A reverse mortgage gives Canadians over the age of 55, a mechanism to access the equity in their home, whilst keeping their home until they die or eventually decide to sell their home. The most common use case for a reverse mortgage is to supplement retirement income. However, whilst a reverse mortgage is a good idea for some people, there are some cases where it does not make sense. In this article we cover:

- What is a reverse mortgage?

- Requirements to qualify for a reverse mortgage in Canada

- How a reverse mortgage works in Canada

- How much can I borrow based on my age and home value?

- What are the costs of a reverse mortgage in Canada?

- What are the pros and cons of a reverse mortgage

- Improper uses of a reverse mortgage

- Positive uses of a reverse mortgage

- Reverse mortgage vs HELOC

- Where can you get a reverse mortgage in Canada?

- Frequently asked questions

- Final remarks

What is a reverse mortgage?

A reverse mortgage is a type of loan that allows Canadian homeowners who are 55 years or older to access the equity in their home as tax-free cash, without having to sell the property or make regular monthly repayments. Instead of paying down the loan over time, the loan is usually repaid when the homeowner sells the home, moves out permanently, or passes away.

Requirements to qualify for a reverse mortgage in Canada

When you apply for a reverse mortgage in Canada, the lender will look at the following factors.

- You must be at least 55 years old (if you have a spouse on title, both must be 55 or older)

- Use the property as your primary residence for at least six months of the year

- Own a qualifying property, such as a detached home, condo, townhouse, semi-detached home, or plex

- Have sufficient home equity

- Have a minimum appraised home value of around $250,000

- Own a property in an eligible location, usually major urban centres like Toronto or Montreal.

In each case, the following rules are generally true:

Remember, equity is the current market value of your home minus any remaining mortgage that you have on the property. To work out the market value of your home, the lender will do a home appraisal. This is to ensure that they are not lending more than the home is actually worth.

Free Valuation

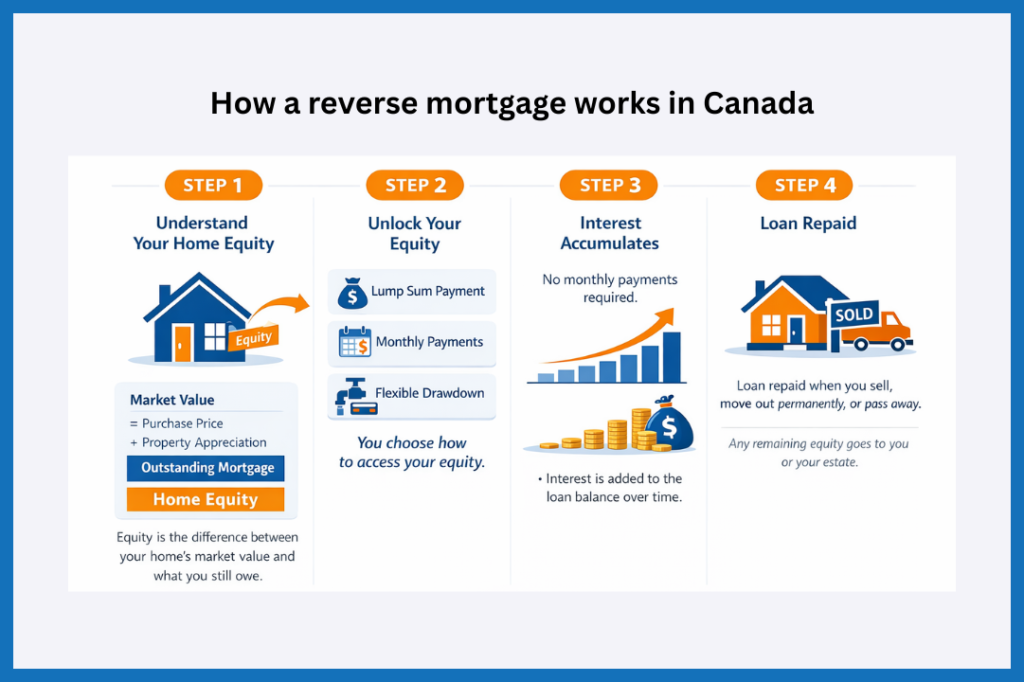

How a reverse mortgage works in Canada

The exact way that your reverse mortgage works depends on the type of reverse mortgage you get and how you receive the initial equity release. Typically there are three ways that you can get access to your home equity. These are:

