Credit Report Definition

Your credit report is a summary of your credit history.

In Canada, your credit report shows:

- Basic details to used to identify you

- A list of your credit accounts (like credit cards, loans, or lines of credit)

- A record of who has looked at your credit report

- More serious financial issues, like accounts sent to collections or legal records related to debt.

What is a credit report?

Your credit report is a summary of your credit history. It shows how you’ve used borrowed money over the past 5–7 years. This includes things like your loans, credit cards, and whether you’ve paid them back on time.

Lenders use your credit report to assess how likely you are to repay your debts, based on your past borrowing and repayment behavior. Your report does not take into account how much money you have in the bank or your net worth. Instead, it focuses on your track record of on time debt repayments. This is because, even people with high incomes or assets can miss payments.

✨ Note

Your report is typically several pages long, depending on how many credit accounts you’ve had, how often you’ve applied for credit, and whether you have any collections or public records.

Why is your credit report important?

Your credit report matters because it helps lenders and other organizations judge how reliable you are with money.

If you have a history of paying your debts on time, lenders record that behaviour on your credit report, which makes them more likely to approve your applications and offer you lower interest rates.If your report shows missed payments or accounts in collections, lenders may decline your application or charge you higher interest rates because they see you as a higher risk. This means that you could end up paying more than your peers to borrow the same amount of money.

Beyond lending, insurers, landlords, employers, and utility providers may also check your credit report to decide whether you are likely to meet your financial obligations. If your report shows that you have a bad history with credit, landlords may be less willing to rent to you, insurers may charge higher premiums, and utility providers might require a deposit before setting up service.

For all these reasons, you should aim to keep your credit report in good shape since this can make a meaningful difference in your financial options and costs over time.

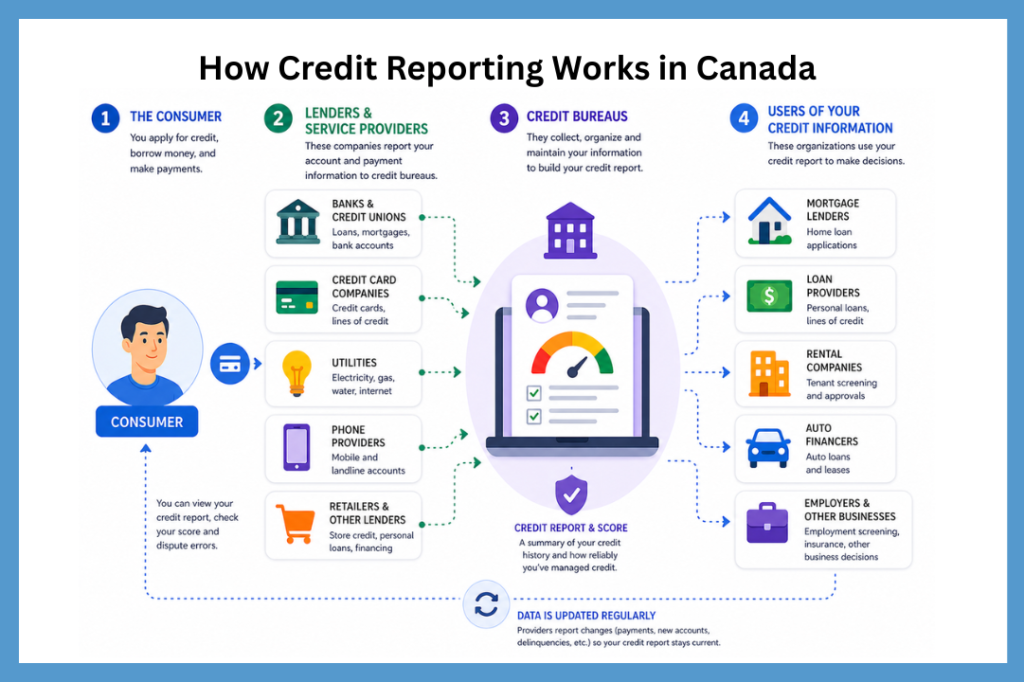

Where does the credit report come from?

In Canada, one of two credit bureaus prepares your credit report: Equifax or TransUnion. These are private companies that specialize in collecting, storing, and reporting on the credit history of Canadian citizens.

Canadian businesses (like banks, credit card companies, and lenders) regularly send information about how you borrow and repay money to the credit bureaus. The credit bureaus then extract key details—such as your balances, payment history, and account status—and compile this into a credit report. Lenders will then use the report to decide whether to approve your application and what interest rate or terms to offer you.

