Buyers Closing Cost Calculator Quebec

Closing costs typically represent 2-4% of the purchase price for the property. For a more accurate estimate of your closing costs, use our closing cost calculator below.

Professional Fees & Insurance

Additional Moving Expenses (Optional)

Want To Reduce Your Closing Costs?

Planning to buy soon? The right real estate agent will help you calculate your total closing costs and identify rebate programs so that you can avoid overpaying for your home.

What are closing costs?

Closing costs are all the one time expenses you need to pay when you buy a property. These costs are in addition to your down payment. Closing costs include the legal, administrative and government fees required to officially transfer ownership from the seller to you.

You usually pay closing costs around the time you close, and they typically total between 2% and 4% of the purchase price. The table below shows how much you will need to pay for homes of different prices. For example, 5% on a property worth $450,000 is $22,500.

| Example Property Price | Estimated Closing Costs (2%) | Estimated Closing Costs (4%) |

|---|---|---|

| $350,000 | $7,000 | $14,000 |

| $400,000 | $8,000 | $16,000 |

| $450,000 | $9,000 | $18,000 |

| $500,000 | $10,000 | $20,000 |

As you can see, these are not insignificant amounts. So what exactly are you paying tens thousands of dollars in closing costs for? And where can you afford to cut costs?

What are the most common types of closing cost in Quebec

The most common types of closing cost are the land transfer tax (the welcome tax), and the notary fees. Generally, the Quebec real-estate process does not require you to hire lawyers.

Land transfer tax (welcome tax)

When you buy a property in Quebec, you must pay land transfer tax. Municipalities charge this duty whenever a property transaction takes place. The way it works is, you will first sign the deed of sale that marks the completion of the transaction. The notary will then update the Quebec Land Register to reflect the details of the transaction. Once the notary has updated the land register, the relevant municipality gets automatically notified about the details of your transaction. The municipality will then calculate how much land transfer tax you owe and send you an invoice. You should receive the invoice within 90 days of your home purchase.

Land transfer tax is a progressive tax that municipalities calculate based on the higher of the property’s purchase price or assessed value. This means the municipality will tax different portions of the property’s value at different rates. In Quebec, each municipality must apply the minimum land transfer tax rates set by the provincial government. Individual municipalities may impose higher rates and add additional brackets. This is why land transfer tax varies significantly from one city to another.

💡 Free Welcome Tax Calculator

Use our free 2026 Welcome Tax Calculator to accurately budget your property purchase.

Notary

In Quebec, the buyer normally hires and pays for the notary. This is because it is the notary’s job to verify that the seller has clear title (ownership) to the property and the legal right to sell it. As this is in the interest of the buyer, it makes sense that the buyer should pay for the notary. The buyer has also agreed in the promise to purchase (Clause 7.3 ) to pay the notary to prepare and register the deed of sale.

ℹ️ Note

In Quebec, the notary fee normally falls somewhere between $1,700 – $2,800. In our closing cost calculator above, we preset this figure for you.

Other types of closing cost

In addition to the common types of closing costs, there are also several other closing costs that normally show up in the transaction. These include:

Let’s take a quick look at each of these closing costs now.

Pre-purchase inspection

The pre-purchase inspection is a professional evaluation of a property’s condition. The home inspection identifies potential issues or defects before you take ownership of the property. Clause 8 of the promise to purchase lets you choose whether to have the home inspected before taking ownership.

You should get a pre-purchase inspection because if you discover a “hidden defect” after taking ownership, the seller must pay for the repair work. However, an issue qualifies as a hidden defect only if a reasonable inspection before closing could not have uncovered it.

In certain parts of Quebec, you should also order specialist tests that general home inspections do not cover. This includes tests for pyrite, asbestos, radon, and so on. Your home inspector and/or realtor may also recommend that you get tests for mould, or Iron Ochre deposits. If you skip these specialist tests, you risk paying for any repairs yourself, because issues discovered later may not qualify as hidden defects under the law.

ℹ️ Note

The average cost of a home inspection in Quebec is between $800 – $1300. The cost depends on the size of the property and if you need any specialist tests.

Consult with your realtor to find out what type of inspection you need to get.

However be aware that the OACIQ (the real-estate brokers regulator) requires that all brokers:

- Your real estate broker must recommend that you obtain at least a basic home inspection before purchasing a property.