- Receive a lump sum payment

- Equal payments every month

- Flexible drawdown (similar to a line of credit)

In all of these cases, once funds are withdrawn, the lender applies either a fixed or variable interest rate, depending on the type of reverse mortgage you choose. Unlike a traditional mortgage, you don’t make monthly interest payments. Instead, the interest accumulates over time and is added to the total loan balance.

The loan is typically repaid when you sell the home, move out permanently, or pass away. At that point, the property is sold and the loan balance (including all accumulated interest) is paid to the lender. If any equity remains after the loan is settled, and the remaining funds go to you or your estate.

With a reverse mortgage you still retain ownership and occupancy of your home. Because of that, you remain responsible for:

- Paying your property taxes

- Taking out home insurance

- Paying for maintenance and repairs

- Paying your condo fees or special assessments

- Paying your utilities and local fees

- Living in the home as your primary residence (usually at least six months per year)

Failure to meet these obligations can lead to penalties or even default. In such cases, the lender may have the right to foreclose on your home to recover the loan.

Note

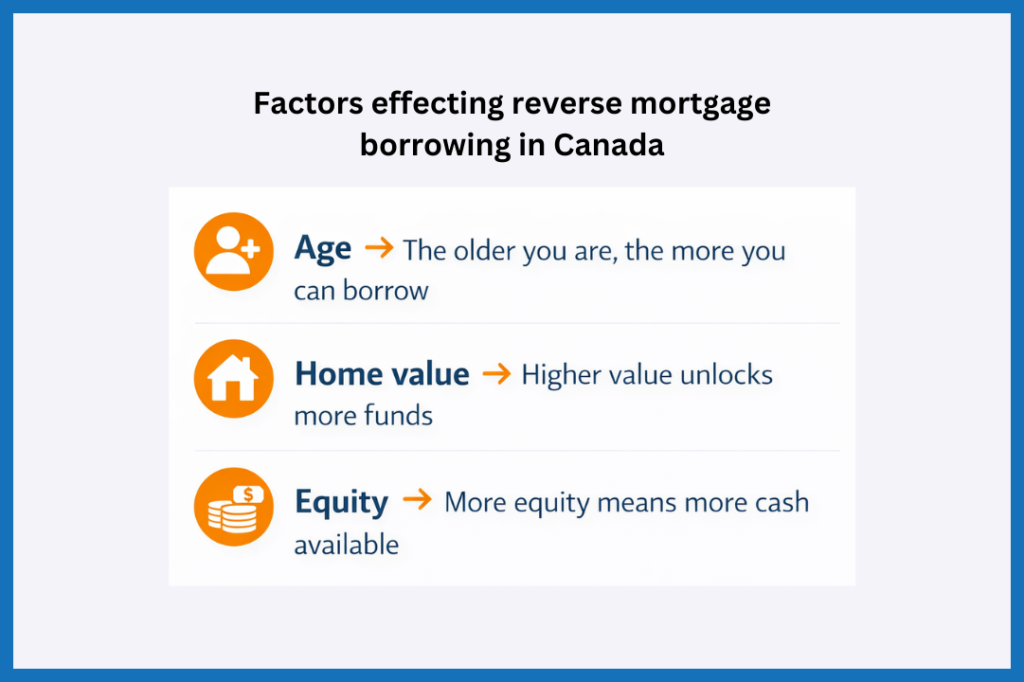

How much can I borrow based on my age and home value?

Most Canadian lenders will allow you to borrow up to 55% of your home value and in some cases, lenders will allow you to borrow up to 59% of your home value. Because the loan is secured against your home equity, lenders will look at how much equity you have in your home. Home equity is calculated as the current market value of your home minus any unpaid mortgages or other loans that you have secured against the property.

