Your offer isn’t just a form you fill out once you’ve found the right home. It’s an iron-clad, legally binding contract for one of the largest financial decisions you’ll ever make. Whatever, you agree to in this document, can become enforceable by law and, breaking the agreement can create significant financial penalties or even legal action.

If you agree to buy a home for $700,000 and later discover, through inspection, that there are serious issues—mould, asbestos, radon—your ability to walk away or renegotiate a lower price depends on the conditions that were included in the offer.

The question is: are you buying a great home at a fair price or is the seller’s agent the one in control?

In this article, we cover:

- What is a promise to purchase?

- What goes into a promise to purchase?

- Inside the Promise to Purchase: The 16 key sections explained

- Top things to watch out for

- How to negotiate your promise to purchase like a pro

Need Help Preparing Your Offer? (It's Usually Free)

An experienced buyer’s broker doesn’t just negotiate the price—they save you thousands by negotiating repair credits, price drops after home inspections, inclusions, and seller-paid closing costs.

Use Immovision AI to find a top-rated, local buyer’s agent in seconds. It’s usually free.

What is a promise to purchase in Quebec?

In Quebec, a promise to purchase (sometimes called an offer to purchase) is the formal way that a home buyer makes an offer to a home seller. In short, it is a contract that sets out the price, conditions and timeline for buying a property.

Since the promise to purchase is a contract, this means that once the seller receives the promise to purchase it is legally binding. As such, a buyer cannot back out of the contract once the seller receives the offer, unless the seller fails to fulfill a condition in the promise to purchase.

What goes into a promise to purchase?

In Quebec, the promise to purchase is a template document provided by the OACIQ. This is the regulatory authority that oversees real estate brokers and agencies. There are different different templates depending on the type of property. For example, the OACIQ offers one template for divided versus undivided co-ownerships and another for residential buildings with fewer than five units that do not belong to a co-ownership.

Below are some examples of promise to purchase templates with links to the official downloadable versions:

- Residential property with fewer than five units (not a condo) Download PDF

- Condo (divided co-ownership) Download PDF

- Undivided co-ownership (shared ownership) Download PDF

- Immovable / general property Download PDF

- Property sold by the Public Curator Download PDF

Whilst there are different templates, each document follows the same legal structure.

💡 The top 6 things to focus on

Looking for a summary of the promise to purchase? Read about the 6 top things to check in your promise to purchase.

Inside the Promise to Purchase: The 16 key sections explained

Below you’ll find the 16 standard sections of a promise to purchase, along with a brief explanation of what each section covers. Once you understand what these mean, you will be able to use the promise to purchase as a negotiation tool.

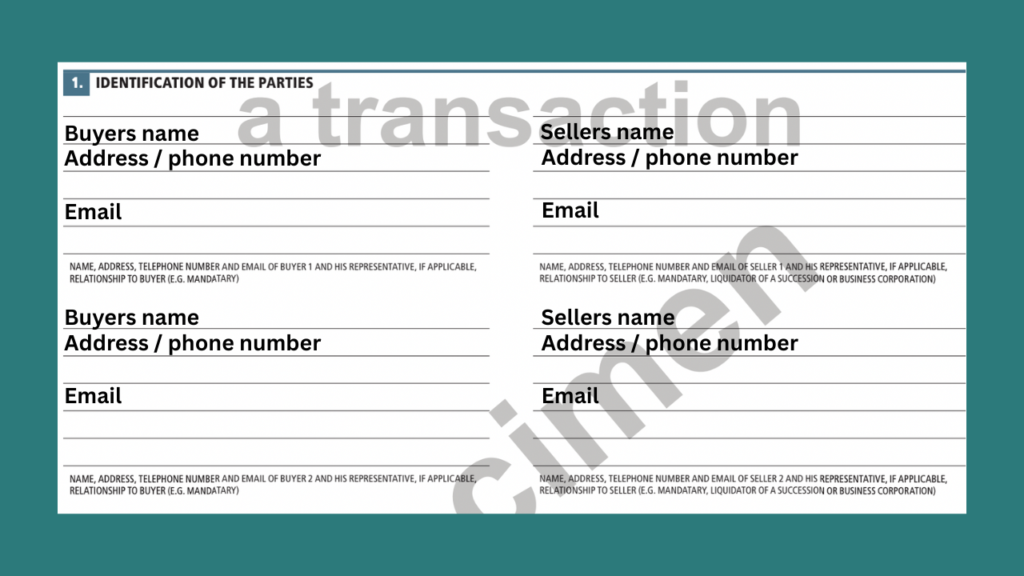

1. Identification of the parties

This section lists the buyer’s and seller’s legal names and contact information. This confirms who the contract binds. There may be multiple buyers and sellers. If this is the case you need to list out all parties in the transaction.