✨ Note

Not all businesses report to both credit bureaus, and some don’t report at all. This means that different credit bureaus may show slightly different information on your credit report, depending on which lenders report to them.

What information is on your credit report?

The information in your credit report, will depend on which credit bureau creates your report. However, in general, there are four main sections to your credit report. These are:

Let’s look at what information the credit bureau typically includes in each case.

✨ Note

Your credit report summarizes all of your borrowing and repayment activity into a single three-digit number between 300–900. We call this your “credit score“. More on this later.

Personal Information

This part of your credit report is there to identify who the report belongs to. In Canada, this information includes:

- Name

- Address

- Date of birth

- SIN number

- Employment status

- Current employment status

- Past employment status.

Lenders and credit bureaus use basic personal details to match credit information to the correct individual. Although the bureaus have designed this system to be reliable, mistakes and fraud happen all the time. This is why it is so important to check your credit report regularly.

When you review you review your credit report regualarly, you can catch issues early. For instance, a loan or collection account that does not belong to you. You can then take steps to correct the issue before they become harder to resolve over time.

Checking your credit report regularly helps you catch errors early.If you find a loan or collection that doesn’t belong to you, you can fix the error more easily before too much time passes and companies lose, misplace, or delete old records.

Check Your Credit Report (For Free)

Get a free credit report in minutes with LoansCanada—Canada’s most trusted comparison platform.

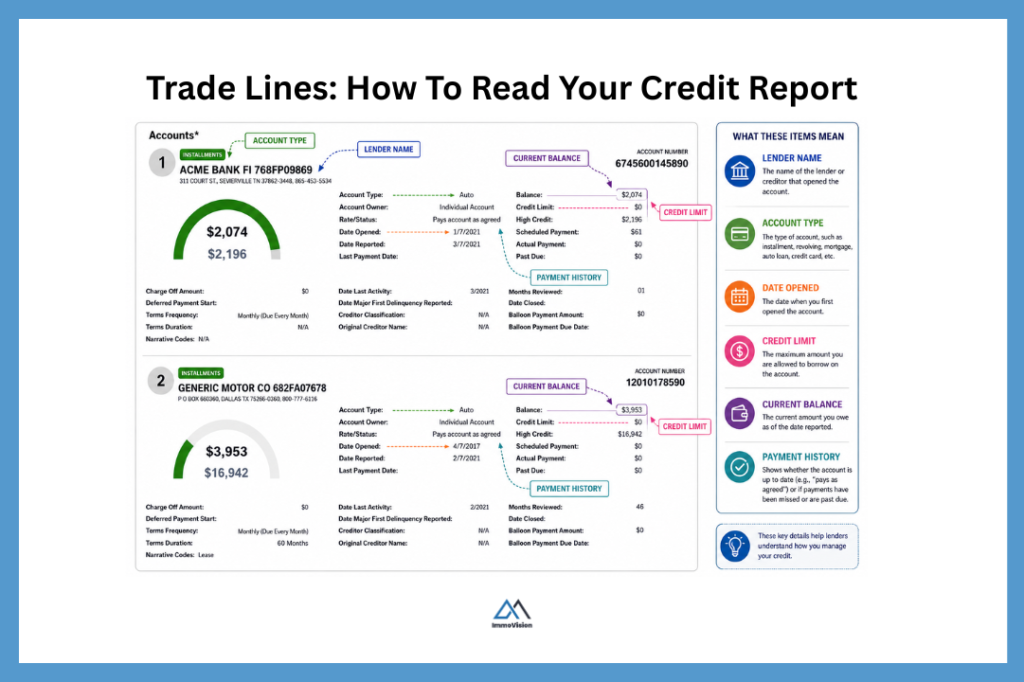

Trade lines

Creditor trade lines are a list of accounts that you have with your lenders. For example, you might have a credit card, mortgage, and car loan. In this case you would have three creditor trade lines. The trade lines will include:

- The name of the lender

- The type of account (e.g. revolving, installment, or mortgage)

- The date you opened the account

- What your credit limit is

- Your current account balance

- Your payment history (e.g. whether you are up to date or have missed any payments)

The screenshot below shows how this looks on the Equifax sample report.

Inquiry information

A soft inquiry is a check of your credit report that is not related to a credit application (for example, when you check your own credit or a company does a background check). This type of inquiry does not impact your credit score or your ability to borrow.

By contrast, a lender makes a hard inquiry when you apply for credit. This hard inquiry, which is a request for more information about your credit history, tells the credit bureau that you are actively seeking new credit. A hard inquiry does impact your credit report since it can slightly lower your credit score and signals potential increased borrowing risk.