For example, let’s say that you bought your home in 2001 for $250,000 and, after years or property price appreciation and personal investment, it is now worth $750,000. Let’s say that you also have an outstanding mortgage of $50,000 on the property. In this case, your total equity will be $750,000 − $50,000 = $700,000. This means that you could qualify for between $385,000 and $413,000. The first $50,000 would be used to pay off your existing mortgage, leaving approximately $362,500 available to you.

What are the costs of a reverse mortgage in Canada?

Reverse mortgages are not free. In fact, reverse mortgages are more expensive than either home mortgages or Home Equity Line of Credit. This is for two main reasons:

- Reverse mortgages charge a higher rate of interest

- Interest added to the loan compounds

Reverse mortgages typically charge a higher rate of interest compared to other loans. This is because lenders take on more risk with a reverse mortgage. Repayments are usually not made monthly, and the loan may not be repaid for many many years.

During the time that you have the loan, you are not paying down any of the mortgage. This means that you interest rate not only works in reverse, but it actually compounds over time. Consider the following example for a $300,000 home mortgage at 5% interest, paid over 25 years vs a reverse mortgage for the same amount paid as a lump sum. As you can see, the effect of the compound rate makes the reverse mortgage more than 3x more expensive over a 25 year term.

| Year | Home mortgage balance | Reverse mortgage balance |

|---|---|---|

| Start | $300,000 | $300,000 |

| 5 years | $265,800 | $382,900 |

| 10 years | $221,700 | $488,700 |

| 15 years | $165,300 | $623,700 |

| 20 years | $93,000 | $795,900 |

| 25 years | $0 | $1,015,800 |

| Total interest cost | $225,600 paid | $715,800 added to loan |

| Total repaid / owed | $525,600 paid in total | $1,015,800 owed at end |

Of course, you do not need to take all of the $300,000 as a lump sum payment with a reverse mortgage, which can significantly reduce amount you owe at the end of 25 years.

Other costs of a reverse mortgage in Canada

Other costs associated with the mortgage may include:

- Home appraisal fees

- Set-up fees

- Pre-payment penalties (if you pay off your mortgage before it is due)

- Closing costs

Note

What are the pros and cons of a reverse mortgage

Here are some of the pros and cons of a reverse mortgage in Canada.

The pros of a reverse mortgage are:

- No income verification – Because the reverse mortgage does not require you to make fixed monthly payments the lender does not need you to prove that you have a stable income stream to make the payments. You will still need to meet the other qualification requirements for a reverse mortgage.

- No repayment during your lifetime – You don’t need to repay a reverse mortgage unless you sell, move out permanently, or pass away. This means that you can remain in your home for life, provided you continue to maintain the property and keep up with property taxes, insurance, and utilities. If you have a spouse who outlives you, they must continue meeting these obligations to stay in the home.

- Reverse mortgage payments are tax free – Because the funds are not treated as taxable income, they typically do not impact income-tested social benefits such as OAS (Old Age Security) or GIS (Guaranteed Income Supplement).

- No negative equity guarantee – The most you or your heirs will ever owe is the fair market value of your home when it’s sold. If the home sells for less than your reverse mortgage balance, you are not responsible for the difference.

The cons of a reverse mortgage are:

- Higher rate of interest – Reverse mortgages offer the highest rate of interest compared to either regular home mortgages, refinancing or HELOCs.

- Equity declines over time – A reverse mortgage reduces the equity that you own in the property over time.

- Reduced inheritance – Even though the lender may only give you 55%–59% of your home’s value, this doesn’t mean there will be any equity left over for you to pass on to your heirs. In fact, the interest that you don’t pay each month is added to your loan balance, and the lender charges interest on that interest. This is called compounding, which will magnify the speed and total cost of the mortgage. Over time, especially if you live many years, the loan can grow enough that the lender ends up owning most or all of your home’s value, leaving little or nothing for your heirs.

- Upfront and ongoing fees – Most reverse mortgage lenders will charge you high home appraisal fees, set-up fees and closing fees that are deducted from the amount that they will lend to you.

- No mental health provision – Many aging people suffer from dementia and may be unable to manage keep up with regular property tax payments, property maintenance, utility bills and insurance. If this happens, the reverse mortgage provider may be able to foreclose on your property.

