In Quebec, there are two types of co-owned properties: divided and undivided.

In this article, we cover:

- What is a divided co-ownership?

- What is an undivided co-ownership?

- The differences between divided vs undivided co-ownerships at a glance

- A detailed look at divided vs undivided condos

- The pros and cons of divided vs undivided co-ownerships

- Which is best, a divided or undivided condo?

To start with, what is a divided co-ownership?

What is a divided co-ownership?

In a divided co-ownership (or divided condo), each owner owns their individual unit outright while sharing ownership of the building’s common areas, including the lobby, roof, and parking areas. It is the most common type of condo ownership in Quebec.

The graphic below gives you a visual illustration of what a divided condo looks like.

A divided condo is similar to individual property ownership in that, each unit:

- Has its own cadastral number (or lot number)

- Pays their own property taxes (municipal and school taxes)

- Can go to any lender for their mortgage pre-approval

What is an undivided co-ownership?

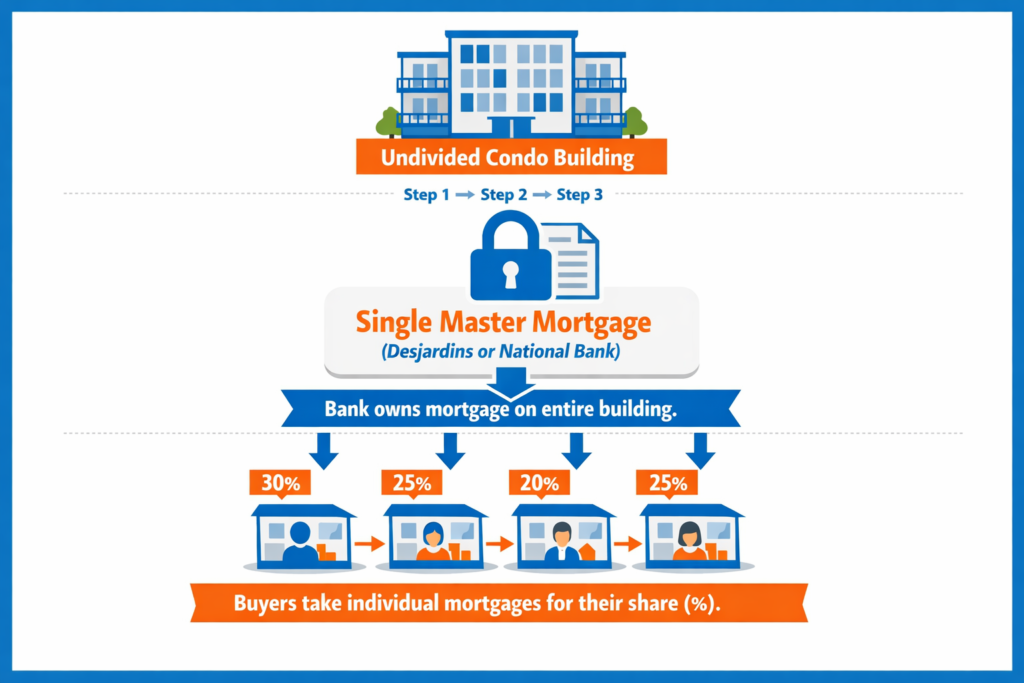

Undivided co-ownership are like companies in that owners of the undivided condo will own a share of the building. For example, you might buy into 3% of the ownership of the building. In this case you would be responsible for 3% of the building. For example, you are responsible for 3% of the tax account for the entire building. This type of co-ownership is much more like being in partnership with the other owners.