- They must also provide the names of at least two home inspectors, although they may receive a referral fee or commission for those recommendations.

If you would prefer an independent referral, you can use Immovision’s Find a Specialist feature.

Appraisal fees

Mortgage lenders often require a home appraisal to confirm that they are not lending more than the home is worth.

Typically A Lenders will arrange the appraisal and pay for it themselves because they want you as a new client. In this case, buyers will mostly be unaware that the appraisal is happening. By contrast, B Lenders and other Alternative Lenders, usually pass the cost of the appraisal on to the borrower through their administrative fees. That being said, we would highly recommend asking your lender to waive an appraisal fee.

Find Out The Value Of Your Property In Seconds

Get a free valuation of any property in seconds so that you do not overpay for the home.

Title insurance

Every property has a title, which is the legal document proving ownership and describing the rights associated with the property. When you buy a property from someone else, the property title transfers to your name. This transfer officially makes you the new legal owner of the property.

Issues can arise with a property title. For example, there could be outstanding liens or hypothecs such as a hypothec of construction, unpaid property taxes, disputes over property boundaries, zoning law violations and so on. The notary normally flags these issues during closing. However, if the notary fails to catch problems the buyer could face legal or financial complications even after completing the sale. For this reason, many lenders will often require that a buyer gets title insurance.

ℹ️ Note

The average cost of title insurance in Quebec is between $500 – $1,200. Ask your realtor or notary if they think that you need title insurance.

Latent defect insurance

A latent defect is a “hidden issue” in a property that you could not reasonably discover at the time of purchase. These defects are usually structural or major issues that affect the safety, stability, or usability of the home and could be very expensive to repair.

Latent defect insurance is a type of coverage that protects a homebuyer (and sometimes the lender) against costs that arise from hidden defects.

In Quebec, sellers must pay for repairs caused by latent defects. However, they may not automatically accept responsibility and could decide to challenge the claim in court. In this case, latent defect insurance can help cover legal fees if disputes arise. Latent defect insurance can help cover legal fees in such disputes and also pay for repairs if the seller is unable to do so.

ℹ️ Note

The average cost of latent defect insurance in Quebec is between $350–$600. Most realtors in Quebec carry some form of latent defect insurance for their clients. However this is generally limited by time and scope.

Closing costs that are specific to some buyers

The following closing costs are specific to certain types of home buyers.

GST/QST on new or substantially renovated homes

In Quebec, you must pay a sales tax whenever you buy a newly built or substantially renovated home. The sales tax consists of a federal portion and a provincial portion. The federal portion is the Goods and Services Tax (GST), and the provincial portion is the Quebec Sales Tax (QST).

For example, if you buy a home for $400,000, you must pay 5% in GST and 9.975% in QST. This yields a combined tax rate of 14.975% which adds $59,900 to your closing costs. You or your buyers broker should have entered any GST or QST into Clause 4 of the promise to purchase.

If the property costs less than $450,000, then you may be eligible for the GST/QST new housing rebate. This allows you to claim back up to 36% of the GST paid, to a maximum rebate of $6,300. You can also claim back up to 50% of the QST paid, to a maximum rebate of $9,975.

CMHC mortgage insurance

If you plan to buy a home with less than 20% down payment, then you must take CMHC mortgage insurance. Alternatively, you are able to buy mortgage default insurance from private insurers Sagen or Canada Guaranty.

Your lender adds the insurance premium to your mortgage principal, and you repay it over the life of the mortgage through your regular mortgage payments. However you must pay only the sales tax on the insurance premium at closing. In Quebec, this includes federal sales tax and provincial sales tax.

The cost of your mortgage insurance depends the type of property, and what you plan to do with the property. It is also impacted by the amount you are borrowing (your loan-to-value ratio). To work out what your CMHC closing costs will be, you need to therefore consult the CMHC insurance premiums.

The CMHC offers Eco Improvement and Eco Plus programs that allow you to get up to 25% cash back on your insurance premium when you either buy or make energy efficient upgrades to your home.

ℹ️ Note

Use our CMHC Mortgage Default Insurance Calculator to work out what the exact cost of your CMHC insurance will be.

Property tax adjustments

If you are buying a resale home, the current owner will likely have paid property taxes for the whole year. Because of this, you will likely need to reimburse a portion of the property tax to the seller at closing. These are known as property tax adjustments and they include municipal property tax and school tax.

