facing gardens. Conversely, certain aspects of your home may become more difficult over time; for instance, a narrow driveway leading onto a busy road can be tricky to manage as you get older.”

Downsizing is a big decision. If you’re considering a move to a city condo or retirement community, some retirees try a short-term rental first. Living there for a few months can help you see whether you prefer this style of living over the comfort, space, and routines of your current home.

3. Future Fit: Will this home still work for you 20–30 Years From Now?

Retirement can last a long time and so it is important to think beyond today. Consider mobility, maintenance, layout, and long-term comfort. The goal is not just to reduce space, it is to ensure your home remains practical and supportive as your needs change. To this extent, you may decide to stay where you are but repurpose empty rooms for hobbies, exercise, storage, or visiting family, making your home work better for your retirement lifestyle.

Frequently asked questions

1. Overestimating your homes value – lots of people will look at what prices properties similar properties are listed at in their area and make their own assessment on the value of their property. However, estimates are generally inaccurate and can skew your planning. It is much better to get a local expert to run a comparative market analysis (or CMA) so you have a realistic, evidence-based valuation, which will ultimately help plan this important decision without taking an unnecessary risk.

2. Underestimating how long and how emotionally draining decluttering can be – Many people do not realize that downsizing a large home can take one to two years. Starting too late forces rushed, stressful decisions, and can replace a thoughtful transition with panic and regret.

3. Underestimating new home costs – Many people think that by downsizing they will avoid known renovations in their existing home and reduce their monthly expenses. The reality is that you will be potentially living in your new home for 20+ years — more than a quarter of your life. With that in mind, you should carefully consider not just the purchase price, but the long-term costs of maintenance, repairs, upgrades, and how well the property will support your needs over time.

4. Not thinking carefully about your future lifestyle – Many people downsize too much and later regret not having enough space. It’s often a good idea to think beyond your immediate needs and consider how you’ll actually live in the home over time. Having an extra room for visiting grandchildren, space for family to stay overnight, or enough room to host gatherings and celebrations can make a big difference to your comfort and quality of life. Choosing a home that supports how you want to spend time with the people who matter most will help ensure your new space feels welcoming, flexible, and truly fit for the years ahead.

– Early retirement (mid-50s to early 60s) – Many people downsize just before or soon after stopping full-time work. This can free up equity, reduce bills, and simplify life while you’re still active enough to manage the move easily and enjoy the benefits for longer.

– Around pension age (mid-60s to early 70s) – This is one of the most common times. Your income is usually clearer, your housing needs are easier to predict, and you can choose a home that better supports your long-term lifestyle. In the United Kingdom, many people consider downsizing around State Pension age for this reason.

– Later retirement (75+) – Some wait until maintaining a larger home becomes physically demanding or unnecessary. While this can still work well, moving later in life can feel more stressful and limiting in terms of options.

Final remarks

Downsizing for retirement is not a silver bullet that will automatically unlock equity or simplify your life. While it can do this for some, it might not for others, especially if the move disrupts routines, social connections, or the sense of comfort you’ve built over the years.

Retirement lasts for roughly a quarter of your life and just as when you bought your first home, it’s important to weigh both financial and personal factors before making a decision. If you want to stay put, then take a look at the financial options that are available to you but, if you want to move and get closer to family, make sure that you carefully plan your finances around the lifestyle you want for this new stage of life.