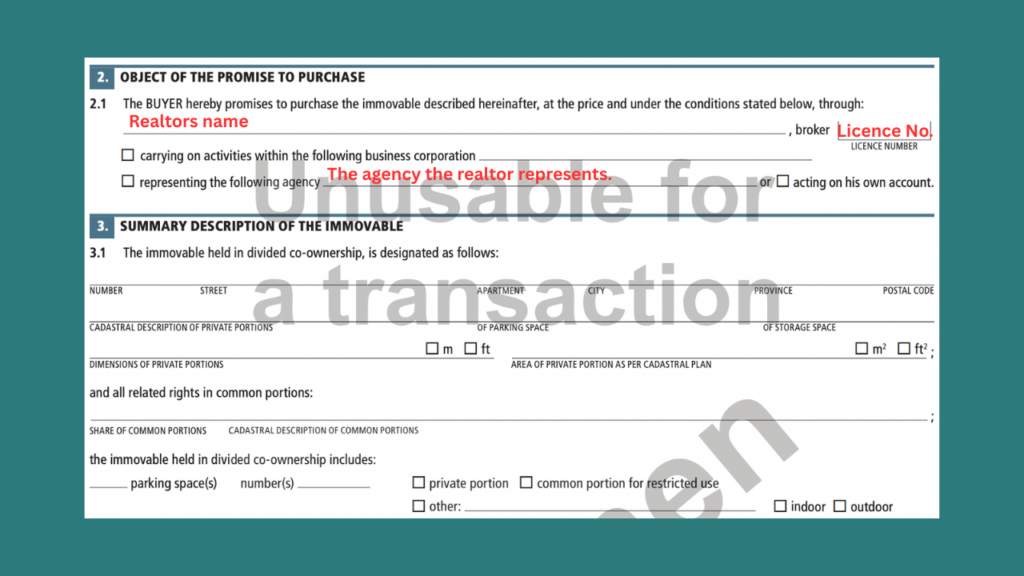

2. Object of the promise to purchase

The second part of the promise to purchase is where you write who your real-estate agent is. Their name, licence number, the name of their corporation, agency or if they are working alone.

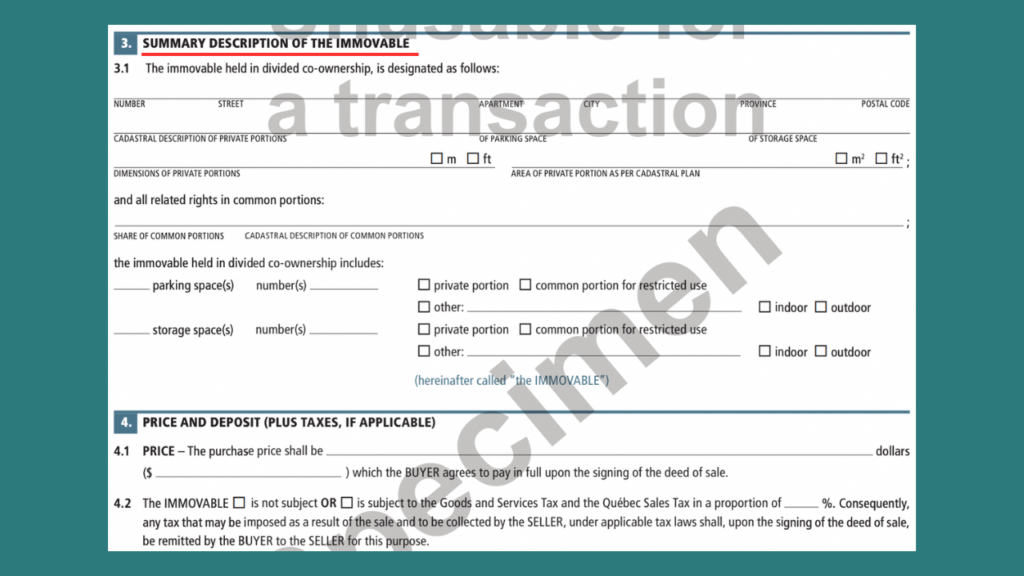

3. Summary of the immovable

The immovable is the type of property (e.g. condo, townhouse, duplex) and its key characteristics such as parking spaces, storage or private land area. All of the land in Quebec is divided into lots and each lot has its own lot number, also known as a cadastral number. To ensure that you are offering to buy the correct property, you should check the cadastral number and the cadastral description in the Quebec Land Register.

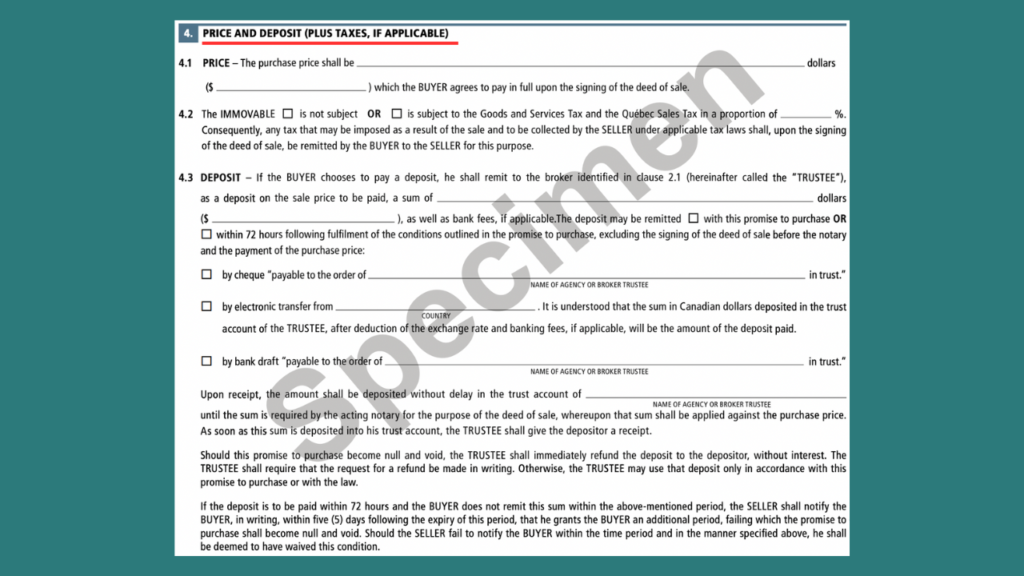

4. Price and deposit (plus taxes if applicable)

Clause 4 states the price that you want to offer to buy the property, the deposit amount and whether taxes (GST/QST) apply.