- Limited lender choice – In Canada, reverse mortgages are not offered by mainstream banks and, there are very few lenders that will give you a reverse mortgage.

Improper uses of a reverse mortgage

The most common mistakes that people make when taking out a reverse mortgage are:

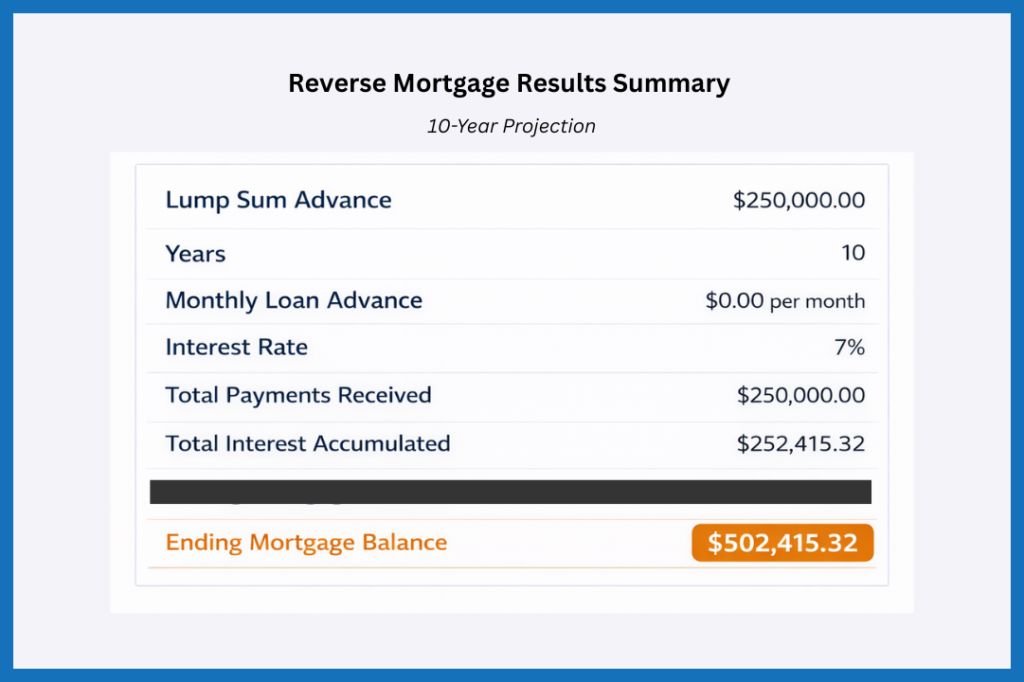

Starting too soon

Let’s say that you take out $250,000 in a reverse mortgage at the age of 62, this means that after 10 years, with a 7% rate of interest, your total ending mortgage will be $502,415.32.