For instance, imagine that you decide to use credit to finance several things within a short time frame. This can make you appear riskier to lenders, as it suggests you may be taking on too much debt at once or relying heavily on credit, which can lower your credit score and affect your credit profile.

✨ Note

Hard inquiries can remain on your credit report for up to 3 years and too many hard hits (more than 5–6 in 12 months) can impact your credit score and ability to borrow.

Public records and collection information

In this part of your credit report, the credit bureaus record legal actions, along with debts that have gone into default or that have been sent to collections. This includes:

Bankruptcies

In Canada, bankruptcy is a legal process designed to protect you from your creditors while you deal with your debts. While bankruptcy law is the same across Canada, credit reporting rules can vary slightly by province.

In Quebec, and in the case of a first-time bankruptcy, it will generally remain on your credit report for 6–7 years after discharge. Discharge simply means from the point that you are no longer legally required to repay the debts that are included in your bankruptcy. A second bankruptcy remains on your credit report for about 14 years after discharge.

Consumer proposals

In a consumer proposal, you agree to pay back part (or sometimes all) of your debt over a period of up to 5 years, and in exchange, creditors agree to forgive the remaining balance. Once you and the creditor agree a proposal, the creditor can no longer take legal action against you, and interest on the debts stops.

A consumer proposal will appear on your credit report and typically remains there for 3 years after completion (or up to 6 years from filing, whichever comes first).

Judgements

Judgments are court orders that confirm you owe a debt and require you to repay it. These rules depend on provincial laws that govern civil procedure and debt enforcement, such as the Civil Code of Québec in Quebec.

For example, if you owe a significant amount of property tax to your municipality, they can obtain a judgement against you. This means that they will sue you for the amount owed (the unpaid property tax). If the court orders you to pay the debt, this result will show up on your credit report.

Similarly, if you renovated your home and didn’t pay the contractors, they might register a lien against your home. In Quebec, we call this a construction hypothec. The law allows the contractor to register the lien in the Quebec Land Register. This will make it hard for you to sell you home however, to enforce their claim, the contractor must obtain a judgement. If this happens, the judgement will show up on your credit report.

✨ Note

Failure to pay a debt after receiving a court order will lead to enforcement actions such as wage garnishment, seizure of assets, or additional legal consequences.

Collections

Collections are debts that have not been paid and have been transferred or sold to a collection agency after a period of non-payment.

If you fail to make payments on a debt (such as a credit card or loan), the creditor may eventually send the account to a collection agency. This will be recorded on your credit report and signals that the debt is seriously delinquent.

A collection account can significantly impact your credit score and will generally remain on your credit report for about 6 years from the date of last activity (such as your last payment).

Even if the debt is paid, the record of the collection may still remain on your credit report for that period, although it may be marked as “paid.”

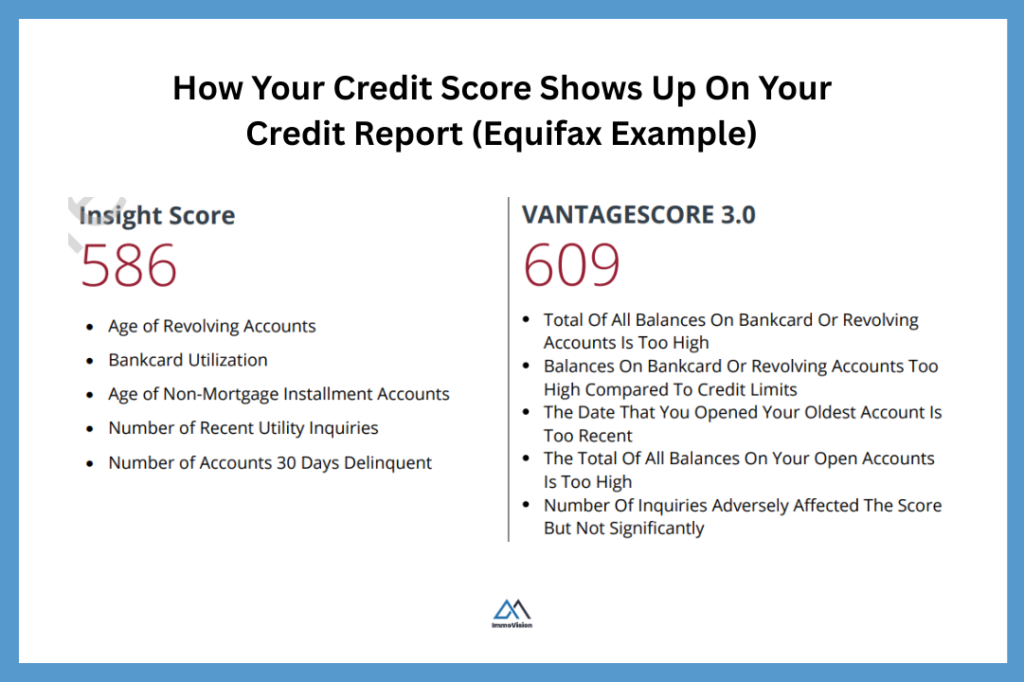

What is your credit score?