Deposits are not mandatory however they can be a tool to help make your offer stand out if there are multiple buyers offering to buy the same home. If the buyer decides to offer a deposit, then the statement here is that the buyer provides a deposit in “good faith”, and the real estate agency or broker holds it in trust.

Regarding taxes, it is worth noting that the federal and provincial governments in Canada charge taxes on new or substantially renovated properties (GST and QST respectively). You will input any taxes on the property at this point. You may be able to claim back part of these taxes after you complete the purchase via the GST/QST New Housing Rebate in Quebec.

⚠️ Do You Know The Fair Market Value Of Your Home?

The list price is just the seller’s asking price. It doesn’t necessarily reflect the property’s fair market value.

Before submitting an offer, your real estate broker should be preparing a Comparative Market Analysis (CMA) to determine what similar homes have recently sold for and whether the property is priced fairly.

If you don’t have access to a CMA, use our free Home Value Estimator to get an independent estimate and avoid overpaying, or connect with a realtor using our Agent Finder tool and order a free CMA.

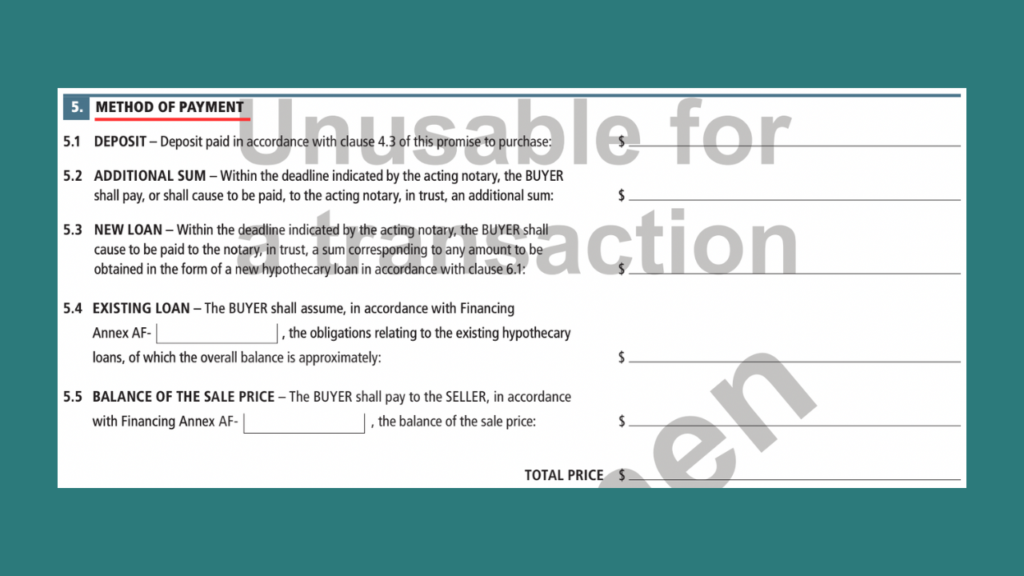

5. Method of payment

Section 5 of the promise to purchase explains how the buyer will pay for the property. For example, the deposit amount, the size of the downpayment, through a mortgage and/or using funds from the sale of another property.

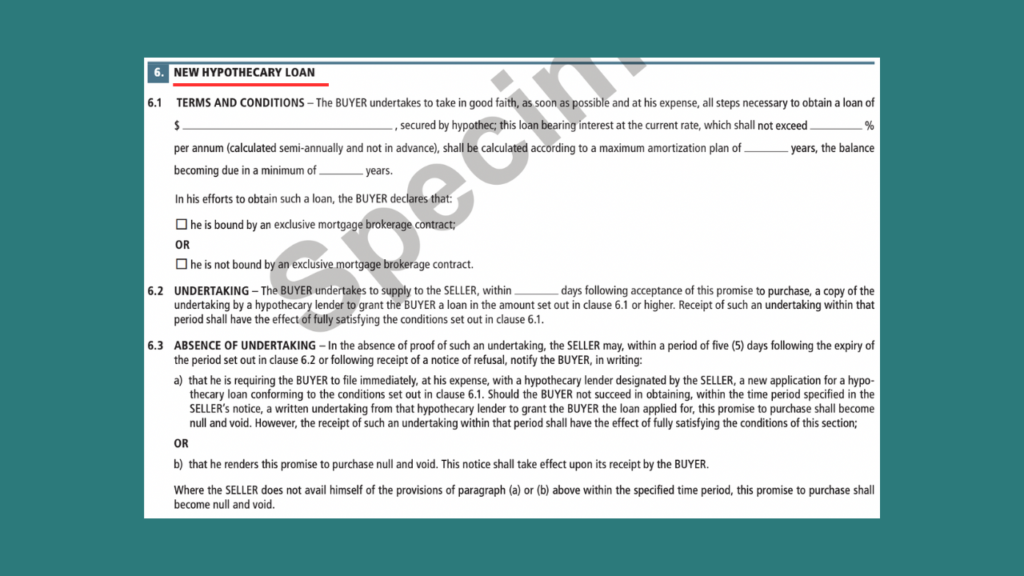

6. New hypothecary loan

In Section 6, you outline the terms of the mortgage you are applying for. This includes the amount you intend to borrow, the interest rate, and the mortgage length and term. You can also indicate how much flexibility you are willing to allow for these terms. For example, if a lender pre-approves you at 3.5%, you can set a slightly higher rate, such as 4%. This allows you to satisfy your financing condition if rates rise before you finalize your mortgage.