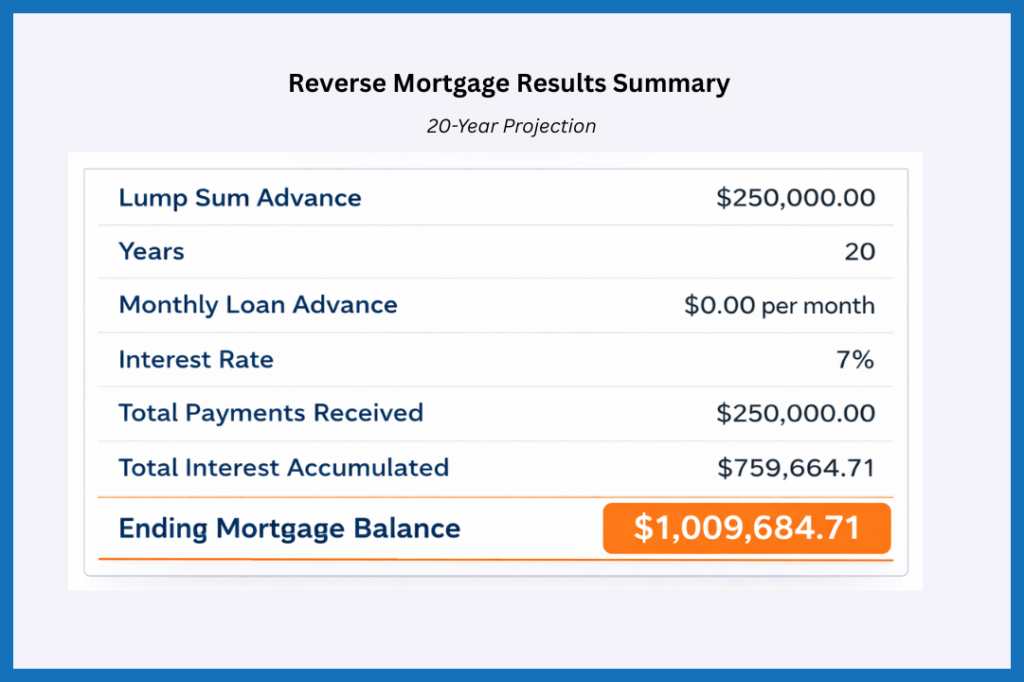

Now, at the age of 72 you will likely to continue living for another 10 years. At this point, the mortgage total will grow to approximately $1,009,684.71.

In this scenario, if you are running low on liquid assets once you reach your mid-seventies, you will not have the flexibility to refinance, relocate, or manage unexpected healthcare or living expenses without putting significant pressure on your remaining home equity.

Not communicating with family

Quite often, reverse mortgages end badly if the heirs to your estate are not aware of them. In this case, your children or other heirs may be expecting to receive your home in their inheritance. However, if there is a reverse mortgage in place, the lender can take and sell your home after you pass away, so as to recover the outstanding loan balance.

Often, family members are unaware that a reverse mortgage was taken out. It’s only when they begin reviewing the estate and discussing the will that they discover the home is subject to a substantial reverse mortgage balance, significantly reducing the inheritance they expected to receive.

Not considering health risks

As we age, it’s common to experience changes in health that may require additional support.

The terms of a reverse mortgage require that you keep up to date with property taxes, homeowners insurance, and ongoing home maintenance. However, if your health declines or you experience a period of cognitive or physical incapacity, managing these responsibilities can become more difficult. An extended hospital stay or move into assisted living, for example, may make it challenging to stay on top of these obligations. If the loan conditions are not met, the lender may have the right to call the loan due.

One practical way to prepare for this possibility is to grant an enduring power of attorney to a trusted family member or advisor, who can step in to manage your financial affairs, ensure taxes and insurance are paid, and help maintain compliance with the terms of the loan.

Positive uses of a reverse mortgage

Most of the downsides of a reverse mortgage occur when they are used incorrectly. For others, they can be a great tool. For instance, consider a slightly older retiree couple, in their mid 80s. In this case, they may be running low on liquid funds and, in this case, they may want to take out a reverse mortgage to suplement lifestyle needs and, to get more care provided to them in their home.

In this case, the retiree couple should be clear in their intentions and speaks with their family and loved ones about their intentions. In some cases, this may even provide family members the opportunity to offer their own financial, physical and emotional support, so that the older person can avoid the high cost of a reverse mortgage.

