Dividing a home and other family assets during a separation or divorce can feel overwhelming. The good news is, Quebec’s family patrimony rules provide a framework to ensure property is divided fairly. Understanding how it works, step by step, can help you feel more in control during an emotionally difficult time. In this article we cover:

- What is family patrimony?

- What property is included in family patrimony

- What is not include in family patrimony

- Your rights and obligations concerning the family residence

- How to calculate and divide family patrimony

- Working with a realtor during a divorce

- Frequently asked questions

- Final remarks

What is family patrimony?

Family patrimony is a legal concept in Quebec that requires certain family assets to be divided equally between spouses when a marriage or civil union ends, whether through divorce or death.

Family patrimony does not include all assets, but it generally covers the family home, secondary residences, household furnishings, vehicles used by the family, and pension or RRSPs accumulated during the marriage. Quebec law automatically applies family patrimony to married couples and civil unions, and couples cannot waive it in advance except in very limited circumstances. Section 414 of the Civil Code of Quebec sets this out.

What property is included in family patrimony?

Family patrimony generally includes:

- Residences used by the family, this include all residences e.g. primary and secondary residences.

- Household furniture used by the family e.g. furniture, appliances, electronics, artwork.

- Motor vehicles used for family transportation, this includes all motor vehicles e.g. cars, boats, recreational vehicle’s (RVs).

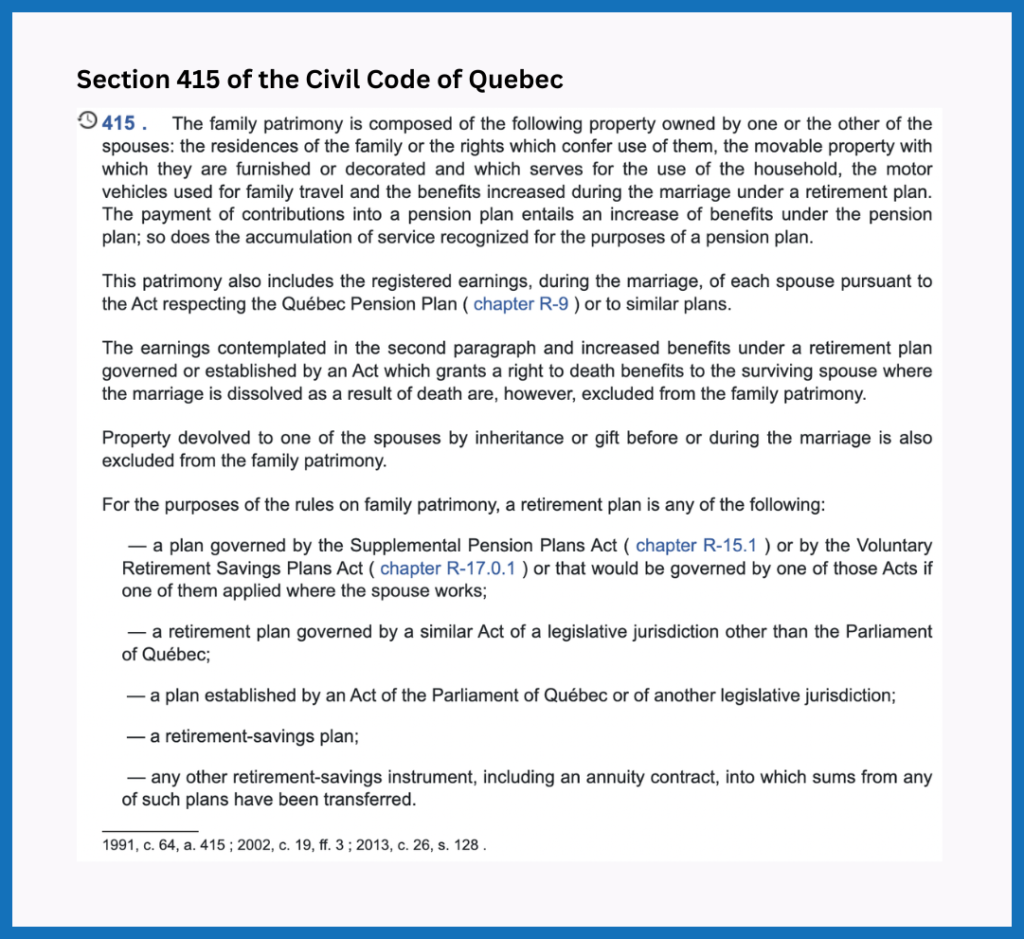

- Benefits accrued during the marriage under pension or retirement plans e.g. RRSP and pension funds.