You also make a commitment to complete your mortgage and obtain and share a written loan commitment from a mortgage lender with the seller. Once the seller receives this commitment, the financing condition is satisfied. However, if you fail to provide the loan commitment within the deadline, the seller may either:

- Require you to obtain financing from another lender. If another lender is willing to provide financing that meets the terms set out in the promise to purchase, you may be required to proceed with that financing.

- Cancel the transaction. The seller can notify you in writing that the financing condition has not been satisfied and declare the promise to purchase null and void. Depending on the circumstances, you could lose your deposit and may be held responsible for damages suffered by the seller.

⚠️ Always Set Financing Conditions

Even if you have been pre-approved for your mortgage, a lender can still deny your mortgage at closing. If this happens, you will need to look for an alternative lender and, this could mean that you are forced to accept a rate that is higher than you initially budgeted for. This is why including a financing condition in your Promise to Purchase is so important—it provides protection if your mortgage approval does not proceed as expected.

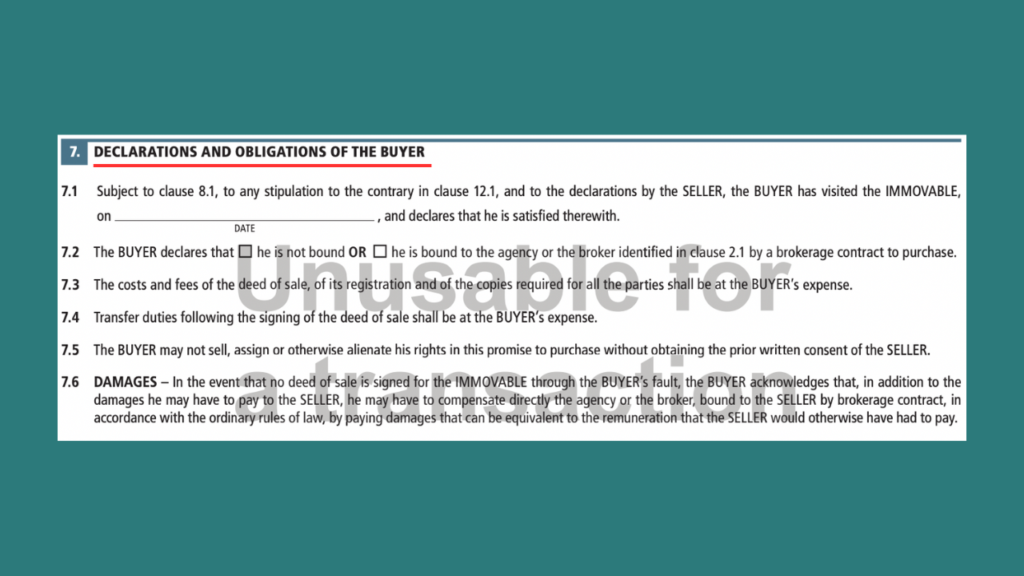

7. Declaration and obligation of the buyer

In Section 7, the buyer makes a series of declarations that they affirm are true and for which they take full responsibility. These include confirming that they visited the property on a specified date, which ensures that the seller will transfer the property in the same condition it was in on that day. The buyer also declares that, to the best of their knowledge, no law (such as bankruptcy restrictions), contract, or court decision prevents them from completing the transaction.

Next, the buyer agrees to cover the notary’s fees for organizing the closing, preparing the deed of sale, and registering the transaction with the appropriate land registry. They further commit to paying any transfer duties, such as the land transfer tax (known colloquially as the welcome tax), and to attend the signing of the deed of sale on time.

Additionally, the buyer irrevocably promises not to sell, transfer, or assign any rights or obligations under the promise to purchase and acknowledges that only they are responsible for fulfilling the agreement.

Finally, the buyer recognizes that failing to fulfill any obligation under this promise may entitle the seller to claim damages. This may include retaining the deposit and seeking additional compensation to cover any losses or expenses resulting from the buyer’s non-compliance.

💡 Closing Costs

The costs that you agree to pay here are part of your closing costs. Learn more about closing costs in our article: The complete guide to closing costs for buyers in Quebec real-estate (2026).

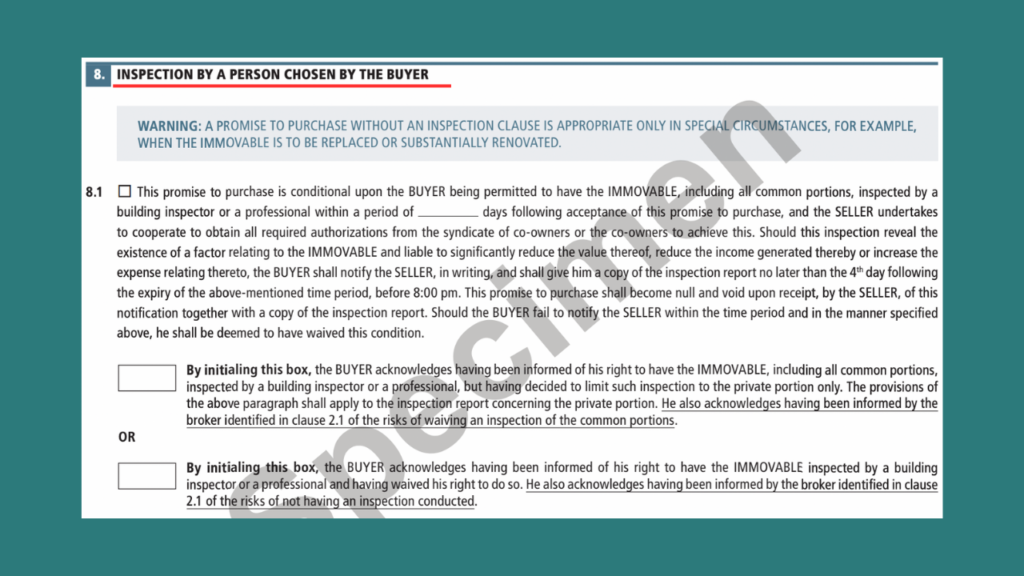

8. Inspection by a person chosen by the buyer

This section gives the buyer the right to have the property inspected by a qualified professional within a specified timeframe. It is essential to hire an experienced inspector to evaluate the property thoroughly because, once you purchase the home, the responsibility for repairing any defects generally falls on you.