The differences between divided vs undivided co-ownerships at a glance

The table below shows the main differences between divided and undivided condos.

| Divided co-ownership | Undivided co-ownership | |

| Best for | Buyers seeking independence and resale flexibility | Families, friends or investors buying together to share costs |

| Co-ownership type is like | Owning an individual condo unit in a managed building | Sharing ownership of an entire property with private usage agreements |

| Size of down payment (minimum) | ~5% | ~20–30% (usually 20% for owner-occupied, 30% for rental) |

| Banks that finance | Most major banks and lenders | Only two – Desjardins and National Bank |

| Key documents | Declaration of co-ownership (sets out condo rules, shares, and maintenance) | Indivision agreement (defines rights, shares and usage) |

| Unit cadastral numbers | Yes – each unit has its own title | No – one title for the entire property |

| Management | Managed by a syndicate of co-ownership (condo association) | Managed collectively by co-owners |

| Contingency fund | Mandatory reserve fund (for major repairs) | No formal requirement, relies on co-owners’ savings |

| Insurance fund | Building insured by syndicate; owners insure their own unit | Shared insurance arranged by co-owners |

| Owner expenses | Each owner pays own expenses and taxes | Collective account for shared bills and mortgage |

| Ability to sell | Easy – can sell or mortgage your unit independently | Harder – other co-owners often have first right of refusal |

| Options to rent | Usually allowed, subject to condo rules | Usually allowed, but must follow indivision agreement |

| Ability to renovate | You can renovate your unit freely (within condo bylaws) | Only minor interior work; major changes need co-owner approval |

| Repossession of dwelling | Yes – lender can repossess your specific unit | No – because the whole property is shared |

| Condo fees | Normally monthly condo fees paid to syndicate | Usually higher or more irregular – depends on agreements |

A detailed look at divided vs undivided condos

We can group the differences between divided and undivided condos into seven categories. These are:

- Owner finances

- Contracts

- Building management

- Building finances

- Renting divided vs undivided condos

- Repossession

Let’s dive into the differences in these condo types now.

Owner finances

One of the main differences between divided and undivided condos is the size of downpayment you need to buy. You can buy a divided condos with as little as a 5% downpayment, whereas to buy an undivided condos you will often need a minimum of 20% downpayment. Also, whilst almost any bank will give you a a mortgage for a divided condo, there are only two banks in Quebec that finance undivided condos: Desjardins and National Bank.

With undivided condos specifically, Desjardins or National Bank holds a single mortgage on the entire building. Buyers must then take out their individual mortgage through the same bank, for their percentage share of ownership in the property. This means that the banks will own one master mortgage contract with all the individual owners of the property.

Because all co-owners share one mortgage, a default by one co-owner means the others may have to cover that person’s monthly payments. This can be hard for the bank to enforce, making the entire loan riskier, and so the bank adds extra restrictions to protect itself. For example, the mortgage contract will not allow one owner to refinance or sell their share freely since, since the whole property is the banks collateral.

Contracts

There are major difference in terms of which documents that govern how the divided vs undivided co-ownership organizes themselves, make decisions and what owners rights are to do things like rent or renovate individual their condo units. The table below shows the main contracts you need to understand when buying a divided or undivided condo.

| Contract Type | Divided Condo | Undivided Condo |

| Main governing document | Declaration of Co-Ownership – Defines each private unit, the common areas and ownership shares. | Indivision Agreement – Defines each owner’s share, rights, exclusive use areas, and cost-sharing rules. |

| Daily rules | Bylaws – Covers building rules (noise, pets, renovations, etc.). | Often included within the indivision agreement itself; sets out similar lifestyle and usage rules. |

| Purchase contract | Promise to Purchase – Adapted for divided co-ownership. | Promise to Purchase – Adapted for undivided co-ownership. |

| Financial / Management documents | Minutes & Financial Statements of the Syndicate – Show building finances, reserve fund, and major repairs. | Co-Ownership Loan Agreement – Shared mortgage contract with the bank for the entire property. |

| Optional supporting documents | Insurance and Contingency Fund Statements – Verify coverage and building health. | Occupancy Agreement – May specify which co-owner occupies which unit, if not detailed in the indivision agreement. |