Section 415 of the Civil Code of Quebec sets this out.

What is not included in family patrimony

Family patrimony does not include the following property:

- Personal property

- Property that was a gift

- A business or farm

- Cash and bank accounts

- Savings, bonds,

Your rights and obligations concerning the family residence

The family residence is often the most valuable asset in a marriage. Quebec law calculates the family patrimony share of your home based on when you purchased it, how you own it, whether you have a mortgage, and how you financed it. The outcome is highly fact-specific and depends on proof. Below are some of the more common scenarios that can come up.

1. Sole Ownership vs. Joint Ownership

If both spouses are on the property title, then the family residence is part of the family patrimony. In this case, the law will normally divide the home equally between the two spouse. However, if you are the sole owner of your house or condominium, it may still be part of the family patrimony if it served as a family home.

This is because, when you married or formed your civil union, your domicile became your family residence and became subject to the rights that protect the family residence.

Note: Legal ownership and family patrimony rights are not the same thing.

2. Timing of the Purchase (Before or During Marriage)

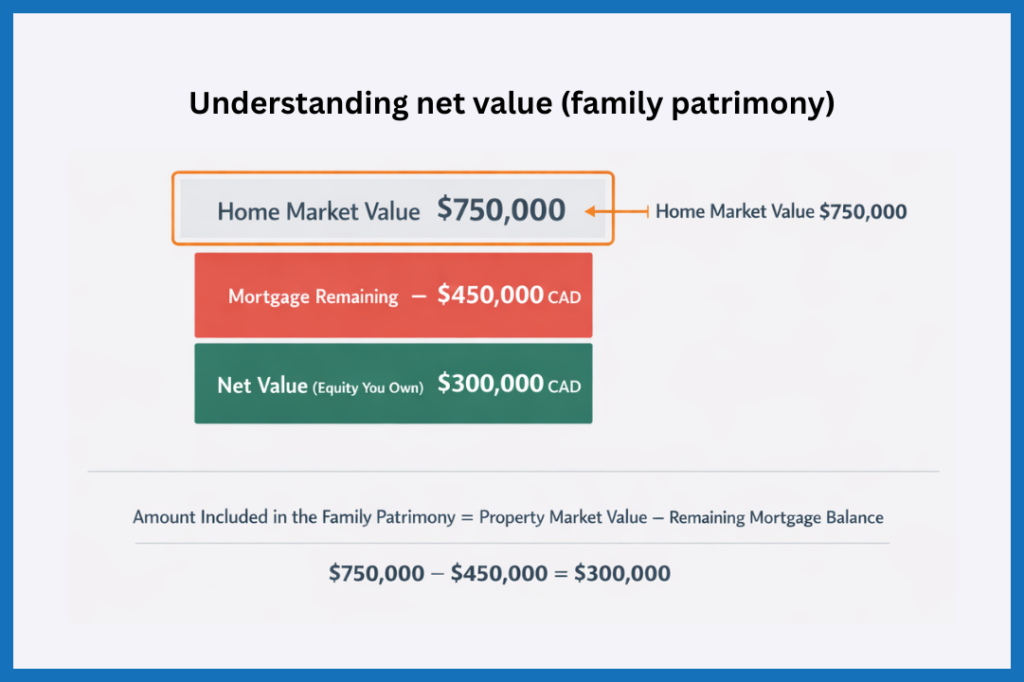

If the one of both of the spouses bought the family home during the marriage, the law will usually include the net value in the family patrimony. Net value in this context means the amount of the home you actually own. Quebec law calculates net value by taking the home’s current market value and subtracting any remaining mortgage or debts secured against it.