The credit bureau uses all the data on your credit report to compute a credit score. This is a 3 digit number between 300-900 that summarizes your likelihood of repaying borrowed money on time and in full. Your credit score is one of the most important figures lenders use to assess your application for credit and determine the terms they offer.

Both Equifax and TransUnion use two different methods to calculate your credit score. Equifax uses ses the FICO scoring model as well as its own proprietary Equifax Risk Score. TransUnion uses the VantageScore model as well as its own proprietary TransUnion Risk Score. Both bureaus may report the results of these different scoring models on your credit report.

Below is an example of how this looks on the Equifax credit report.

Notice that the score also includes clear reasons explaining why the borrower received that score. Credit bureaus provide these explanations to show what are the key factors that influenced the result. This gives you insights into what is affecting your credit score and how you can improve your credit score.

For more information on how credit score works, read Credit Score Explained: What It Is, How It Works & Proven Ways to Improve Yours in Canada.

What information is on not on your credit report?

Early credit reports included subjective character assessments, and even marital status. However, over time the credit bureaus refined credit reports as they have learned which factors best predict whether someone will repay their debts on time and in full.

Today, credit reports still exclude many types of information that people might assume are relevant, but that don’t meaningfully improve how well lenders can assess credit risk. These are:

Debts that are older than 5-7 years

Canada’s federal and provincial laws limit how long credit bureaus can keep certain types of information on your credit report. The exact timeframe depends on the type of data, and the province where you live.

In Quebec, the Act respecting the protection of personal information in the private sector implies that:

- The credit bureau can only collect your personal information for the purpose of running your credit score (s.4 of the Act).

- The credit bureau can only use the information for the reason they collected it (or closely related reasons) (s.12 of the Act).

These laws work together to mean that once the original reason for collecting personal data is no longer valid, an organization no longer has a legal basis to keep it. In other words, if credit bureaus no longer need certain information to assess your creditworthiness or calculate your credit score, they must remove it from your file. The table below gives common examples used by Equifax and TransUnion.

| Type of Information | Equifax | TransUnion |

|---|---|---|

| Late payments | ~6 years from the date of delinquency | ~6 years from the date of delinquency |

| Collections | ~6 years from the date of last activity or assignment | ~6 years from the date of last activity or assignment |

| Bankruptcy (first filing) | ~6 years from discharge | ~6–7 years from discharge |

| Hard inquiries | ~3 years | ~6 years |

✨ Note

If credit bureaus keep data on your credit report longer than necessary (according to their own reporting policies), you can contact the bureau and request that delete it.

Foreign debts

Equifax and TransUnion do not generally report on foreign debt. For example, if you have a loan from a American bank, that does not operate outside of the United States, that debt will typically not show up on your Canadian credit report.

The only exception to this is when a lender operates in multiple countries and shares data internally. For instance, if you borrow money from American Express in the United States, American Express in Canada will likely know if you have missed payments or defaulted on your account. A lender may also ask you to provide a credit report from another country before approving a loan.

However, ultimately, there is no automatic global credit reporting system. Credit systems remain largely country-specific.

Unreported data

Even within a country, not all businesses report to credit bureaus. For example, some payday lenders do not report to both bureaus, and many small or mid-sized businesses lack the systems or incentives to report customer data consistently.

Because of this, a credit report can only include information that the bureaus actually receive. If a company doesn’t report your account, it won’t appear on your report—at least initially.

However, unpaid debts can still end up on your credit report later. If a lender stops reporting an account but you fail to repay it, they may transfer or sell the debt to a collection agency. When this happens, the account may not appear as a regular trade line, but it can still show up under collections.

Note

Ideally, you want to avoid missed payments altogether. But if you do miss a payment and it escalates, the same debt can appear in multiple sections of your report:

- As a late payment under trade lines

- As a collection account if it is sent to collections

- And, in more serious cases, as a judgment under public records

This kind of “triple impact” from a single debt can significantly lower your credit score. The good news is that this situation is often avoidable if you communicate with your lender or resolve the debt before it escalates to collections or legal action.