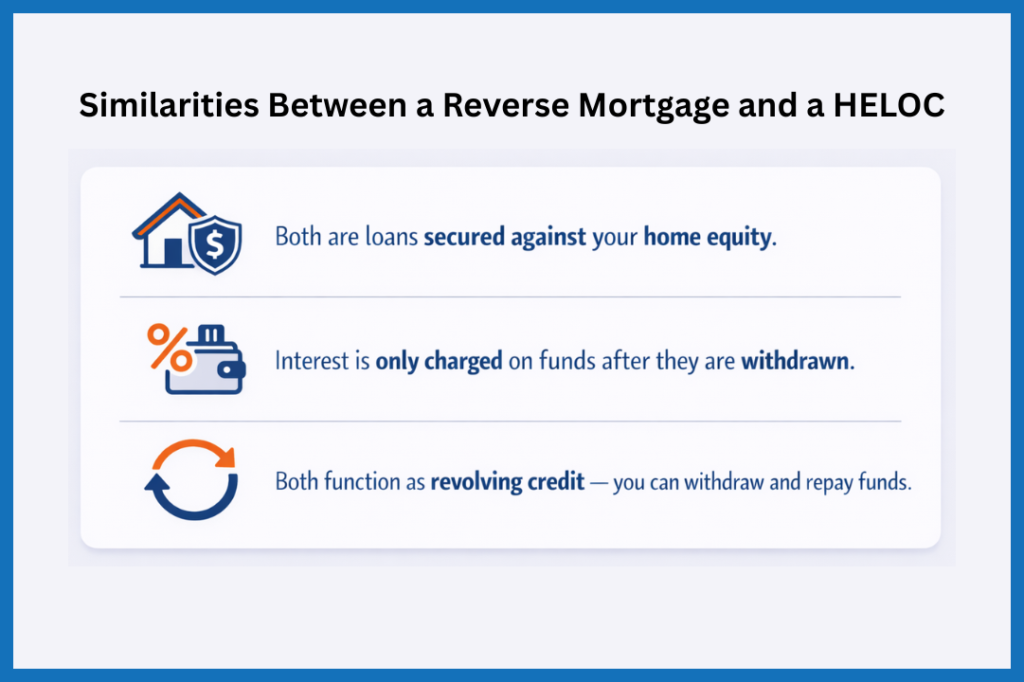

Reverse mortgage vs HELOC

Both reverse mortgages and Home Equity Line of Credit (HELOC) allow you to access equity in your home. They are similar in the following ways:

However, a reverse mortgage is quite different from a HELOC in several ways, in particular how the revolving credit line works. The table below shows the key differences between reverse mortgages vs HELOCs.

Reverse Mortgage vs HELOC — Key Differences in Canada

Where can you get a reverse mortgage in Canada?

In Canada, reverse mortgages are provided by a small group of specialized lenders rather than being widely offered by the major banks. HomeEquity Bank offers the CHIP Reverse Mortgage nationwide, available directly to homeowners or through mortgage brokers. It also provides alternative access options, such as the Bloom Home Equity program, which allows eligible homeowners to draw funds gradually instead of taking a lump sum upfront.

Equitable Bank distributes its reverse mortgage primarily through brokers in select major cities across Ontario, British Columbia, Alberta, and Quebec. In addition, Home Trust offers reverse mortgage products through the broker channel, typically with more limited geographic availability and eligibility requirements.

Note

Frequently asked questions

To do this, you will need to make a large downpayment on the new home, usually between 45% – 65% of the purchase price. This money will need to either come from your own personal savings or from the proceeds of selling your previous home. Then, instead of taking a regular mortgage for the rest of your life, you can use a reverse mortgage on the new property to cover the remaining amount.

The home itself acts as security for the loan and you do not need to make monthly payments. Instead, the interest gets added to the loan balance over time. The loan is repaid when you sell the home, move out permanently, or pass away.

How much you can borrow in depends on your age and the home’s value, but it’s typically between 10% and 59% of the property’s value.

One important thing to remember: reverse mortgage interest rates are usually higher than traditional mortgage rates. Because you’re not making payments, the loan balance grows over time, which can reduce the equity left in your home later.

Here’s what that means for your heirs:

– Your heirs can sell the home, repay the reverse mortgage, and keep any remaining equity.

– If they want to keep the home, your heirs must repay the loan (usually by refinancing or using other funds).

– If the home’s value is less than the loan balance, most Canadian reverse mortgages are “non-recourse”, meaning your heirs are not personally responsible for paying the shortfall. The lender can only claim the value of the home.

Example

– Home value at death: $800,000

– Reverse mortgage balance (including interest): $450,000

– Remaining equity for heirs: $350,000

However, if the loan balance were $820,000 and the home sold for $800,000, your estate would not owe the extra $20,000 (with most major Canadian reverse mortgage products).

Final remarks

A reverse mortgage is a financial product for Canadians that are 55+ years old. It allows you to get access to equity in your home and is primarily used by Canadians in the later stage of their retirements. Although the product can work for some people, it can be misused. As such, it is very important to think about what your long term financial goals are and run the numbers for the different scenarios. To do this, we would recommend that you speak with a trusted financial planner who can advise you, not just about reverse mortgages but also give you access to the most up to date information.