Building management

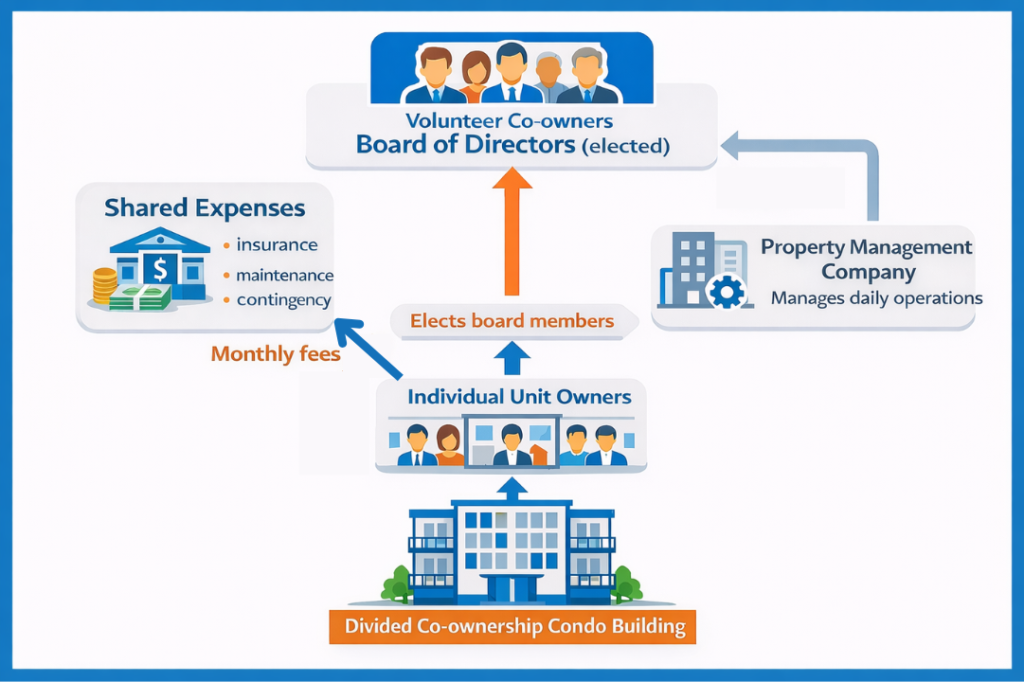

Owning a divided co-ownership is like owning a single unit in a building. You pay your own property taxes and maintain your unit’s interior, while a syndicate of co-ownership (or condo association) manages the building. Co-owners elect a board of directors, usually volunteers from among themselves, to run the syndicate. The board typically appoints a property management company to handle daily operations, but the company usually has no seat on the board or voting rights.

Individual unit owners pay a monthly fee to cover shared expenses, including building management, insurance, common-area maintenance, snow removal, and contributions to the contingency fund for future repairs.

By contrast, an undivided co-ownership is more like a partnership where each “partner” owns a share of the entire property rather than a separate unit. The co-owners sign an indivision agreement that defines who occupies each apartment, how they share expenses, and how they make major decisions.

In an undivided co-ownership, there is no condo syndicate. Instead the co-owners themselves handle everything, from maintenance and insurance to approving renovations and collecting contributions for shared costs. As with divided condos, co-owners will typically appoint a property manager, who will present key decisions about building maintenance to them. However, unlike a divided co-ownership, the co-owners vote to appoint this company rather than leaving the decision to a small group of directors.

Building finances

Divided and undivided co-ownerships manage building finances very differently.

In a divided co-ownership, the building functions like a small organization with its own legal structure and finances. The syndicate of co-ownership (condo association), led by a board of directors, manages daily operations. Co-owners pay condo fees into the syndicate’s bank account, which the syndicate uses for operating expenses (cleaning, electricity, snow removal, etc.), insurance, professional services, and a mandatory contingency fund. The syndicate must keep detailed financial statements and share them with owners annually.

In contrast, undivided co-ownerships have no syndicate or board, and no legal entity manages the money. Instead, the co-owners handle everything jointly under the indivision agreement. Each co-owner pays their share of common expenses (insurance, taxes, maintenance) into a shared account managed by an appointed representative. The co-owners will vote on large expenses (usually they require a by majority or unanimous decision making). The property receives a single municipal tax bill, which the co-owners split according to their shares.