A professional inspector can also advise you on the appropriate tests to conduct for specific risks such as pyrite issues or other structural concerns. While a seller may be responsible for defects that the inspector should have detected but missed in their report, it is still the buyer’s responsibility to order the right inspections.

You can make your offer conditional on satisfactory inspection results. Buyers and their brokers often refer to this as the “pre-inspection clause”. Many inexperienced buyers think of the pre-inspection clause as a “global way out” of the deal. However, this is not actually the case. In fact, you can only utilize the inspection clause to withdraw your offer if the inspection uncovers a significant problem that has not been disclosed in the Seller’s Declaration; minor issues or cosmetic defects do not justify cancelling the purchase. Major normally means one problem that is cost at least 3% of the purchase price.

⚠️ What If You Want To Inspect A Known Issue?

If you want to inspect an issue that the seller has declared, for example a crack in the foundation, or a sump pump that hasn’t been inspected for 20 years, you must explicitly mention this in your promise to purchase.

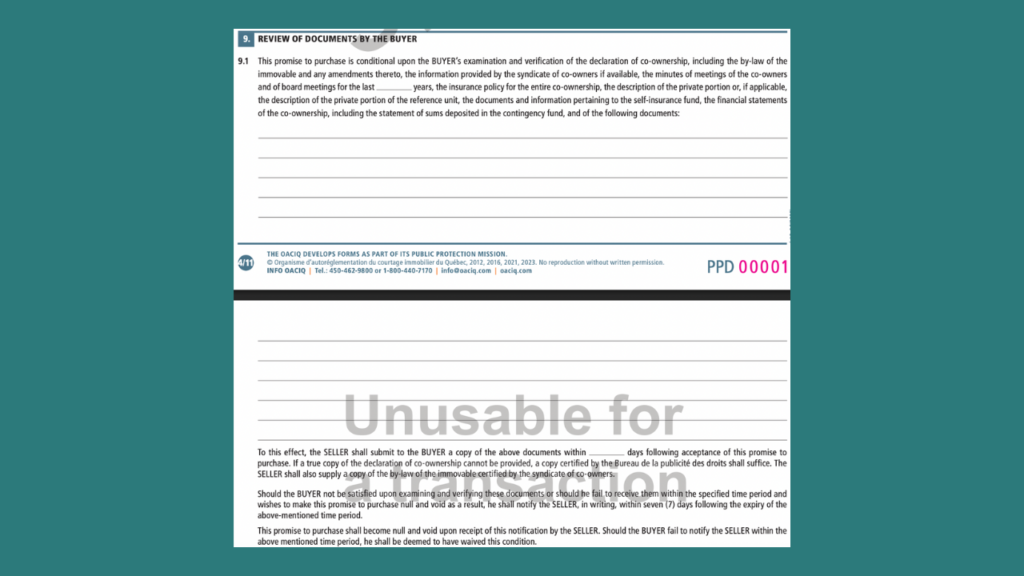

9. Review of the documents by the buyer

In this section, we outline which of the documents we want to receive from the seller in order to review before the final decision to buy. The buyer and their broker are allowed to review these documents to their “complete satisfaction”. This is super interesting, because it gives you a window into the seller’s disclosures, the condition of the property, and any potential issues that could affect your decision to proceed.

Buyers should request items such as heating bills, records of any construction work (to confirm it was done legally), the certificate of location and verification of any warranties or guarantees provided by the seller. If you are buying into a co-ownership (i.e., a condo), you should also review the declaration of co-ownership, meeting minutes, the status of the reserve (condo) fund, documentation required under Bill 141, and the maintenance log.

We also outline the timeline for this process: the seller will have a set number of days to provide the requested documents, and the buyer will have seven days from receipt to review them thoroughly.

