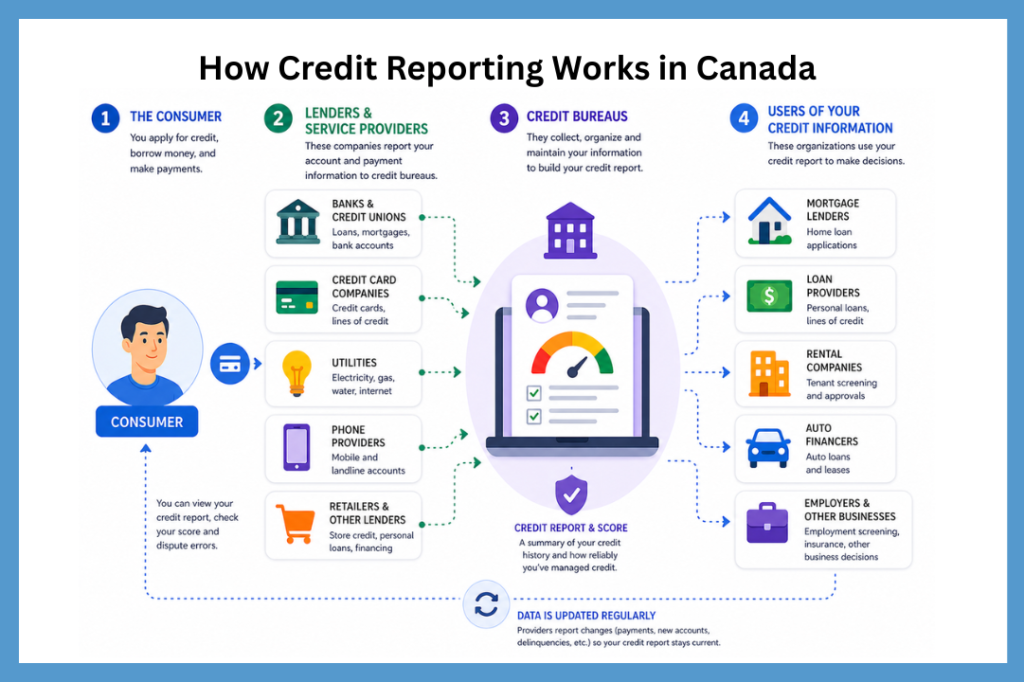

Definition of a Credit Bureau

A credit bureau is a company that collects, maintains, and reports information about your credit history to lenders and other authorized parties. There are two main credit bureaus in Canada: Equifax Canada and TransUnion Canada.

What is a Credit Bureau?

A credit bureau is a company that collects and keeps track of information about how you borrow and repay money. It will first gather data about you from lenders like banks, credit card companies, and phone providers. It then uses this data to create your credit report and credit score.

In Canada, there are two main credit bureaus: Equifax Canada and TransUnion Canada. Lenders use the information from these companies to decide whether to approve you for credit, how much to lend you, and what interest rate to offer.

For example, let’s say that you are late paying on your credit card bill, the credit card company will likely report this to at least one of the two credit bureau so that if you apply for a loan in the future, lenders can see your payment history and assess how reliably you repay your debts. They will use this information to decide on whether to approve your loan or mortgage application and on what terms.

The graphic below explains how the process works.

Who Reports to the Credit Bureaus in Canada?

Not all businesses in Canada report to the credit bureaus. For instance, some payday lenders, phone companies, gyms and many more, may not report your regular or missed payments.

In Canada, the following types of companies tend to report to the credit bureaus:

- Financial institutions like banks and credit unions

- Credit card companies, retail, and store cards

- Debt collection agencies

- Some cell phone companies, cable, and internet providers

- Student loan companies

- Public records like bankruptcy or consumer proposal

- Court-ordered judgments and registered items like a lien on a car, or a hypothec of construction

⚠️ Important

Even if a payday lender does not report a missed payment, the knowledge of your missed payment can still get to the credit bureaus.