The notary will calculate the property tax adjustments for you and share the amount you must pay ahead of closing. You can also work this out yourself by dividing the annual property tax bill by 365 days and multiplying it by the number of days from the closing date to the end of the tax period.

💡 Free Property Tax Calculator

Buying a home in Montreal? To calculate what property taxes are due on your home, you can use our free Montreal Property Tax Calculator.

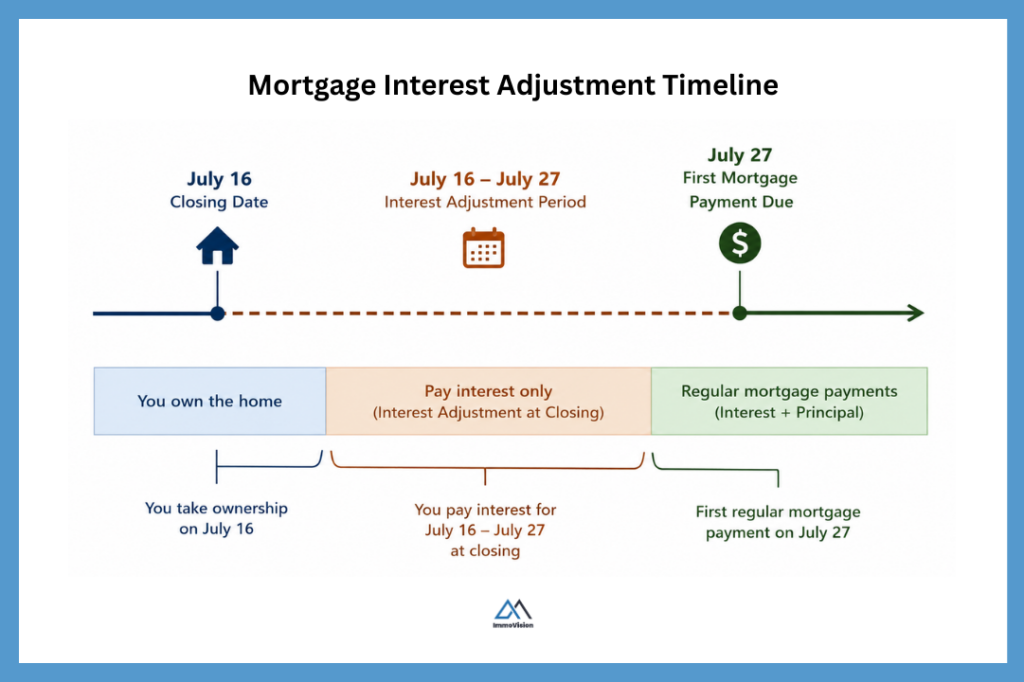

Interest rate adjustments

Unlike renting, most lenders will charge you the interest plus principal that you owe at the start of the month. This means that, unless you take ownership on the day of your first mortgage payment, you will have to pay an interest adjustment at closing. This will cover the cost of your mortgage from the days between closing and your first scheduled mortgage payment.

For example, let’s say that you buy a property on July 16th but your first mortgage payment is not due until 27th July. In this case, interest will accrue immediately, and you will need to pay the interest that accumulates between July 16th and July 27th as an interest adjustment at closing. Your first regular mortgage payment on July 27th will then cover the interest and principal from that day onward.

Other closing costs to consider

While some costs do not officially form part of your closing costs, you must still budget for them when buying a new home. These costs may include:

- Moving costs (normally somewhere between $750 – $1,500)

- Condo fees

- Expenses related to new furniture or appliances

- Home insurance

- Utilities setup (such as internet, electricity, etc.)

- Repairs and maintenance

Final remarks

Closing costs add tens of thousands of dollars to almost every property transaction. What makes them so difficult to budget for is that they are variable. They depend on the property value, the type of property, the municipality that you buy in and so on.

Most realtors will tell you to budget between 2 – 4% of your purchase price for the closing costs. However, it does help to understand what the costs since they come at different times. Knowing what to expect ensures that you don’t forget to budget for something.

Want To Reduce Your Closing Costs?

Planning to buy soon? The right real estate agent will help you calculate your total closing costs and identify rebate programs so that you can avoid overpaying for your home.