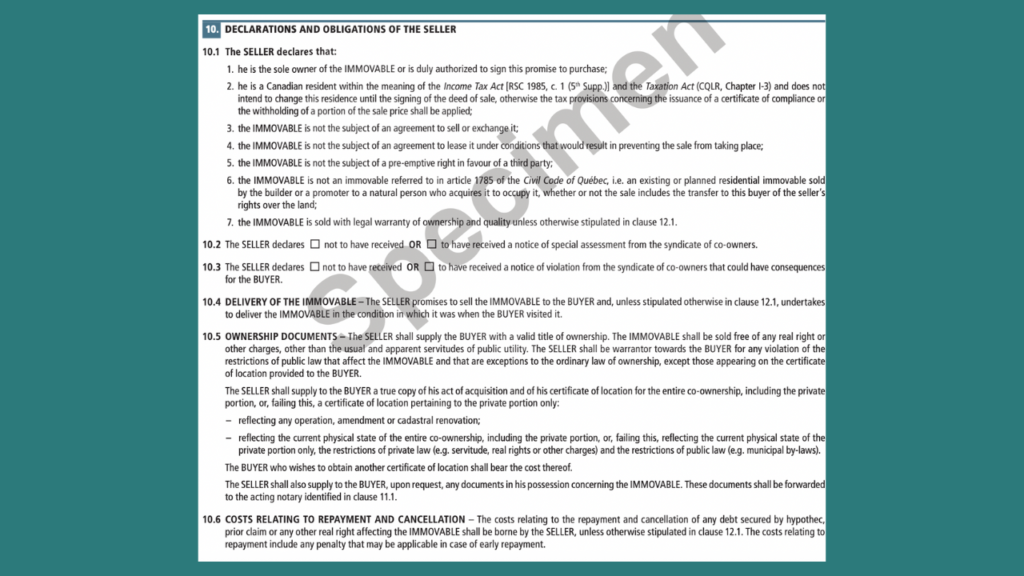

10. Declaration and obligations of the seller

Section 10 covers the declarations made by the seller. These are promises about the property’s condition and legal status, carefully chosen by the OACIQ to give you confidence in proceeding with the purchase. For example, the seller declares that they are the sole owner of the property, that there are no known liens or encumbrances on the property, including construction hypothecs, outstanding property taxes, or other claims that could affect ownership.

The seller also discloses any expected significant expenses, confirming that they will deliver the property in the same condition you visited it in, transfer the property title to you, and make several other commitments that ensure the transaction proceeds smoothly and securely.

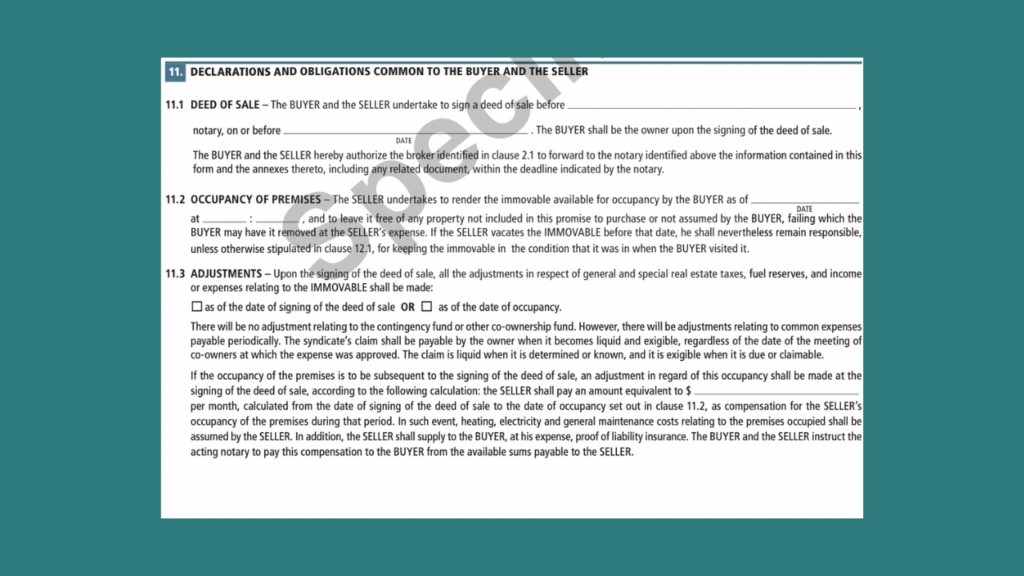

11. Declarations and obligations common to the buyer and seller

Section 11 covers mutual obligations, like cooperating with the notary, respecting timelines, and signing all necessary paperwork.

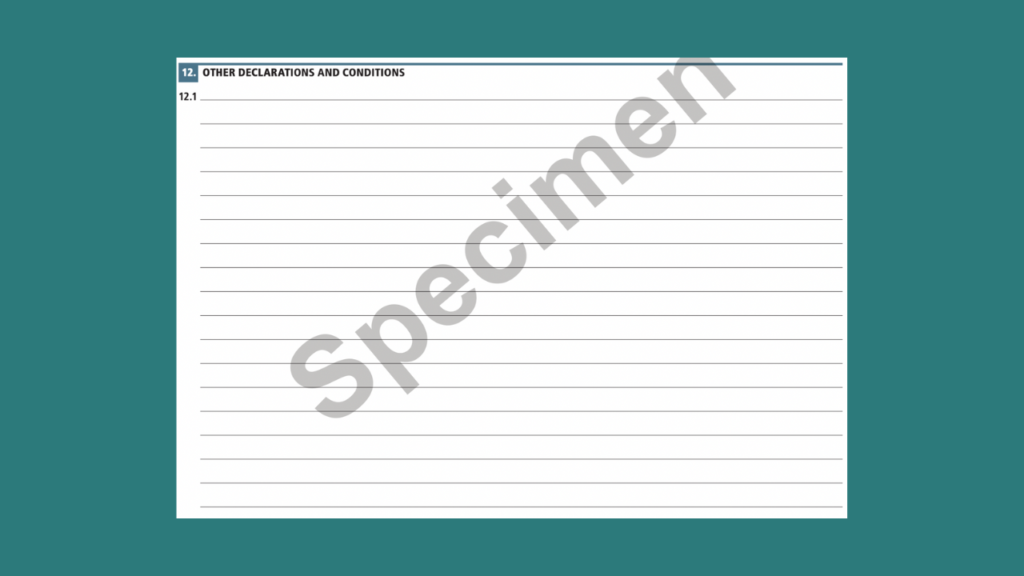

12. Other declarations and conditions

Section 12 is a catch-all section, where any additional clauses can be added. You will often see buyer’s brokers add in requests for repairs, inclusion of specific furniture, sale conditions tied to another transaction, or requests for special tests such as for pyrite, mould, asbestos and vermiculite, radon and / or iron ochre.