This is because, you fail to repay a loan, the lender may charge off the debt and transfer it to a debt collection agency. The collection agency can then report the debt to credit bureaus, where it appears on your credit report as a collection account. This type of entry can lower your credit score, which is why many people try to avoid leaving debts unpaid.

Who Does Not Report To The Credit Bureaus

Many companies choose not to report to the credit bureaus. This is because it costs money, and takes effort to make it work. For small businesses such as gyms, landlords, small service providers, the cost and complexity often isn’t worth it.

The following situations tend to only report information in certain cases:

- Small and Medium Sized Businesses

- Landlords reporting late or missed rent payments

- Utility companies (gas and hydro)

- Payday loan lenders

- Unpaid provincial, federal or municipal taxes

Small and Medium Sized Businesses

Small and medium sized businesses tend not report their customers payment history to credit bureaus. This is primarily because it costs money, and takes technical effort to make it work.

To report data to a credit bureau, a business must enter into a formal reporting agreement with a credit bureau and invest in software development to integrate its systems with the bureau. Once this infrastructure is in place, the company is responsible for maintaining it, as there is a legal obligation to ensure that all reported data remains accurate and up to date. Failure to meet these requirements can result in legal liability.

That said, even if a small or medium sized business does not report payment history directly, it can transfer unpaid accounts to a collection agency. The agency can then report the debt to the credit bureaus and it will show up on your credit report.

Landlords Reporting Late or Missed Rent Payments

Landlords can report late or missed rent payments to credit bureaus, but most do not this because as with the small and medium sized businesses, it costs money, requires effort, and brings possible legal liability. As a result, many landlords choose not to report missed rent payments at all.

Landlords in Ontario, British Columbia, and Alberta, can use services like the Landlord Credit Bureau (LCB). This service acts in a similar way to a credit bureau in that landlords can submit rent payment data, which the LCB will aggregate and report to the credit bureaus. This includes both on-time payments and missed payments.

In Quebec there is no LCB and so, there are only two ways that this can get on your credit report. First, if a landlord takes legal action for unpaid rent and obtains a judgment through the Tribunal administratif du logement (TAL), that record becomes public. Alternatively, if the landlord sells the debt to a collection agency, then the agency can register this debt as a collection.

ℹ️ Note

Even though most landlords do not send details of missed payments to credit bureaus, most will run a credit check on you before renting to you.

Utility Companies (Gas and Hydro)

Large utility providers like Hydro-Québec generally do not report regular payment history. This is because they enforce billing through service interruption and collections rather than credit reporting.

Unlike a credit card issuer, which can limit your access to future borrowing, a utility provider has direct control over an essential service. In cases of non-payment, they can suspend service which causes an immediate and disruptive than a typical credit account.

Payday Loan Lenders

Payday lenders are more likely than most service providers to report directly to credit bureaus. Many payday loan companies report both the opening of the loan and your repayment behaviour, including missed or late payments.

Because payday loans are short-term and high-risk credit products, even small missed payments or defaults can be reported quickly. If the debt goes unpaid, it is also commonly sent to collections, which will further impact your credit report.

Unpaid Provincial, Federal or Municipal Taxes

Neither the Canada Revenue Agency, or provincial tax authorities, such as Revenu Québec, will report unpaid tax to a credit bureau.

The one exception to this is if you owe a very large amount of tax and make no effort to pay it back at all. In this case, tax authorities will likely involve their collections departments. They can then get a court judgement against you for the debt and this will show up in the legal section of your credit report.

The same applies to any late property taxes, or land transfer duties that you might owe to the municipality as a homeowner. However, in Quebec, continued non-payment can lead to the municipality to pass the debt to collections and register a legal hypothec (a lien—a legal claim against your property for the amount you owe) against your property. The hypothec will show up in the Quebec Land Register, it may affect your credit, and it will have to be paid anyway when you sell, as the notary will identify and settle it from the proceeds.

ℹ️ Note

There’s no fixed rule about which companies report to credit bureaus. However, and in general, if you pay for services upfront, like a Netflix subscription, while those billed after use may be. However, even the company does not report to the credit bureau, the debt can still appear on your credit report if the company sends it to collections or becomes a court judgment.