For example, imagine your family home has a current market value of $750,000, and you still owe $450,000 on the mortgage. The family patrimony then includes the $300,000 of equity, and you and your spouse each receive half after you sell the home.

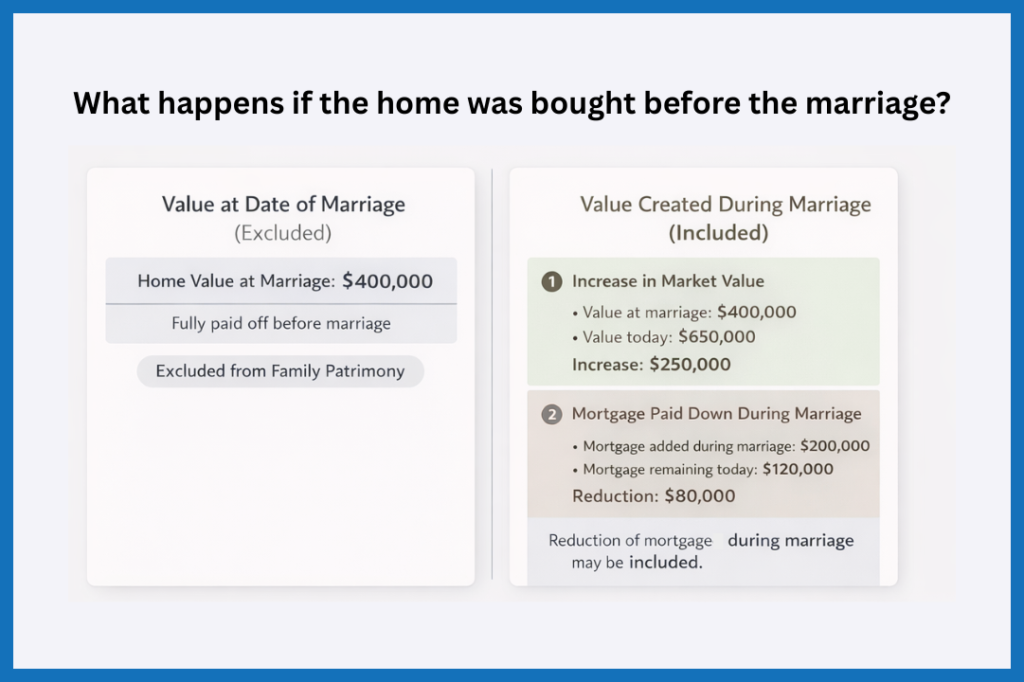

By contrast, if you purchased the home before marriage and fully paid it off, Quebec law typically excludes its net value at the date of marriage from the family patrimony.

However, the law still includes any increase in the home’s value during the marriage. If you re-mortgaged the home at any point, the payments that reduce the mortgage during the marriage may also count toward the family patrimony.

Note

3. Inheritance and gifted funds

If one spouse inherits a property or receives it as a gift, the law generally excludes that property from the family patrimony. The same rule applies to money gifted to one spouse, including a gifted downpayment used to purchase a home.

The spouse who claims that property or funds are excluded must prove their origin. This includes money received as a gift and used for renovations that increased the home’s value. If the spouse cannot clearly trace and prove where the funds came from, the court may refuse to exclude them from the family patrimony.

4. Investments and improvements to the property

Under Quebec law, you must include any renovations that increase the value of your home in the family patrimony. The important factor is not how much money you spend, but how much the improvements actually raise the property’s value. Lawyers and judges often hire an expert realtor or professional home appraisal to determine how much value your renovations added.

** Important Note **

How to calculate and divide the family patrimony?

In this section we go through one example to help you understand the basic rules for dividing the family patrimony.