Data on net worth

Perhaps surprisingly, credit reports do not include any information about the individuals net worth. This means that even if you have millions of dollars in assets, including cash, property, cars, and so on, you might still have poor credit. Essentially this is because, wealth, in and of itself, is not a good predictor of a persons reliability when it comes to repaying their debts.

All that being said, when you apply for credit, lenders do care about your net worth, as well as your sources of income. This is because they are want to assess affordability. That is, if you can reasonably handle new debt payments.

How to fix a mistake on your credit report?

According to Canadian federal law, credit bureaus must ensure that the information on your credit report is accurate. This means that if you spot a mistake on your credit report that is negatively impacting your ability to borrow money on good terms, you can contact the credit bureau and inform them of the error.

It is best to do this well in advance of when you need to borrow money, because fixing errors can take time, and investigations are not instant. If you leave it until the last minute, lenders may review your credit report before the credit bureau corrects the error and offer you less favourable terms

To fix a mistake on your credit report, you need to take the following steps.

Step 1. Identify the mistake

First, you will need to request a copy of your credit report. You can do this using a platform like Loans Canada, or you can ask the lender to send the detailed report to you. Once you have the report, you will then need to look over the report and identify where the mistake is. The most common mistakes on a credit report are:

- Inaccurate personal details:

- Incorrect account information:

- Fraudulent accounts:

- Uncorrected negative information:

Step 2. Gather evidence

Once you have identified the error, the next step is to gather evidence. Depending on the mistake you must will need to write a clear explanation of the mistake, and how this shows up on your credit report. For any claim that you make, you need to provide proof.

For instance, let’s say that you paid an outstanding credit card bill 6 months ago, but it is still showing up on your credit report as unpaid. In this case, you will need to contact the lender and ask them to update their records and report the correct payment status to the credit bureaus. If the lender agrees that they have made a mistake, you use this as evidence to share with the credit bureau.

Step 3. Contact the credit bureau

Once you have gathered your evidence, the next step is to identify which credit bureau is reporting the incorrect information. From there, you can follow the credit bureau’s procedure for filing a dispute online.

Below is the process for filing a dispute with TransUnion Canada and Equifax Canada.

Transunion Canada

English: 1-800-663-9980

French: 1-877-713-3393 or 514-335-0374

TransUnion Consumer Relations

P.O. Box 338, LCD1

Hamilton, ON L8L 7W2

Equifax Canada

Equifax Canada Co.

Consumer Relations Department

Box 190, Jean Talon Station

Montreal, QC H1S 2Z2

Step 4. Wait for a response

The credit bureau will review your dispute and carry out an investigation, which may include contacting the lender or creditor that supplied the information.

If the lender confirms there has been an error, the credit bureau may update or remove the incorrect entry from your credit report. However, if the lender verifies that the information is accurate, the entry will remain on your report without any changes.

Frequently asked questions

How to check credit report in Canada?

To check your credit report in Canada, you can visit either Equifax or TransUnion, create an account, and request access to your credit report (and in some cases your credit score).

Alternatively, you can use a free third party platform like Loans Canada, which provides a free estimate of your credit score and shows information based on data from both credit bureaus.

How to check credit report for fraud?

To check your credit report for fraud, you should regularly review it for accounts or activity you don’t recognize, such as credit cards you didn’t open, loans you didn’t apply for, or inquiries from lenders you’ve never dealt with. You can request your report from Equifax and TransUnion and compare all listed accounts and activity against your own records. If you spot anything suspicious, you should report it immediately and place a fraud alert or credit freeze.

How to check credit report for errors?

To check your credit report for errors, you should carefully review all personal details, accounts, balances, and payment histories on your report. Look for incorrect late payments, outdated balances, closed accounts still shown as open, or any information that doesn’t match your records. You can access your report through Equifax or TransUnion, and if you find mistakes, you should file a dispute so the credit bureau can investigate and correct the information.

Final remarks

Your credit report plays a central role in your financial life in Canada. It affects lenders’ decisions on whether to approve your credit applications, the interest rates they offer you. It also affects landlords decision to let you rent, insurance premiums, and whether some service providers or employers consider you financially reliable.

The key takeaway is simple: your credit report is not something to check once and forget. It is a living record that changes over time as you borrow, repay, and interact with lenders. By reviewing it regularly, you can spot errors, catch signs of fraud, and understand what is helping (or hurting) your credit profile.

To stay on top of your credit, check your credit report for free with platforms like Loans Canada and review it regularly for any changes or errors.