As such it is best to pay what you owe, since this helps avoid long-term credit damage and makes life simpler.

What Information Do Credit Bureaus Report On?

Credit bureaus collect data to assess how likely you are to repay a debt. They do not focus on how much money you earn or how much you have in the bank, because those factors do not reliably predict repayment behavior. For instance, even individuals with significant wealth sometimes fail to repay their debts.

Instead, credit bureaus focus on data that helps them predict whether you will actually repay what you legally owe. The credit bureau chooses this data by analyzing millions of real-world credit records and identifying patterns in the data that consistently correlate with repayment behavior. This includes:

- Personal information: Identifiers such as your name, address history, date of birth, and employment information. The credit bureau uses this data to verify your identity and match your credit file to you accurately.

- Trade credit lines (your accounts with lenders): A list of your accounts with lenders, including credit cards, loans, and other credit products. Each entry shows the account balance, limits, payment history, and account status. From this, credit bureaus and lenders can see whether an account is in good standing or marked with ratings such as R (revolving), I (instalment), or in delinquent / default status (e.g., R9).

- Credit inquiries: A list of times that a lender has checked your credit. This includes both hard inquiries (credit applications) and soft inquiries (background or account reviews). Hard inquiries are when you apply for credit. Credit bureau’s have found that hard inquiries are indicative of potential lending risk, especially if there are many within a short period. For this reason, hard inquiries can hurt your credit score, whereas soft inquiries do not.

- Public records and collections: Financial events such as accounts sent to collections, along with certain legal records like bankruptcies, consumer proposals, and court judgments (where applicable). The bureau uses this information show serious credit events.

Notable Exclusions: What Information Do Credit Bureaus Not Report On?

Credit bureaus do not report on every financial transaction throughout your life. This is because, they consider certain types of data to be either non-predictive of repayment behaviour or restricted by law. This includes:

Data That Is Older Than 5 – 7 Years

In Canada, credit bureaus generally do not report information that is between 5–7 years old. The exact timeframe depends on provincial laws and the type of data. In Quebec, the Act respecting the protection of personal information in the private sector limits how long most negative information can remain on your credit report (often around 6–7 years, depending on the item). In Ontario, similar timelines come from the Consumer Reporting Act.

| Type of Data | Quebec (approx.) | Ontario (approx.) |

|---|---|---|

| Late payments | 6 years | 6 years |

| Collections | 6 years | 6 years |

| Bankruptcy (first) | 6–7 years | 6–7 years |

| Hard inquiries | 3 years | 3 years |

Note

You can ask a credit bureau to remove data that a company reports after the deadline. Borrowers commonly do this as part of improving or cleaning up a credit report.

Data On Foreign Debt

Canadian credit bureaus generally do not report on foreign debt. For example, if you have a loan from a European bank that does not operate outside of its home country or region, that debt will typically not appear on your Canadian credit report.

The only exception to this is if a lender operates in multiple countries and shares data internally. For instance, if you borrow money from RBC in the UK, RBC in Canada will likely know if you have missed payments or defaulted on your account. A lender may also request that you share a credit report from a foreign country with them before approving a loan.

In the end, there is no automatic global credit reporting system. Credit systems remain largely country-specific.

Unreported Data

Even within a single country, the data reported can vary. A business that shares data with one credit bureau may choose not to share it with others. For instance, many payday lenders will only report negative information (such as missed payments or defaults), or report exclusively to a single credit bureau rather than both.

To find out whether a business you work with reports to a credit bureau (and to understand their policies around collections), review their terms and conditions, credit agreements, or privacy policy disclosures.

Data On Personal Income

Credit bureaus do not use data on personal income, your job status, or your assets or savings to determine your likelihood of repaying debt. This is because these factors are not consistently reliable predictors of repayment behavior.

However, lenders still care about this information. When you apply for credit, lenders often ask for your income and employment details because they are assessing affordability. That is, if you can reasonably handle new debt payments.

