Definition

What is a hypothec of construction?

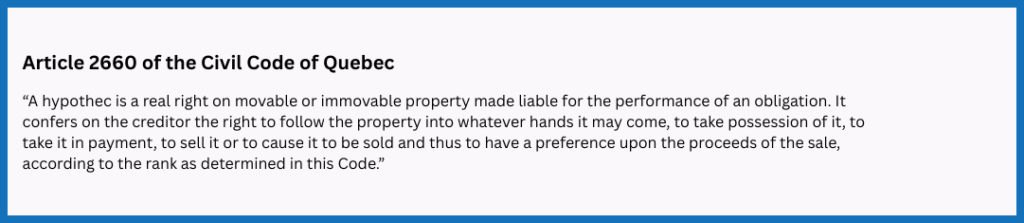

The hypothec of construction is a legal claim or lien that a contractor, builder, or supplier can place on a property for unpaid construction, renovation, or repair work. Article 2660 of the Quebec Civil Code gives the creditor the right to follow the property into whoever owns it, take possession of it, claim it as payment, or sell it themselves. This protection allows those who have worked on a project to have recourse in case of non-payment. The existence of hypothecary rights also encourages prompt payment across the industry.

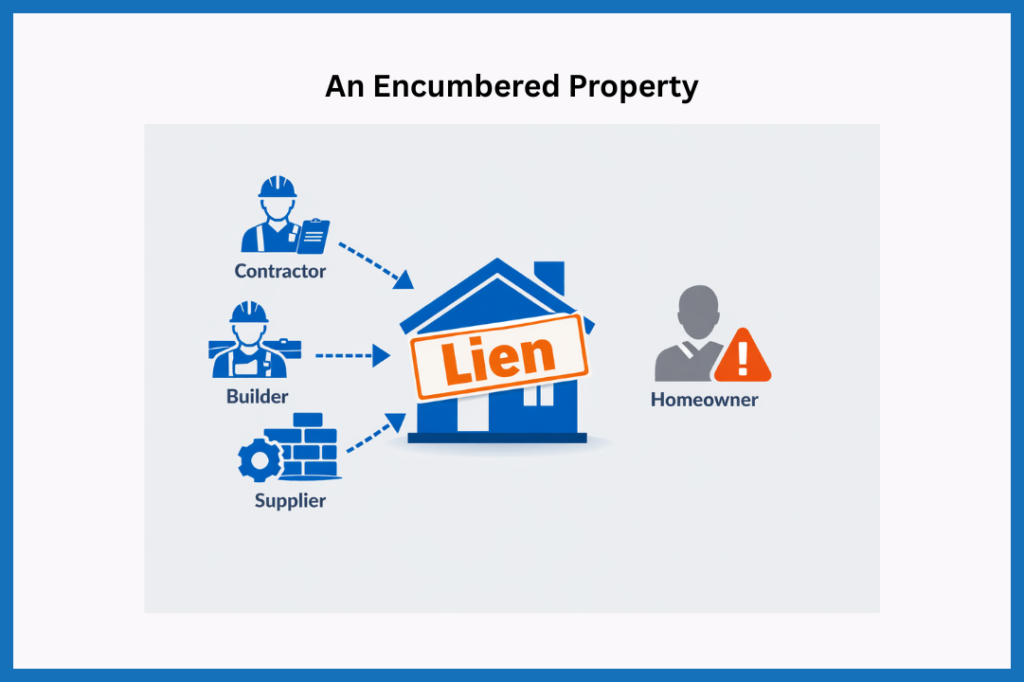

In real-estate terms, we say that the lien encumbers the property. This means that if you are the owner of the property, you must resolve any outstanding construction debts before transferring, selling, or using the property as collateral.

Who has the right to file a legal construction hypothec in Quebec?

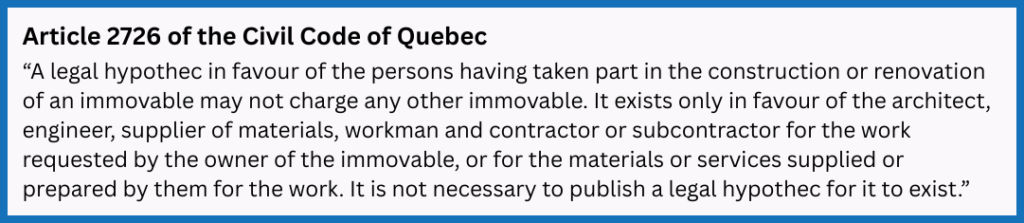

Article 2726 of the CCQ states who may file a legal construction hypothec and how this works.

According to Article 2726, creditors are allowed to register a construction lien only on the property where they performed the work. It can only include the value of the work, services, or materials supplied to that specific property. This means it cannot include, for example, work done on another property. And the legal hypothec exists regardless of who ordered the work or who currently owns the property.

The steps to register a construction hypothec

According to Article 2726, a construction hypothec comes into existance as soon as a contractor, builder, or supplier provides labour or materials to the property. To keep the hypothec alive, the contractor must actively enforce it. This means:

- Publication: After substantially completing the construction work, the contractor or supplier must publish the hypothec at the Quebec Land Registry Office and serve a notice of preservation to the owner via bailiff within 30 days.

- Prior notice: The contractor or supplier must also serve a prior notice of exercising the hypothec to the owner and co-contractor (if they are different people) and publish it within six months after the work ends.

- Deadline enforcement: If the contractor or supplier does not complete these steps properly, the hypothec expires and loses its validity.

Note

Hypothec of construction divided vs undivided condos

When a single owner holds the entire property — for example, a detached, semi-detached, townhouse — the contractor registers a legal construction hypothec directly on the property, and the owner alone must pay any outstanding construction debts.