Example – How to calculate and divide family property in Quebec

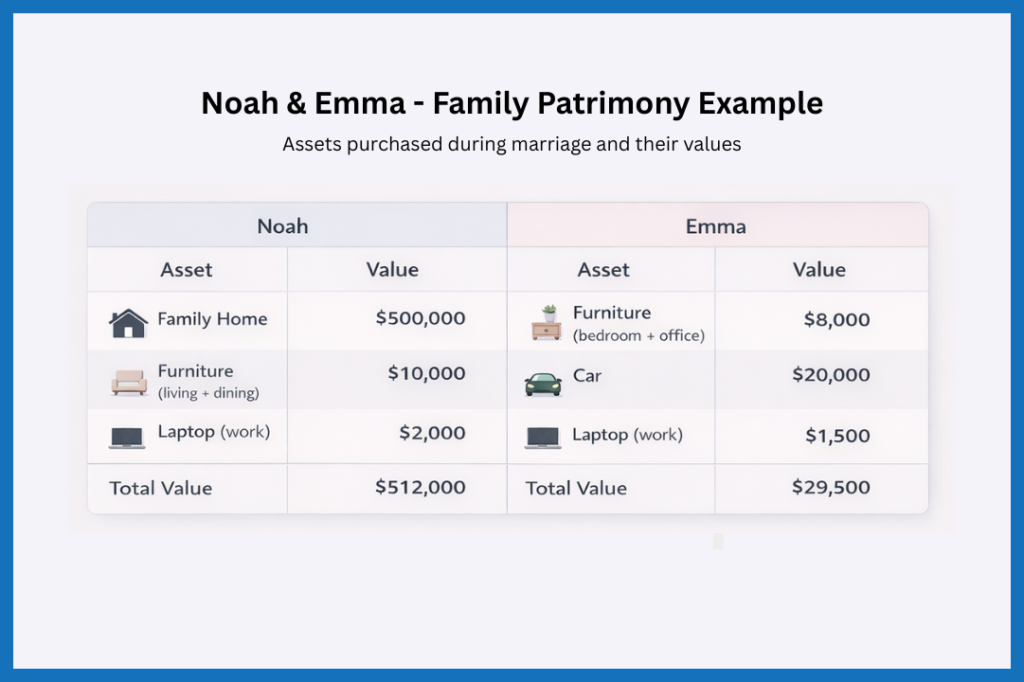

Noah and Emma are going to get divorced. They own the following property, which they bought while they were married:

The value of the family patrimony is calculated in the following steps:

- Identify which property is included in the family patrimony.

- Calculate the net value of the included property.

- Account for any amounts that should be subtracted (e.g., gifts, prior exclusions).

- Determine how the property’s value will be divided based on ownership and contributions.

- Decide on a method for payment or distribution.

1. Identify which property is included in the family patrimony

Noah and Anne will include the family home, furniture and car in the family patrimony.

2. Calculate the net value of the included property

- Family home: $500,000 – $150,000 (outstanding mortgage) = $350,000 = net value of the family home

- Car: $20,000 – $0 (no debts) = $15,000 = net value of car

- Furniture: $18,000 – $0 (no debts) = $18,000 = net value of furniture

3. Account for any amounts that should be subtracted (e.g., gifts, prior exclusions)

In this case there are no other amounts to subtract.