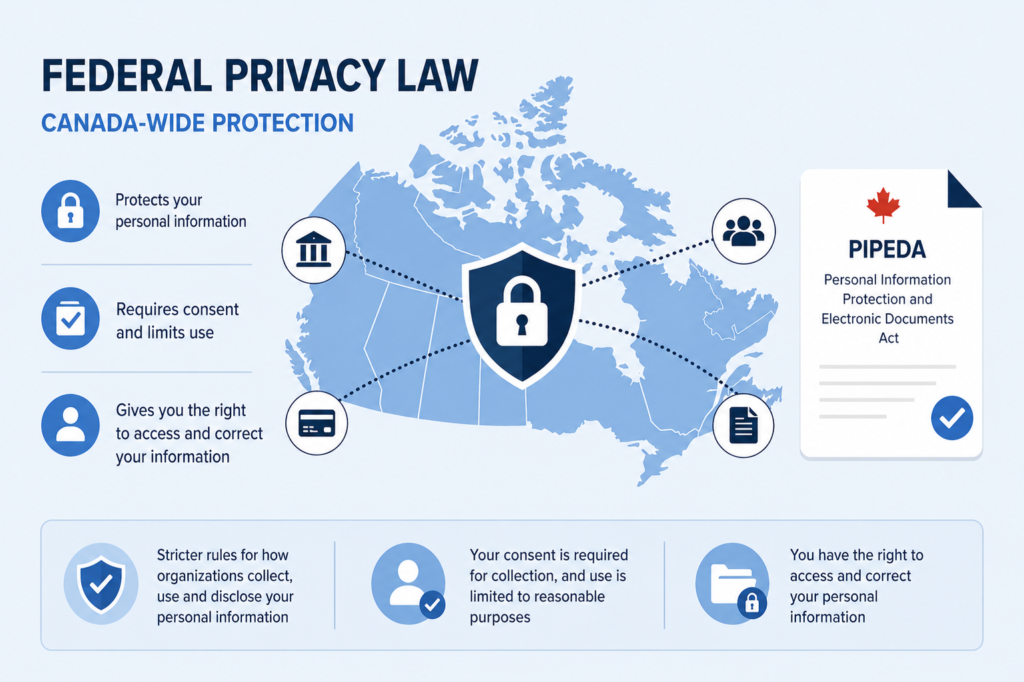

Who Do Credit Bureaus Work For And Who Regulates Them?

Credit bureaus sell credit reports to lenders such as banks, credit unions, and credit card companies. Their role is to act as independent data providers, supplying information that lenders use to assess risk.

They cannot fabricate data, share your information freely, or report inaccurate details. Instead, they must follow strict privacy laws at both the federal and provincial levels.

At the federal level, this includes the Personal Information Protection and Electronic Documents Act (PIPEDA), which governs how private-sector organizations collect, use, and disclose personal information. It requires consent, limits use to reasonable purposes, and gives individuals the right to access and correct their data.