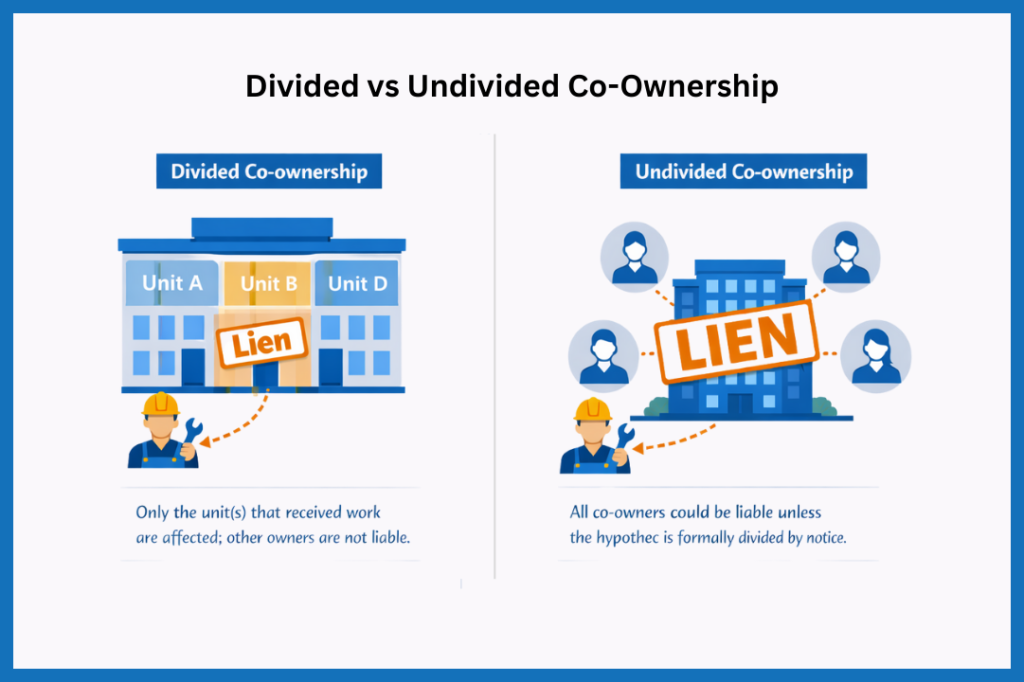

Co-ownerships are more complex because multiple people share the property. The co-owners’ liability for a construction hypothec depends on the co-ownership type: divided or undivided.

In a divided co-ownership, a legal construction hypothec applies only to the unit(s) that benefited from the work, meaning only the co-owners whose property value increased are responsible (Article 1051 CCQ). By contrast, co-owners in of an undivided co-ownership share the property collectively. As such, the law permits the contractor to register a hypothec against the whole building. As such this can effect all owners who could be liable for a portion of the debt based on their ownership share, even if the work only benefited part of the property. This is unless the contractor formally divides the hypothec by filing a notice.

How to check for a hypothec of construction

To check for a hypothec of construction, you can initially work with your real-estate agent. They will look for evidence that contractors have been paid by reviewing the seller’s declaration, invoices and reciepts for any renovation work done and the certificate of location. They can also check the Quebec Land Register however, realistically only the top agents do this level of due diligence.

Once the agent is satisfied that they have done their own due diligence, they will help you to make the promise to purchase close the property. Clause 10.1.5 of the promise to purchase states that the seller declares that the immovable is not the subject of a pre-emptive right in favour of a third party. This means the seller confirms that no third party has a claim or legal interest in the property that hasn’t been revealed. Finally, before you purchase the property, the notary will run a title search to check that the property is free of any liens, hypothecs, or other claims that could affect your ownership.

All of these checks make it unlikely that a hidden lien would go unnoticed. If a lien did slip through because the seller failed to disclose it, the seller could be held liable for any losses caused by the undisclosed claim.

Why does the hypothec of construction matter in real-estate

The hypothec of construction matters in real estate because creditors register it against the building itself, not the person who ordered the construction work. This means that it can directly affect property ownership (the property title), sale, and financing.

1. It follows the property, not the owner

Even if the person who hired the contractor sells the property, the lien remains attached to the property itself. This means the new owner must pay any outstanding construction debt if the previous owner did not resolve it.

2. It can block a sale or transfer

You cannot legally transfer a property with an active construction hypothec until the owner clears the debt. Notaries typically check for hypothecs during a title search before completing a sale. If the owner does not clear the lien, the sale cannot go through, and they could face the original debt, interest, and legal fees to release the hypothec.

3. It can force a sale

If contractors enforce their hypothec through the courts, they can force a sale. The notary pays the contractor first from the sale proceeds, before the owner, mortgage lender, or other creditors, which could leave the owner still owing mortgage debt while losing the property.

4. It affects financing

Mortgage lenders view a legal construction hypothec as a high-priority lien. If unpaid, it can take priority over the mortgage, putting the lender’s loan at risk. Before approving financing, lenders make owners pay or resolve the construction hypothec.

5. It protects contractors but creates risk for owners

While contractors collect payment through the hypothec, buyers face a hidden risk. If they don’t check for it, they could inherit unexpected debts tied to prior construction or renovation work.

Frequently asked questions

Final remarks

A hypothec of construction is a legal claim that a contractor, builder, or supplier can place on a property to secure payment for construction, renovation, or repair work. This system is there to ensure that the contractor receives prompt payment for their work.

From a real-estate perspective, buyers should verify whether a hypothec of construction exists on the property. If one does exists, then they should work with their real-estate agent to either pay or settle the claim before closing the sale, or re-adjust the purchase price to reflect the cost. Buyer’s may also want to investigate property title insurance to safeguard against hidden liens or other title issues on the property.