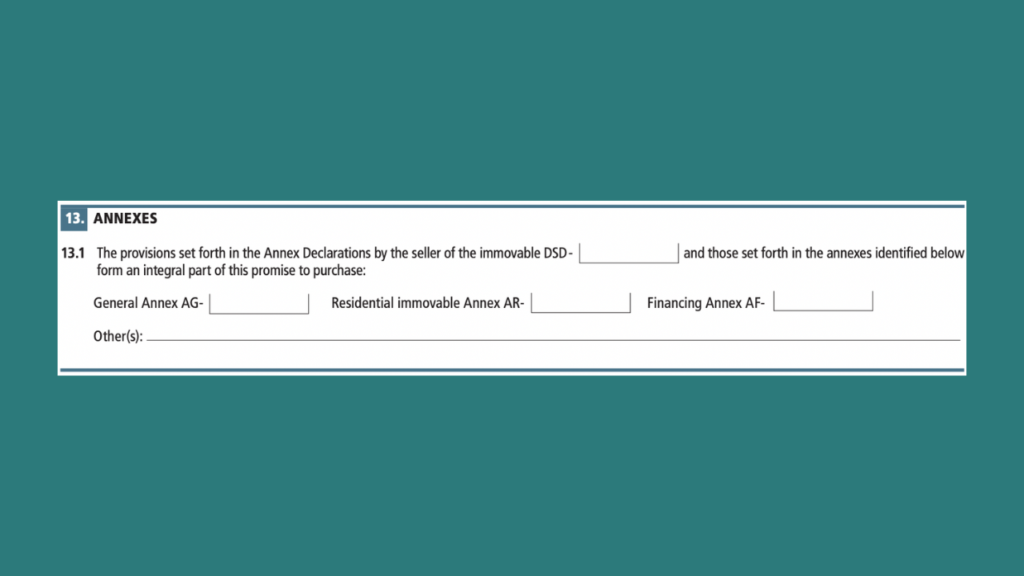

13. Annexes

Lists any extra documents attached to the offer like building inspection reports, financial pre-approvals, or special agreements.

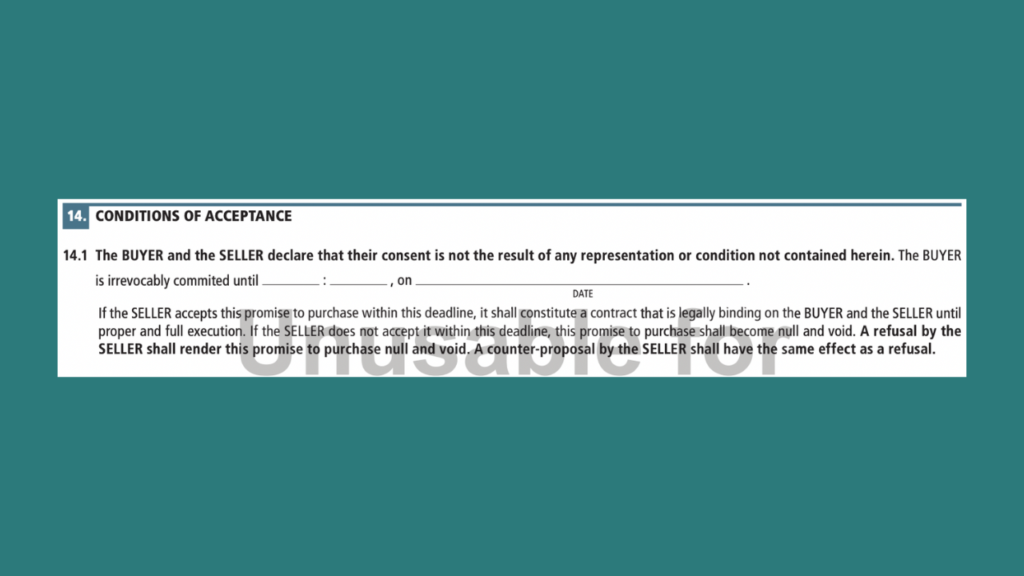

14. Conditions of acceptance

Specifies the deadline by which the seller must accept the offer and how the acceptance will be communicated. Generally speaking, you should set a timeline that works for you and that does not give time for the seller to get more competing offers on the table.

15. Interpretation

Clarifies how the document should be legally interpreted in case of ambiguity, ensuring both parties understand the terms the same way.