Renting divided vs undivided condos

In an undivided co-ownership, the bank does not allow the owners’ to rent out their units. This is because rentals typically carry additional risk. For instance, tenants can stop paying rent, treat the building with less care than owners, and create landlord-tenant disputes, all of which could affect the bank’s investment. If a co-owner does want to rent out part of a unit, they will need written approval from the other co-owners and the bank (which is rare).

By contrast, in divided condos, each unit owner can generally rent out their condo, unless the declaration of co-ownership or condo bylaws restrict it (for example, requiring minimum lease durations or prohibiting short-term rentals like Airbnb). The board enforces these rules, it doesn’t invent them, but it can interpret and apply them, such as approving or rejecting tenant applications.

Note

Renovating divided vs undivided condos

When it comes to renovations, divided and undivided condos work very differently.

In a divided co-ownership, owners have much more freedom to renovate the inside of their units. For instance, owners can usually make cosmetic or layout changes like painting, flooring or even re-modeling their kitchens, bathrooms, bedrooms etc. all without asking for approval. However, the condo’s board of directors must approve any work that affects the building’s structure, plumbing, electrical systems, or common areas (like balconies or exterior walls). Owners must also follow the declaration of co-ownership when carrying out the work.

In an undivided co-ownership, things are stricter. This is because changes to one unit can impact the overall property valuation and each co-owner’s share. As such, co-owners need to follow the indivision agreement, where most renovations require the consent of all co-owners or, in some cases, the bank. As a result, renovations can be slower and require more coordination.

Repossession of dwelling

In a divided co-ownership, each condo unit has its own mortgage and property title. This means that if an owner stops making payments, the bank can repossess that individual unit. In this case, the lender will enforce its hypothec (mortgage) and take ownership of the unit. The lender will then sell the unit to recover the debt. This change does not directly affect the other condo owners in the building.

In an undivided co-ownership things are much more complicated. If one co-owner defaults, the lender can claim the entire property, not just that co-owner’s share. However, in practice the lender usually works with the other co-owners to cover the missed payments or buy out the defaulting owner’s share. If that fails, the bank can seize and sell the entire building, even if the others have paid their share.

Pros and cons of divided co-ownership vs undivided co-ownership

In this section, we cover the pros and cons of divided co-ownership vs undivided co-ownership.

Pros and cons of divided co-ownership

Divided condos offer the independence and flexibility of true homeownership, combined with the convenience of shared building management.

Owners have full ownership over their units. This means that they can sell or rent their units and have more freedom to renovate and personalize the interior of their home. Financing is straightforward and condo associations handle most of the building’s maintenance and insurance. This makes it a hands-off option for busy professionals or investors looking to buy and rent. The trade-off is that divided condo owners pay monthly condo fees and must follow the building’s declaration of co-ownership, which can limit things like short-term rentals, large interior renovations or exterior modifications.

Pros and cons of an undivided co-ownership

Undivided condos are more like partnerships than individual ownership.

All owners share ownership of the entire property with other co-owners, each with exclusive rights to occupy a specific unit. These properties are usually more affordable to buy into but require a larger down payment and come with tighter restrictions on financing, renting and renovations. Since the co-owners do not have a condo syndicate, they make all decisions collectively. This means strong cooperation among co-owners is essential. This setup can work well for families, close friends or long-term co-owners who value shared responsibility and lower entry costs more than the ability to rent, sell, or modify their unit independently.

Final remarks

The difference between divided and undivided co-ownership comes down to control and responsibility: in divided condos, each owner fully controls their unit and pays their own fees, while in undivided co-ownership, owners share the whole property, the mortgage, and all decisions.

As such, choosing between a divided and an undivided co-ownership really depends on your goals, finances, and lifestyle.

If you want independence, easy financing and long-term resale or rental potential, a divided condo is usually the smarter choice. You’ll have more control over your unit, simpler dealings with lenders, and clearer rules through the declaration of co-ownership.

On the other hand, if you’re looking for a more affordable way to buy into the market, perhaps with family members or close friends, an undivided condo can be appealing. The lower purchase price can make ownership accessible, but it comes with trade-offs: higher down payments, fewer financing options, and the need for strong collaboration among co-owners.