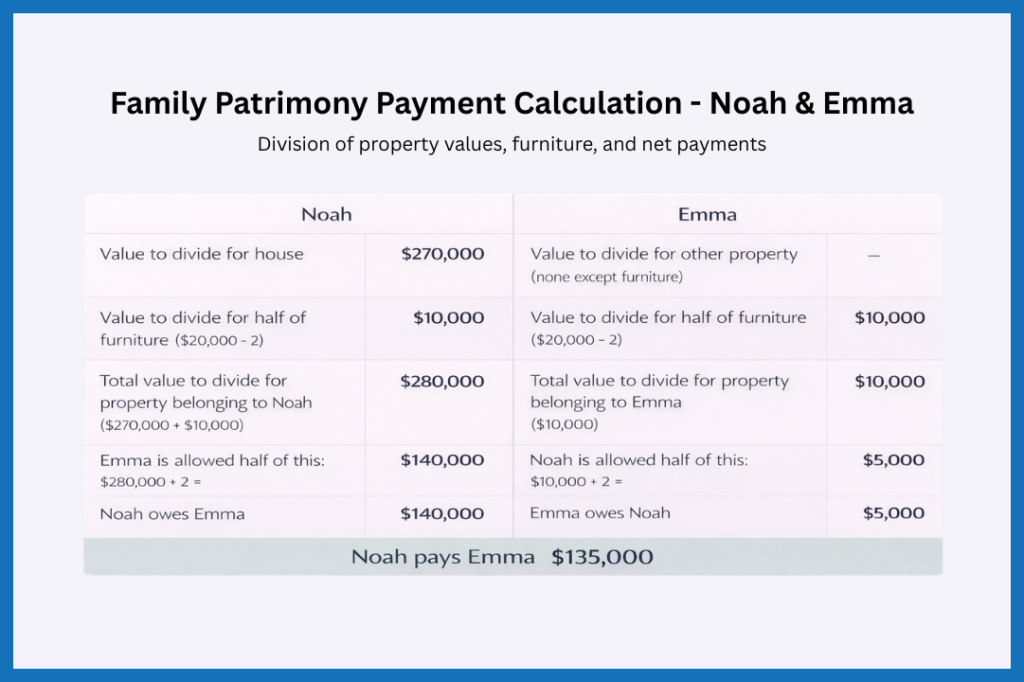

4. Determine how the property’s value will be divided based on ownership and contributions

The table below shows how the properties value will be divided.

5. Decide on a method for payment or distribution

The final step is to decide on a method for payment.

Since Noah owes $135,000 to Emma, Noah has a couple of options.

- Noah can pay cash to Emma, if he has the money.

- Noah can transfer his assets to Emma to settle the debt. In this case, if Noah transfers the house to Emma, Emma would owe Noah $135,000 for the account difference.

- Noah can sell the family home and use the proceeds to compensate Emma.

Working with a realtor during a divorce

You can engage a real estate agent once both spouses agree to sell the home, or if a court order permits the sale. Although many couples getting a divorce will request hire their own agents, you do not need two separate agents and if you do have two seperate agents, this can create conflicts. The key here is that the realtor cannot work to sell the home if any listing requires the consent of all owners or a legal mandate.

What a realtor can and cannot do

A realtor cannot provide legal advice, but they can help you take steps to protect yourself. For example, if your spouse is not a co-owner of the property, you can file a declaration of family residence. This informs third parties that the home cannot be sold without consent, protecting you from unilateral action.

Role of the realtor in the process

Realtors who know how to handle the sale of a family home in a divorce are normally very experienced. In addition to the usual role that the realtor takes on, the realtor will also:

- Give good recommendations for family lawyers that they have worked with in the past.

- Act as a point of contact for lawyers if there is disagreement on the sale price.

- Negotiate with a home appraisers who may come back with a lower valuation on the property.

- Help implement interim agreements, such as a pre-approved list price, or pre-approved terms for acceptance.

- Respect the emotional and practical challenges of the situation. Divorce sales can be particularly difficult when children are involved. The realtor should handle the process sensitively so that children do not associate the sale or loss of the family home with one parent’s “fault”.

Frequently asked questions

This can lead to long delays, sometimes more than three years, before the house can be sold and the proceeds divided. This is because the parent staying in the home has little incentive to agree to sell quickly and give up time with the children. However, if no agreement is reached, the court may ultimately order the sale of the home, unless one parent can prove a valid reason to delay or prevent it.

– Lump-sum payment: Sometimes the other spouse can make a one-time payment to help you retain the home.

– Spousal support: A fixed or indexed payment can provide guaranteed income to cover mortgage or living costs.

– Division of RRSPs or other assets: Part of your retirement or investment savings can be used to generate cash.

It’s important to understand your rights and options in your specific situation. A lawyer specializing in family law can help you determine the best way to access cash or structure payments to maintain the home or transition fairly.

Final remarks

While the rules of family patrimony provide a clear legal framework, every situation is unique. You can make the process smoother and protect your financial and emotional interests by keeping good records, understanding your rights, and working with experienced professionals such as family lawyers, realtors, and appraisers.