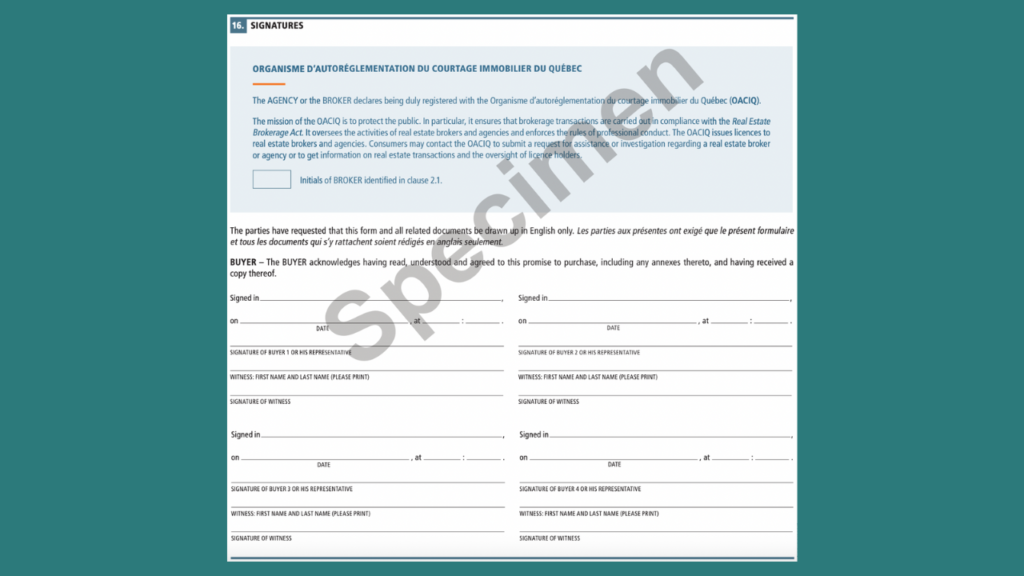

16. Signatures

The final section where both the buyer and seller sign and date the document, making the promise to purchase legally binding.

Top things to watch out for

Most sellers are represented by a listing agent whose job is to get the seller the best possible price.

They may be friendly, helpful, and reassuring—but they represent the seller, not you.

That doesn’t mean you shouldn’t trust them. It means you should verify important claims independently and make sure every protection you need is written into your offer. If you are working with a buyer’s agent this is something that they should do.

In this section we give you a three things that you need to watch out for before you sign your promise to purchase.

1. Run a Comparative Market Analysis (CMA)

Before you commit an offer, it’s important to understand what similar homes in the area have recently sold for. This is known as a Comparative Market Analysis (CMA), and it helps you determine whether your offer price is in line with the current market or whether you are overpaying.

The simplest way to get this information is to work with a local realtor who understands recent sales, neighbourhood trends, and how buyers are actually pricing similar properties in your area.

⚠️ Warning

CMAs are complex. You need to understand the local market, the condition of the property, and the cost of any required repairs. Otherwise, you run the risk of paying a premium for problems you didn’t spot.

To find a local agent, use Immovision AI. We scan more than 27 million past real estate transactions to identify the top-performing realtors in your area.

2. Trust, but verify everything

If you are buying a house, you need to check:

- Visual condition of the property (foundation, roof, windows, drainage, signs of water damage, cracks, etc.)

- Seller’s Declaration for past issues and known defects

- Previous inspection or expert reports

- Repair and maintenance records

- Renovation invoices

- Permits and certificates of compliance for major work

- Warranties and maintenance contracts

- Certificate of location

- Documents relating to the septic system, well, or water supply (if applicable)

- Past incidents such as water infiltration, flooding, sewer backups, fire, infestations, cannabis cultivation, asbestos, pyrite, radon, etc.

If you are buying a condo, you should also check:

- Declaration of co-ownership

- Condo bylaws and rules

- Minutes of board and co-owner meetings

- Financial statements

- Financial forecasts and budgets

- Contingency fund (reserve fund) information

- Special assessments (current or planned)

- Insurance information

- Request for Information to the Syndicate (RIS)

- Any ongoing legal disputes involving the syndicate

- Restrictions on rentals, pets, renovations, short-term rentals, etc.

Need Help Preparing Your Offer? (It's Usually Free)

An experienced buyer’s broker doesn’t just negotiate the price—they save you thousands by negotiating repair credits, price drops after home inspections, inclusions, and seller-paid closing costs.

Use Immovision AI to find a top-rated, local buyer’s agent in seconds. It’s usually free.

3. Set up the right conditions

You should, at a minimum, obtain a pre-purchase inspection. Depending on the property, additional specialized inspections may also be necessary.

You should also ensure that all relevant documents have been provided and carefully reviewed. If anything is missing, your promise to purchase should be made conditional on your ability to obtain and verify those documents.

It’s also important to understand how conditions work: if a defect or issue has already been properly disclosed by the seller, you generally cannot later use that same issue to justify backing out of the offer after the inspection period. If you want to investigate a disclosed issue further—for example, a faulty sump pump, or HVAC system that has not been inspected for 20 years—you should specifically include that concern as a condition in your offer.

How to negotiate your promise to purchase like a pro

Listing agents often use strategic pricing and marketing tactics to generate competition and drive multiple offers. In these situations, the highest offer does not always win — the strongest overall offer does.

As a buyer, it’s important to understand how to structure your promise to purchase so that it remains competitive while still protecting your interests. In a multiple-offer scenario, this can mean balancing price, conditions, timelines, and flexibility so that your offer is attractive to the seller without exposing you to unnecessary risk.

Frequently asked questions

1. If the offer is rescinded before the seller receives it;

2. If there is an escape or cancellation clause already included in the contract;

3. If an agreement is reached between the parties;

4. If one of the conditions in the contract isn’t met.

Final remarks

The promise to purchase communicates your offer to buy a property. Whilst the promise to purchase differs according to the type of property e.g. detached house vs a plex, there are 16 core sections that are universal to all promise to purchase contracts.

Each section gives the buyer an opportunity to negotiate not just on price, but on timelines, conditions, and risk.

Experienced brokers research the seller and the property to identify factors that may influence the seller’s flexibility. This might include how long the property has been on the market, whether the asking price aligns with comparable sales, or whether public records suggest financial pressures might exist.

While no two situations are the same, understanding the seller’s position helps you structure an offer so that it reflects where you may (or may not) have leverage. The promise to purchase then becomes the tool you use to test that leverage and adjust your strategy based on the seller’s response.

Need Help Preparing Your Offer? (It's Usually Free)

A buyer’s broker can help you structure your promise to purchase, negotiate the purchase price, and protect your interests throughout the transaction. In most cases, their commission is even paid by the seller.

Don’t rush your transaction. Don’t overpay for your home.