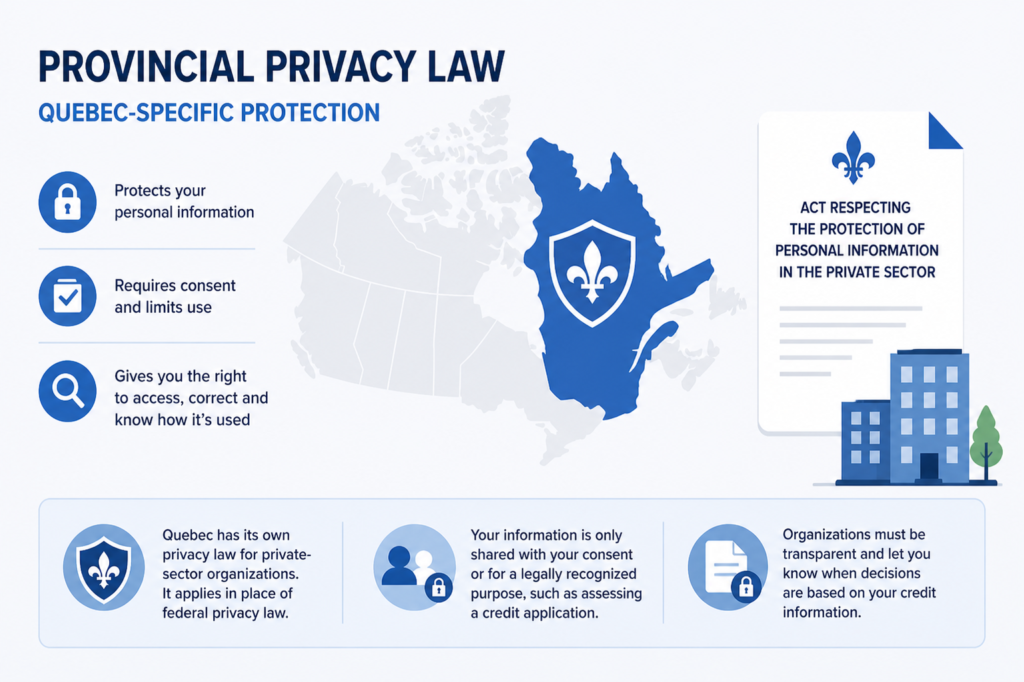

For example, in Quebec, private-sector organizations follow the Act respecting the protection of personal information in the private sector instead of the federal Personal Information Protection and Electronic Documents Act. These laws limit access to your credit information to parties with your consent or a legally recognized purpose, such as assessing a credit application, and require organizations to inform you when decisions are based on that information. For example, if a bank denies a mortgage application based on your credit report, they must tell you that this is because of your credit score.

Frequently Asked Questions

Are Credit Karma, Mogo, Borrowell, or Clear Score Credit Bureaus?

No. In Canada, there are only two official credit bureaus: Equifax Canada and TransUnion Canada.

Companies like Credit Karma, Borrowell, ClearScore, and Mogo are not credit bureaus. Instead, they are credit monitoring or financial services platforms. They work by pulling your credit data directly from Equifax or TransUnion and displaying it to you in a simplified dashboard. In most cases, they do not add new credit data or replace your official credit report.

Their main value is providing free access to your credit score and monitoring tools, but they often also promote credit products such as loans or credit cards based on your profile.

Do Landlords Report Rent Payments to Credit Bureaus?

No. Most landlords in Canada do not report rent payments to credit bureaus.

Rent reporting is optional and usually requires a third-party service. Some landlords may choose to report through platforms or credit-building services, but it is not common practice. In most cases, rent only appears on your credit report if:

- The landlord sends unpaid rent to a collection agency, or

- The landlord takes legal action and obtains a court judgment

Otherwise, on-time rent payments typically do not appear on your credit file.

Why are There Only Two Main Credit Bureaus in Canada?

Canada has only two main credit bureaus: Equifax Canada and TransUnion Canada.

This exists largely due to market structure and history. Both companies originated in the United States and expanded into Canada early on, establishing nationwide systems for collecting and distributing credit data.

Over time, they became the dominant credit reporting networks because:

- Lenders standardized reporting through them

- Building new nationwide credit infrastructure is expensive and complex

- The system benefits from consistency across lenders and provinces

As a result, nearly all Canadian lenders report to one or both of these bureaus, and they remain the central sources for consumer credit information in Canada.

Final Remarks

Your credit report is one of the most important financial records you have in Canada. It is an ongoing record of your financial behaviour, and how likley you are to repay your debts.

However, sometimes things happen and you don’t even realize it, like a small debt you forget to pay, mistaken identity, or even fraud on your account. These small issues can grow into bigger problems if they go unnoticed, and they can affect your ability to get approved for loans, mortgages, or even rental applications.

This is why it’s a good idea to regularly check your credit report. It gives you the best chance to improve your credit score, correct errors early, and spot potential fraud before it becomes a serious issue. It also helps you understand exactly what lenders see when they review your file, so you can take steps to strengthen it when needed.

👉 You can check your credit report for free @ LoansCanada, Canada’s most trusted loan comparison platform.